ARTICLE / CLIENT ALERT / US POLICY

December 19, 2024

Read time: 10 min

Deemed the Fourth Industrial Revolution, artificial intelligence (AI) has emerged as the newest watershed technological development of the 21st century, as evidenced by its near ubiquity in discussions of everything from how the information economy functions to the way art is made. The rapid development and deployment of AI technologies took society and governments by surprise.

The US government has since taken a variety of wide-ranging aspirational steps, but legislative activity has been absent. Recent actions by federal and state regulators offer insights into the priorities surrounding AI enforcement. Although these priorities, as well as the nature and scale of enforcement, may shift under the new Trump administration, recent enforcement actions demonstrate the tools available for AI enforcement.

In the wake of the explosive emergence of ChatGPT, the Biden administration took a number of executive actions addressing AI but largely focused on policies and positions related to responsible AI use. In October 2023, President Biden issued an executive order for the “Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence,” which underscored the administration’s commitment to the research, development, and deployment of responsible uses of AI. The executive order instructed the US Department of Commerce to develop guidance for content authentication and watermarking to clearly label AI-generated content and requires developers of AI models that implicate national security, national economic security, and public health and safety to share their safety test results and other critical information with the US government.

President Biden also formed the AI Safety Institute at the National Institute for Standards and Technology, which is part of the Commerce Department. Prior to his election, President-elect Trump pledged to repeal the AI executive order, stating that it “hinders AI Innovation” and that “Republicans support AI Development rooted in Free Speech and Human Flourishing.” Although it remains to be seen how a Trump administration will differ in its treatment of AI, enforcement actions focused on standard causes of action such as fraud and deceptive trade practices are likely to continue, even in the absence of new or more comprehensive federal regulation.

In Congress, Senator Chuck Schumer has led calls for a comprehensive legislative AI framework, although, to date, that has taken the form of legislative working groups and roadmap documents. (In May 2024, the Bipartisan Senate AI Working Group released a “[r]oadmap for artificial intelligence policy in the United States Senate,” stating that “existing laws, including related to consumer protection and civil rights, need to consistently and effectively apply to AI systems and their developers, deployers, and users.) Yet there has been no federal legislation.

There has, however, been substantial legislation passed on the state level. In June 2024, Colorado passed its Artificial Intelligence Act, the first state comprehensive framework addressing the development and deployment of AI, which requires developers of “high-risk artificial intelligence” to use reasonable care to protect consumers from the risks of “algorithmic discrimination.” In September 2024, California passed more than a dozen AI-related bills, including measures imposing disclosure requirements on AI companies regarding the datasets used to train their models, requiring healthcare providers to disclose when they use generative AI to communicate with patients, and imposing limits on how healthcare providers and insurers can automate their services. Since 2023, Indiana has created an AI task force, and Illinois, Louisiana, Texas, and West Virginia have established committees on AI. Additionally, New Hampshire has made it a crime to fraudulently use deepfakes and has created a cause of action.

In the absence of federal legislation and regulation specifically targeting AI, agency officials and prosecutors are regulating AI through the enforcement of existing laws in areas such as consumer protection, financial services, privacy, and civil rights. Enforcement activity thus far has been limited and consistently focused on the impact of AI on individuals, including abuses of AI to perpetrate fraud or deceive consumers.

In the past year, prosecutors have targeted crimes committed through or with the assistance of AI, rather than scrutinizing the development of the technologies themselves. There has been a particular emphasis on the ways in which AI has been implicated in unfair or deceptive practices and the types of fraudulent schemes commonly prosecuted by both local and federal law enforcement.

FTC Actions

On September 25, 2024, the US Federal Trade Commission (FTC) announced a new law enforcement sweep called Operation AI Comply. Lina M. Khan, chair of the FTC, emphasized that “[u]sing AI tools to trick, mislead, or defraud people is illegal” and “there is no AI exemption from the laws on the books.” The initiative specifically targeted operations that either used AI or sold AI technology that could be used in deceptive and unfair ways, as evidenced by the enforcement actions included in the initial rollout of the initiative:

- DoNotPay, an online subscription service offering assistance with commercial and legal issues, held itself out to be “the world’s first robot lawyer” and settled charges for false or unsubstantiated performance claims. The settlement required the company to pay $193,000 and issue a notice to consumers who subscribed to the service between 2021 and 2023 warning them about the limitations of the law-related features of the service.

- Ascend Ecom, Ecommerce Empire Builders, and FBA Machine – three separate companies operating online business opportunity schemes – were charged by the FTC for making representations about their AI-powered business models as part of deceptive earnings claims. As a result of these complaints, federal courts temporarily halted each scheme and put the entities under the control of a receiver.

- Rytr, which marketed and sold an AI writing assistant that produced AI-generated reviews, settled charges for providing its customers with the means to generate false and deceptive written content for consumer reviews.

In November 2024, the FTC charged Sitejabber, a company offering an AI-enabled consumer review platform that “deceived consumers by misrepresenting that ratings and reviews it published came from customers who experienced the reviewed product or service, artificially inflating average ratings and review counts.” More recently, the FTC has negotiated settlements with two different companies involved in security systems – Evolv Technologies and IntelliVision Technologies Corp. Evolv was alleged to have made false representations about its AI-powered security screening system, claiming that it can detect weapons and ignore harmless personal items, including in sports stadiums, hospitals, and schools. Samuel Levine, the director of the FTC’s Bureau of Consumer Protection, underscored that representations about a technology’s abilities need to be especially accurate when they concern the safety of children. IntelliVision Technologies was alleged to have made deceptive claims about its facial recognition software – specifically that its AI-powered facial recognition software was free of gender and racial bias and that it had one of the highest accuracy rates on the market.

SEC Actions

The FTC is not alone in its recently expressed commitment to investigating and applying existing regulatory frameworks to products and services involving or purporting to involve AI. On March 18, 2024, the US Securities and Exchange Commission (SEC) announced that it had settled charges against two investment advisers, Delphia (USA) Inc. and Global Predictions Inc., for making false and misleading statements about their purported use of AI. The firms agreed to settle the SEC’s charges and pay $400,000 in collective civil penalties. The SEC found that Delphia did not have the AI and machine learning capabilities that it claimed. It also found that Global Predictions falsely claimed to be the “first regulated AI financial advisor” and misrepresented that its platform provided “[e]xpert AI-driven forecasts.”

Gary Gensler, chair of the SEC, explained that the two companies had marketed that they were using AI in certain ways when they were not. Gensler referred to this type of misleading claim as “AI washing” and cautioned that companies are capitalizing on the buzz created by the new technologies and purporting to use them to lure and mislead investors and customers. On January 25, 2024, the SEC issued an Investor Alert “to make investors aware of the increase of investment frauds involving the purported use of artificial intelligence (AI) and other emerging technologies.”

State Regulator Actions

Some state regulators have also addressed AI technology through enforcement actions. Most recently, the Texas Attorney General’s Office (AGO) announced a “first-of-its-kind” settlement with a healthcare generative AI company, Pieces Technologies. The settlement resolved allegations that the company had made a series of false and misleading statements about the accuracy and safety of its AI products. According to the Texas AGO, the settlement “highlights the potential for enforcement against AI companies under existing laws that are not specific to AI” and emphasized the importance of “exercising caution in developing claims about an AI product’s efficacy or performance.” This Texas case can also be seen as a warning to companies to understand what their vendors or contractors are doing with respect to AI. Although the Texas AGO targeted the technology provider itself – not the four major Texas hospitals that deployed the technology – the action remains of import to those who use advanced technologies.

Other state attorneys general have also announced or demonstrated a commitment to act on AI, especially using traditional consumer protection theories. In 2023, 23 state attorneys general, including both Democrats and Republicans, responded to the National Telecommunications and Information Administration (NTIA) request for comment on AI policies and urged NTIA to ensure that “AI systems are valid and reliable, safe, secure, and resilient, accountable and transparent, explainable and interpretable, privacy-enhanced, and fair.”

Areas of Future Enforcement

Regulatory activity by the FTC and other agencies also highlights areas of interest for future enforcement. Specifically, the FTC has issued information-seeking orders to eight companies offering surveillance pricing products and services that incorporate data about consumers’ characteristics and behavior. Surveillance pricing refers to the “opaque market” for products sold by third-party intermediaries that “claim to use advanced algorithms, artificial intelligence, and other technologies, along with personal information about consumers – such as their location, demographics, credit history, and browsing or shopping history – to categorize individuals and set a targeted price for a product or service.” The FTC has also expressed interest in AI investments and the partnerships between AI companies, and it has commenced a study of the industry, including information requests to a number of major technology companies.

Finally, the FTC has expressed interest in the risks of generative AI, which can include chatbots, deepfakes, and voice clones. The agency has urged individuals and companies to consider whether they should be making or selling a synthetic media or generative AI product given the potential opportunities for its misuse; whether all reasonable precautions to mitigate the risks of the product are being taken; whether the technology or product is misleading people about what they are seeing, hearing, or reading, particularly in the context of advertising; and whether the burden is on the consumer to detect AI-generated content. Individuals and companies operating in this space should carefully weigh the FTC’s non-exhaustive list of concerns presented by both the creation and implementation of AI technologies.

As of now, federal regulations aimed at AI have yet to be issued, but the enforcement actions described above and the interests telegraphed by the FTC and other regulators confirm that companies need to remain apprised of and vigilant about the risks posed by AI technologies, even as they capitalize on its innovative qualities. While the impact of a new but slim Republican majority in Congress remains unclear, the Trump administration is expected to approach regulatory enforcement of AI with a lighter touch. This is particularly true given the administration’s announcement of tech investor David Sacks as the White House “AI & Crypto Czar.” Nevertheless, bipartisan interest in the AI space and recent enforcement trends indicate that there will continue to be a focus on AI abuses under fraud and deceptive trade practices theories.

Post-Election Outlook: Issues to Watch for Pharmacy Industry Stakeholders

ARTICLE / CLIENT ALERT / US POLICY

December 5, 2024

Read time: 9 min

The 2024 election results will create significant tailwinds for Republican legislative and regulatory priorities in US Congress, federal agencies, and state houses across the country. This On the Subject considers the outlook for pharmacy regulation under the second incoming Trump administration and a unified Republican Congress, as well as state-level pharmacy policies that may advance as Republican public policy momentum builds.

In its second term, the Trump administration is likely to pursue many of the priorities left unfinished at the end of its first term. With respect to pharmacy regulation, during President-elect Trump’s first term, Congress enacted the Know the Lowest Price Act and the Patients’ Right to Know Drug Prices Act. These two acts prohibited “gag clauses” in agreements between pharmacies and pharmacy benefit managers, removing a potential barrier for pharmacists to disclose less expensive drug options to consumers. The legislation sought to increase transparency and reduce patient out-of-pocket costs.

Despite these legislative achievements, several pharmacy priorities discussed in the Trump administration’s American Patients First blueprint remained unfulfilled at the conclusion of the first Trump term. The second Trump administration and Republican-led state houses and administrative agencies will also look to conservative think tanks, such as the America First Policy Institute, the Heritage Foundation, and the Paragon Health Institute, for recommendations on legislative and regulatory strategies to further Republican priorities. Tellingly, in January 2018, the Heritage Foundation reported that President-elect Trump’s first administration had adopted almost two-thirds of its policy recommendations.

Drug Price Transparency

The Trump administration, along with the broader Republican Party, considers transparency and natural market dynamics to be a key pathway to reducing healthcare costs. During the first Trump term, President-elect Trump’s administration implemented several price transparency measures, including a Transparency in Coverage (TiC) Rule that cobbled together several statutory authorities to require certain group health plans and issuers to disclose patient cost-sharing information, in-network provider negotiated rates, and drug pricing information.

On August 20, 2021, the Biden administration determined to defer enforcement of the TiC Rule’s requirement that plans and issuers publish machine-readable files related to prescription drugs. On April 19, 2022, the Biden administration issued a temporary “safe harbor” for circumstances where compliance was “not possible,” but on September 27, 2023, the Biden administration withdrew the safe harbor and announced a “case-by-case” enforcement approach.

In its second term, the Trump administration may look to unwind the flexibilities of the Biden administration and take a stronger stance in enforcing the TiC Rule as applicable to prescription drugs. Many states have passed prescription drug transparency laws, although these laws are most commonly focused on transparency of wholesale acquisition costs, as opposed to consumer out-of-pocket costs that are likely to influence patient choice. Focus by the Trump administration and statehouses on greater consumer access to cost-sharing obligations at the pharmacy counter may affect both prescribing and dispensing trends for prescription drugs.

Biosimilar Products

President-elect Trump’s American Patients First blueprint reasoned that improving the availability, competitiveness, and adoption of biosimilars as “affordable alternatives to branded biologics” can promote innovation and competition for biologics, thereby bringing down prices. The American Patients First plan called for the US Food and Drug Administration (FDA) to continue to educate clinicians, patients, and payors about biosimilar and interchangeable products and asked for suggestions on resources and tools for the FDA to improve the efficiency of the biosimilar and interchangeable product development and approval processes. The blueprint asked for additional suggestions on how to improve the interchangeability of biosimilars and the potential effects on prescribing, dispensing, and coverage of biosimilar and interchangeable products. An interchangeable product may be substituted for its reference product without the intervention of the healthcare provider who prescribed the reference product.

In June 2024, the Biden administration issued draft guidance updating the 2019 Guidance for Industry entitled, “Considerations in Demonstrating Interchangeability With a Reference Product.” According to the new draft guidance, experience has shown that for products approved as biosimilars, the risk in terms of safety or diminished efficacy is insignificant following single or multiple switches between a reference product and a biosimilar product. The FDA acknowledged that its scientific approach to when a switching study or studies may be necessary to support a demonstration of interchangeability “has evolved.” The FDA’s draft guidance would allow applicants to provide an assessment of why the data otherwise provided to the FDA for biosimilar approval supports the switching standard absent data from a switching study or studies. Finalizing this guidance would be consistent with the Trump administration’s historic interest in improving access to interchangeable biosimilars.

The American Patients First blueprint also indicated a need to give each biosimilar a unique billing and payment code under Medicare Part B, which would incentivize the development of additional lower-cost biosimilars. The blueprint stated that the current approach to biosimilar coding and payment creates a “race to the bottom” of biosimilar pricing while leaving the branded product “untouched,” making the biosimilar market unviable and one “that few would want to enter.” Because HCPCS Level II coding for biosimilars is largely unbound by statutory or regulatory requirements, the Trump administration’s Centers for Medicare and Medicaid Services may revisit the HCPCS Level II coding policies to establish a more diversified code set for biosimilars.

Vaccines

President-elect Trump has announced he will nominate Robert F. Kennedy Jr. (RFK) to be the Secretary of the US Department of Health and Human Services (HHS). He also has chosen Dr. Marty Makary to be the US Food and Drug Administration (FDA) Commissioner, Dr. Jay Bhattacharya to lead the National Institutes of Health (NIH), and Representative Dave Weldon to lead the Centers for Disease Control and Prevention (CDC).

RFK has made several statements questioning the safety and efficacy of certain vaccines purchased and administered by pharmacies across the country. If confirmed by the US Senate and appointed, RFK would oversee the FDA Commissioner, who in turn has the authority to approve vaccine applications. The Secretary also selects the director of the HHS National Vaccine Program, which coordinates with the NIH, the CDC, the FDA, and the US Department of Defense to provide direction for research on vaccinations and adverse events related to vaccines. The Secretary can also influence certain health plan, Medicare Part D, and Medicaid coverage of vaccines through oversight of the Advisory Committee on Immunization Practice and the CDC. Medicare Part B coverage of certain vaccines (pneumococcal, influenza, COVID-19, and hepatitis B) is established by statute, but coverage for other vaccines is subject to the Medicare Part B “reasonable and necessary” coverage requirement.

Any action that restricts the development and introduction of new vaccines, the approval of currently available vaccines, or reimbursement for vaccines may disrupt pharmacy vaccine service delivery. Such actions are likely to be challenged in federal court and subject to judicial scrutiny under the interpretive framework of Loper Bright v. Raimondo and the Administrative Procedure Act, as applicable.

Pharmacist Scope of Practice

Support for expanding the scope of practice of pharmacists has continued to gain momentum in recent years, heralded by the Cicero Institute as a potential solution to primary care shortages. Many states have expanded pharmacist scope of practice beyond dispensing medications to include administering immunizations and long-acting injectable medications, prescribing hormonal contraceptives, prescribing antivirals for influenza and COVID-19, counseling on tobacco cessation, and providing point-of-care diagnostic testing services. Several states have enacted statutes defining pharmacist scope of practice based on a “standard of care” model, where pharmacists must act consistently with their education, training, and experience and within the accepted standard of care provided in a similar setting by a reasonable and prudent pharmacist.

Reimbursement for an expanded scope of pharmacist services is also gaining traction in Congress, where the Equitable Community Access to Pharmacist Services Act has collected almost 150 bipartisan cosponsors in the US House of Representatives and 28 bipartisan cosponsors in the Senate as of the time of publication. The legislation would create a new Medicare Part B benefit category for pharmacist services and services furnished incident to the service of a pharmacist. Covered services would include the evaluation and management of patients for testing or treatment of COVID-19, influenza, respiratory syncytial virus, or streptococcal pharyngitis. Medicare Part B would reimburse pharmacist services through the Medicare Physician Fee Schedule as a percentage of physician reimbursement.

Given its potential to reduce the costs of certain types of care and federal healthcare program expenditures, expanding the scope of practice for pharmacists may gain additional momentum with the new federal administration and in state houses. However, scope of practice reforms have historically encountered challenges in Congress and faced considerable political obstacles.

Key Takeaways

- Pharmacy and pharmacy-adjacent regulation is very likely to undergo a period of moderate disruption as the incoming Trump administration takes actions to transition from the outgoing Biden administration, potentially affecting various aspects of healthcare policy, regulatory frameworks, and industry practices.

- Pharmacy and pharmacy-adjacent laws, regulations, and guidance oriented toward transparency, competition, and reduced out-of-pocket costs may benefit from tailwinds from the incoming Trump administration and more conservative state houses.

- Pharmacies and pharmacy stakeholders should consider engaging with federal and state government representatives and regulators on proposed legislation, regulations, and subregulatory guidance that may advance or hinder their strategic interests.

- Several areas of legislation, regulation, and administrative action appear ripe for movement following the 2024 elections. These include drug price transparency, biosimilar interchangeability approval and reimbursement, vaccine approval and reimbursement, and pharmacist scope of practice.

What a Second Trump Term Means for Antitrust Enforcement

ARTICLE / CLIENT ALERT / US POLICY

December 3, 2024

Read time: 8 min

On January 20, 2025, President-elect Donald J. Trump’s administration will come into power. The McDermott antitrust and competition team has analyzed the first Trump term, compared it to the Biden administration’s actions, and reviewed statements from those involved in the upcoming Trump administration. While it appears that the new administration will be good for business, especially for companies planning to expand through mergers and acquisitions, this client alert takes a closer look at what is likely to change and what is likely to stay the same in antitrust enforcement throughout the next four years.

What Will Change

Merger policy is likely to be much more pro-business than during the Biden era.

- Enforcement agencies are likely to abandon the 2023 merger guidelines. In 2023, the Federal Trade Commission (FTC) and the US Department of Justice (DOJ) released revised merger guidelines.[1] These new guidelines lowered market share and concentration levels at which a merger would be presumed illegal. It is anticipated that the Trump administration will abandon enforcement of the presumption at these lower concentration levels and restore enforcement under the prior guidelines.[2] This means that the Trump administration is likely to allow deals to proceed if there are a number of significant competitors to the merging firms, although “3 to 2” and “4 to 3” mergers will still likely be blocked. Furthermore, early termination of the Hart-Scott-Rodino Antitrust Improvements (HSR) Act waiting period is expected to be granted for non-problematic deals. However, it is still important to avoid “bad documents” and customer complaints.

- Antitrust analysis is likely to focus solely on traditional economics. While the Biden administration sought to expand the scope of analyzing a transaction’s effect on labor, the Trump administration will likely focus squarely on a transaction’s impact on prices and innovation, dismissing labor effects when analyzing mergers.[3] Although a win for the Biden-era FTC, in FTC v. Tapestry, Inc., the US District Court for the Southern District of New York applied a traditional horizontal merger analysis and found a narrow market definition.[4] Even though this helped the FTC block the merger, this narrow market definition could be a powerful offensive tool. This is especially true for consumer products mergers, indicating that deals can proceed if the merging parties’ products in the same category are meaningfully differentiated by price, quality, or brand image.

- “Fixable” deals are likely to return. The Biden administration has all but disallowed merging parties from fixing problematic aspects of their deals to avoid regulatory challenge. However, under the second Trump administration, enforcement agencies are likely to permit more deal fixes through divestitures and consent orders, paving the way for more mergers, as they did during the first Trump term.

- Vertical deals are likely to be allowed more frequently. Similar to the return of fixable deals, the Trump administration is expected to be more open to considering behavioral remedies in vertical mergers that would otherwise be problematic. This is a departure from the Biden administration’s policy, which largely foreclosed the possibility of such settlements. The Biden administration lost its vertical merger challenge in the merger of UnitedHealth and Change Healthcare,[5]bwhere the court accepted the merging parties’ behavioral commitments and rejected the government’s challenge. In addition, the Trump administration is less likely to scrutinize vertical deals and is more likely to recognize the cost savings generated by many vertical transactions.

Premerger procedure changes face an uncertain future, but firms should plan for the new rules to take effect as scheduled.

The new rules for premerger notification under the HSR Act are set to go into effect on February 10, 2025,[6] less than a month after Trump will enter office. These rules could be blocked by Congress, delayed by the president, or rescinded or changed by the new DOJ and FTC. However, current FTC staff assumes the new rulemaking will go into effect in February 2025, and we suggest merging parties prepare to comply with the new rules for deals filed after February 10, 2025. Furthermore, even if current FTC Chair Lina M. Khan steps down on day one of the Trump administration, the FTC will still comprise two Republican and two Democratic commissioners, making it unlikely they will reach a majority required to delay the rule.

Agency appointees are expected to endorse a more predictable mainstream antitrust policy.

- Pam Bondi, the former attorney general of Florida from 2011 to 2019, has been nominated for US attorney general. During her tenure as Florida’s attorney general, she joined other states in bringing antitrust suits against generic drugmakers and optical disk drive manufacturers. Along with five other states, Bondi settled with the National Football League in a resale ticket price floor case. Furthermore, she investigated the broiler chicken industry. She does not appear to favor progressive antitrust enforcement as the original attorney general nominee, Matt Gaetz, does.

- Most candidates being rumored for senior antitrust and competition roles in the DOJ and FTC have corporate or law firm experience.

The FTC is likely to roll back many initiatives from the Biden era.

Once Trump nominates a new member of the FTC to bring its composition to three Republicans and two Democrats, the Commission is likely to withdraw the FTC’s rule significantly restricting employee noncompetes and the very aggressive and broad-reaching 2022 Policy Statement on FTC Act Section 5 enforcement.[7] The 2022 Statement has been strongly criticized by current Republican FTC commissioners and Project 2025.[8] In its place, the FTC could readopt the more moderate 2015 Policy Statement on Section 5, which limited the application of Section 5 to conduct that came close to violating the Sherman Act.[9]

Patents are likely to receive greater protection.

Like the first Trump term, where there was little antitrust challenge to standard essential patents, the second Trump term is expected to be pro-patent in antitrust matters, too.

Companies in the political crosshairs could see renewed scrutiny.

In Trump’s first term, the DOJ challenged the merger of Time Warner and AT&T. Trump expressed opposition to the merger under the belief that it would give greater influence to CNN, which had been critical of him and his administration. Similarly, companies that are critical of or disfavored by the second Trump administration could face similar scrutiny and investigation.

What Will Likely Stay the Same

State attorney general enforcement is likely to remain steady or even increase.

State attorneys general, particularly from states with Democratic attorneys general, are likely to step in to fill the void left by a reduction in FTC and DOJ antitrust enforcement. For example, in Trump’s first term, the DOJ settled a telecommunications merger, but states sought an injunction to block the deal in court. Most states have pending antitrust investigations and suits against “Big Tech” companies. Additionally, several state attorneys general are challenging a major grocery merger, supporting the FTC appeal of its noncompete rule, pushing legislation to stop price-gouging, and considering broader premerger notification requirements.

The focus on Big Tech is likely to persist.

The first Trump administration filed cases against and investigated prior acquisitions by several major technology companies. Project 2025 recommends that the FTC continue to investigate Big Tech for potential antitrust violations. However, there may be some departure from the Biden administration’s approach to remedies. The Biden DOJ asked for a remedy that would force Google to sell its Chrome browser, while Trump has expressed potential for settling the Google case short of a breakup.

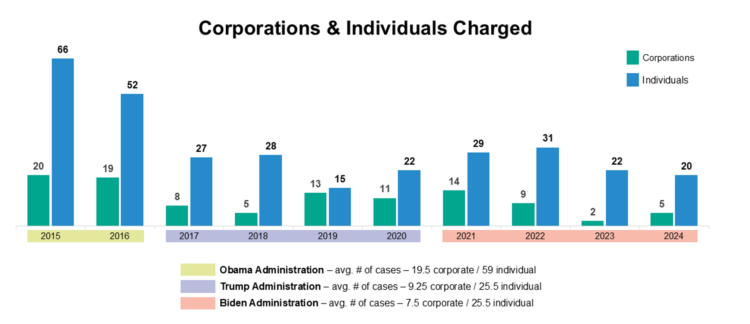

Criminal enforcement is likely to continue its current trajectory.

The first Trump administration filed a similar number of cases as the Biden administration, as shown in the chart below. It is likely that this trend will continue.

Overall, we expect the Trump administration to be much more favorable to transactions as compared to the Biden administration. The Trump administration is likely to be less willing to challenge vertical transactions or transactions under novel theories, such as bundling, and we expect more merger settlements. We believe the Trump administration will not scrutinize private equity transactions to the same extent as the Biden administration and will focus on challenging traditional horizontal transactions. From a conduct perspective, we expect the Trump administration to continue scrutinizing Big Tech and maintain criminal antitrust enforcement at a moderate level.

Supreme Court Rules on Purdue Pharma Chapter 11 Plan: No Authorization for Release of Nonconsensual Claims Against Third Parties

ARTICLE / CLIENT ALERT / US POLICY

July 3, 2024

Read time: 10 min

Introduction

On June 27, 2024, in a highly anticipated ruling, the Supreme Court held that the Bankruptcy Code does not authorize the release of claims against non-debtors without the consent of affected claimants in a ruling springing from the Purdue Pharma bankruptcy. In the 5-4 decision, penned by Justice Gorsuch, the Supreme Court rejected confirmation of the Purdue Chapter 11 plan and remanded the matter back to Judge Sean Lane and the Bankruptcy Court for further proceedings consistent with the Court’s opinion. This is likely the most significant bankruptcy ruling by the Supreme Court since at least 2011 – one that will impact the negotiation and confirmation of bankruptcy plans – particularly, but not exclusively, in cases involving mass tort claims. Harrington v. Purdue Pharma L. P., No. 23-124, 2024 WL 3187799 (US June 27, 2024)

Background

Purdue Pharma, a manufacturer of branded opioid medications, including OxyContin, faced thousands of lawsuits after an affiliate plead guilty to misbranding OxyContin as a less-addictive and less-abusable alternative to other pain medication. To avoid the consequences of the onslaught of litigation, the Sackler family, which owned and controlled Purdue Pharma, withdrew approximately 75 percent of Purdue’s assets over a decade. Left in a significantly weakened financial state, Purdue filed for bankruptcy on Sept. 15, 2019.

Purdue’s original proposed Chapter 11 plan sought to resolve the opioid litigation by incorporating a settlement framework that included a release of claims, both current and future, against the Sackler family in exchange for a lump-sum settlement payment of $4.325 billion at the time of confirmation. The Plan additionally sought to release negligence claims as well as claims for fraud and willful misconduct, and included releases of the family by both consenting and non-consenting creditors.

Most voting creditors supported the plan, although there were a number of other creditors that included opioid victims who voted against the Plan. The Bankruptcy Court approved the Plan and entered a confirmation order on Sept. 17, 2021. Certain parties, including the US Trustee appealed the confirmation order. Pending appeal to the Second Circuit, the Sacklers agreed to contribute an additional $1.175 to $1.675 billion to Purdue’s estate if eight states and the District of Columbia withdrew their remaining objections to the plan. Those states and the District eventually consented, increasing potential recovery to $6 billion. The Second Circuit later affirmed the Bankruptcy Court’s confirmation of the Plan, allowing for it to contain nonconsensual releases of direct claims against the non-debtor Sackler family. After a subsequent appeal by the office of the US Trustee, the US Supreme Court granted certiorari.

Supreme Court Ruling

Majority Opinion

At the outset of its ruling, the Court made it clear that the Sacklers “ha[d] not filed for bankruptcy and ha[d] not placed virtually all their assets on the table for distribution to creditors, yet… [sought] what essentially amount[ed] to a discharge,” something usually reserved for debtors. Thus, the question for the Court boiled down to whether a bankruptcy court may extend the benefits of a Chapter 11 discharge to non-debtors. The majority’s decision approached this question in four ways — by: (1) conducting a textual/statutory interpretation analysis of Bankruptcy Code § 1123(b); (2) looking at related and relevant provisions in the Code to further interpret the meaning of section 1123(b); (3) taking notice of the history of Bankruptcy law; and (4) analyzing the parties’ policy arguments.

- The Text of § 1123(b)

Section 1123(b) sets out, in a list, what a Chapter 11 plan may contain. As the Court observed, that list concludes with § 1123(b)(6) which states that a plan may “include any other appropriate provision not inconsistent with the applicable provisions of this title.” Proponents of the Plan interpret § 1123(b)(6) to allow “a debtor to include in its plan, and a court to order, any term not ‘expressly forbid[den]’ by the bankruptcy code as long as a bankruptcy judge deems it ‘appropriate’ and consistent with the broad ‘purpose[s]’ of bankruptcy.” Thus, Plan proponents believe that § 1123(b)(6) allows the plan to include the nonconsensual release of claims against the Sackler family.

In its analysis, the Court applied the doctrine of ejusdem generis, a statutory interpretation method that sets out that a “catchall must be interpreted in light of its surrounding context and read to ‘embrace only objects similar in nature’ to the specific examples preceding it.” More simply, ejusdem generis “seeks to afford a statute the scope a reasonable reader would attribute to it.”

The Court held that the common thread among the five preceding paragraphs to § 1123(b)(6) is that they all concern the debtor and authorize “a bankruptcy court to adjust claims without consent only to the extent such claims concern the debtor.” The Court thus held that “a bankruptcy court’s powers are not limitless and do not endow it with the power to extinguish without their consent claims held by nondebtors (here, the opioid victims) against other nondebtors (here, the Sacklers).”

2. Related Provisions

The Court next looked to various related statutory provisions for guidance.

First, the Court looked to Bankruptcy Code § 1141 to determine “what is and who can earn a discharge.” The Court noted that the Code “reserves the benefit [of a discharge] ‘to the debtor’”, and the Plan proponents’ interpretation of § 1123(b)(6) would be contrary to the Code by “affording to a nondebtor a discharge usually reserved for the debtor alone.”

Second, the Court noted §§ 541, 523, and 1141 for the proposition that the Bankruptcy Code constrains both the debtor and the discharge of claims against the debtor. More specifically, the Court noted that (1) “[t]o win a discharge…the code generally requires the debtor to come forward with virtually all its assets,” (2) a discharge “does not reach claims based on ‘fraud’ or those alleging ‘willful and malicious injury,’ and (3) a discharge cannot “‘affect any right to trial by jury’ a creditor may have ‘with regard to a personal injury or wrongful death tort claim.’” The Court then held that the settlement provision of the Plan transgresses the Code’s limitations.

Finally, the Court addressed § 524(g) – a “notable exception to the code’s general rules.” Under § 524(g), for asbestos-related bankruptcies (and only for asbestos-related bankruptcies), “courts may issue ‘an injunction…bar[ring] any action directed against a third party’ under certain statutorily specified circumstances.” The Court held that because “the code does authorize courts to enjoin claims against third parties without their consent, but does so in only one context, [it] makes it all the more unlikely that § 1123(b)(6) is best read to afford courts the same authority in every context.”

According to the Court, Plan proponents argued that the limits imposed on debtors and discharges are inapplicable because the Sacklers sought a release, not a discharge. Nonetheless, after looking to related Code provisions, the Court held that no matter how the Sacklers’ sought relief is classified, “nothing in the bankruptcy code contemplates (much less authorizes) it.”

3. History

The third component critical to the Court’s holding was that no party had directed them to a statute (including any prior versions of the Bankruptcy Code) or case “suggesting American courts in the past enjoyed the power in bankruptcy to discharge claims brought by nondebtors against other nondebtors, all without consent of the individuals affected.” According to the Court, “if Congress had meant to reshape traditional practice so profoundly in the present bankruptcy code, extending to courts the capacious new power the plan proponents claim, one might have expected it to say so expressly ‘somewhere in the [c]ode itself.”

4. Policy

Lastly, the Court’s opinion entertained both sides’ policy arguments. Proponents of the plan argued that without the releases, there would be no “viable path” for victims to recover. In the Brief for the Petitioner, the US Trustee disputed this, setting out that with the increased legal exposure resulting from potential lawsuits by individual victims, States, and other governmental entities, the Sacklers might be induced to negotiate consensual releases on more favorable terms. Moreover, the US Trustee argued that with the allowance of nonconsensual third-party releases, tortfeasors would be able to obtain immunity from claims that they normally could not discharge in bankruptcy, all the while failing to place “anything approaching all of their assets on the table.” This, according to the US Trustee, “would provide a ‘roadmap for corporations to misuse the bankruptcy system’ in future cases ‘to avoid mass-tort liability.’”

Despite acknowledging these perspectives, the Court held that it was the wrong audience for the policy arguments, which are for Congress to address. To further emphasize the limited nature of their ruling, the Court also explicitly stated that nothing in their decision should be “construed to call into question consensual third-party releases offered in connection with a bankruptcy reorganization plan,” and the Court was not expressing a view on what qualified as a consensual release. Finally, the Court set out that it would not address whether their reading of the Bankruptcy Code “would justify unwinding reorganization plans that have already become effective and been substantially consummated.”

Dissent

Writing for the dissent, Justice Kavanaugh emphasized that the Court’s decision essentially rewrote the text of the Bankruptcy Code and restricted “the long-established authority of bankruptcy courts to fashion fair and equitable relief for mass-tort victims.” Justice Kavanaugh also explained that because of a 2004 indemnification agreement where Purdue agreed to pay for the legal fees and liability expenses of its officers and directors, the non-debtor release provision would have protected the Purdue estate from being depleted by indemnification claims and would have ensured the victims receive compensation.

Justice Kavanaugh stated:

“[d]espite the broad term ‘appropriate’ in the statutory text, despite the longstanding precedents approving mass-tort bankruptcy plans with non-debtor releases like these, despite 50 state Attorneys General signing on, and despite the pleas of the opioid victims, today’s decision creates a new atextual restriction on the authority of bankruptcy courts to approve appropriate provisions.”

According to Justice Kavanaugh, non-debtor releases are “absolutely critical” to achieving the bankruptcy system’s overarching goal of fair and equitable relief for victims and creditors.”

Takeaways

There are a few key takeaways and considerations following this landmark decision.

- While the opinion likely will have a profound impact on bankruptcy cases, including mass tort bankruptcies, the parameters of that impact are yet to be determined. Non-debtor affiliates of debtors will clearly not be able to receive the benefit of a full release from non-consenting parties. However, those non-debtor affiliates can still use the bankruptcy process to negotiate litigation settlements – with whatever benefits or disadvantages a bankruptcy process could bring. Alternatively, those non-debtor entities can file for bankruptcy to take full advantage of the provisions of the Bankruptcy Code – including potential discharge or other debt resolution.

- The justices expressly avoided defining what constitutes a “consensual” release; future courts will have to make determinations on whether things like “opt-out” releases constitute consent.

- With respect to the Purdue bankruptcy itself, the Debtors have asked the Bankruptcy Court to re-enter mediation. In re Purdue Pharma L.P., et al., 19-23649 (Bkrtcy. Ct. SDNY, June 27, 2024), ECF Doc. 6498. It remains to be seen whether the parties will return to mediation and emerge with a new settlement or otherwise propose a new Chapter 11 plan.

Authored by Douglas S. Mintz and Reuben E. Dizengoff.

If you have any questions concerning this Alert, please contact your attorney or one of the authors.

Supreme Court Finds Insurer Has Standing Despite ‘Insurance Neutrality’

ARTICLE / CLIENT ALERT / US POLICY

June 21, 2024

Read time: 8 min

Introduction

On June 6, 2024, the Supreme Court – in a unanimous decision delivered by Justice Sotomayor – addressed the issue of whether an insurer holding financial responsibility for a bankruptcy claim qualifies as a party in interest under Bankruptcy Code § 1109(b). Reversing the Fourth Circuit decision below, the Court concluded that insurer Truck Insurance Exchange is sufficiently concerned with the proceedings so as to qualify as a party in interest because § 1109(b) is “capacious” and “asks whether the reorganization proceedings might directly affect a prospective party, not how a particular reorganization plan actually affects that party.” Truck Ins. Exch. V. Kaiser Gypsum Co., Inc., No. 22-1079, 2024 WL 2853106 (US June 6, 2024) (emphasis added).

Background

Debtors Kaiser Gypsum Company, Inc. and its parent company, Hanson Permanente Cement, Inc., produced and sold products containing asbestos, and consequently faced tens of thousands of asbestos-related lawsuits. To resolve these liabilities, Debtors filed for Chapter 11 bankruptcy and, under the proposed reorganization plan, created a § 524(g) Asbestos Personal Injury Trust. Section 524(g) “allows a Chapter 11 debtor with substantial asbestos-related liability to establish and fund a trust that assumes the debtor’s liability for ‘damages allegedly caused by the presence of, or exposure to, asbestos or asbestos-containing products.’” Here, the trust contains all present and future claims related to liability springing from asbestos use. In addition to the § 524(g) trust, the Plan also set out to transfer all of Debtors’ rights under their insurance contracts to the trust.

Truck Insurance served as Debtors’ primary insurer. Under the terms of Truck Insurance’s contract, transferred under the Plan, Truck Insurance is obligated to indemnify Debtors up to $500,000 per claim while Debtors must pay a $5,000 deductible per claim and assist in defending against the claims. At issue was the Plan’s provision treating insured and uninsured claims differently. While insured claims are to be filed in the tort system for the benefit of insurance coverage, uninsured claims are to be submitted directly to the trust for resolution. Most importantly, insured claims, unlike uninsured claims, lack disclosure requirements necessitating claimants to identify any related claims in order to reduce fraudulent and duplicative claims.

With the above discrepancy in mind, Truck Insurance filed an objection to the otherwise consensual Plan. Truck Insurance objected, asserting that the trust does not comply with § 524(g) and “the Plan would provide ‘anti-fraud’ protections to the trust in resolving uninsured claims but not to Truck Insurance in resolving insured claims,” subjecting Truck Insurance to potentially millions of dollars in fraudulent tort claims. In re Kaiser Gypsum Company, Inc., 60 F.4th 73, 80 (4th Cir. 2023). Truck Insurance had previously insisted to Debtors that the anti-fraud measures be applied to insured claims but Debtors declined, leading to Truck Insurance’s other contention that the Plan “appear[ed] to be collusive and in violation of [the Debtors’] duty to cooperate and assist,” and in breach of the implied covenant of good faith and fair dealing. Id.

In September 2020, the Bankruptcy Court for the Western District of North Carolina ruled against Truck Insurance and recommended that the District Court for the Western District of North Carolina confirm the Plan. In its recommendation, the Bankruptcy Court adopted Debtors’ Proposed Findings of Fact and Conclusions of Law and set out that Truck Insurance was not a party in interest and lacked standing to object to the Plan. More specifically, the Bankruptcy Court concluded that Truck Insurance could not object because the Plan is “insurance neutral” and returns Truck Insurance to the tort system exactly as it was prepetition. The Bankruptcy Court also stated that Truck Insurance lacked standing despite being a creditor in the case. Later in July 2021, the District Court adopted the Proposed Findings of Fact and Conclusions of Law and confirmed the Plan. Truck Insurance subsequently appealed to the Fourth Circuit.

The Fourth Circuit affirmed the District Court’s judgment. In its analysis, the Fourth Circuit held: “[i]n determining whether a particular reorganization plan sufficiently affects an insurer’s legal rights to render that insurer a party in interest, courts typically look to see whether the plan is ‘insurance neutral.’” In re Kaiser Gypsum Company, Inc., 60 F.4th at 83. Put differently, “[i]f a plan is insurance neutral, the objecting insurer ordinarily is not a party in interest under § 1109(b) and thus lacks standing to challenge the substance of the Plan.” Id.

According to the Fourth Circuit, a plan is deemed insurance neutral “if it doesn’t increase the insurer’s pre-petition obligations or impair the insurer’s pre-petition policy rights.” Id. Ultimately, the Fourth Circuit held that “the Plan was insurance neutral because it expressly preserved Truck [Insurance]’s coverage defenses and the Debtors’ assistance-and-cooperation obligations under the policies, thereby placing Truck [Insurance] in the same position as it was pre-bankruptcy.” Id. at 83-84.

Truck Insurance appealed to the Supreme Court and the Court granted certiorari.

The Supreme Court Reverses the Fourth Circuit’s Decision

The Court began its analysis by looking at the language, context and history of § 1109(b). This provision of the Bankruptcy Code sets out that “[a] party in interest, including the debtor, the trustee, a creditors’ committee, an equity security holder, or any indenture trustee, may raise and may appear and be heard on any issue in a case under this chapter.”

The Court held that a common thread among the parties listed in § 1109(b)’s definition of a party in interest “is that each may be directly affected by a reorganization plan either because they have a financial interest in the estate’s assets…or because they represent parties that do.”

As to context and history, the Court found the following. First, Congress uses the term “‘party in interest’ in bankruptcy provisions when it intends the provision to apply broadly,” and the “general theory behind [§ 1109(b)] is that anyone holding a direct financial stake in the outcome of the case should have an opportunity…to participate in the adjudication of any issue that may ultimately shape the disposition of his or her interest.” Second, “Congress consistently has acted to promote greater participation in reorganization proceedings.” Finally, drafters of the Bankruptcy Code hoped that with an expansive definition of party in interest, a broad range of individual/minority interests would be allowed to intervene in Chapter 11 cases and prevent dominant interests from controlling the restructuring process.

The Court next held that insurers with financial responsibility for bankruptcy claims are parties in interest given that reorganization proceedings can affect insurers’ rights in a variety of ways. For example, “a plan may be collusive, in violation of the debtor’s duty to cooperate and assist, and impair the insurer’s financial interests by inviting fraudulent claims.”

In the case at hand, the Plan, lacking disclosure requirements for insured claims, risks exposing Truck Insurance to millions of dollars in fraudulent claims and thus gives Truck Insurance an interest in the bankruptcy proceedings and the proposed Plan. Additionally, since the Plan eliminates the Debtors’ ongoing liability and claimants have no incentive to propose barriers to their recovery, Truck Insurance may be the only entity with the incentive to identify any issues with the Plan. Citing to In re Global Indus. Technologies, Inc., 645 F.3d 201, 204 (CA3 2011), the Court held that “[w]here a proposed plan ‘allows a party to put its hands into other people’s pockets, the ones with the pockets are entitled to be fully heard and to have their legitimate objections addressed.”

Lastly, in reversing the decision below, the Court also addressed the “insurance neutral” doctrine. According to the Court, “[t]his doctrine is conceptually wrong and makes little practical sense” because it “conflates the merits of an objection with the threshold party in interest inquiry.” More simply put, § 1109(b) evaluates whether a plan might affect a party, not how a plan actually affects a party. Thus, “[w]hether and how the particular proposed Plan… affects Truck [Insurance]’s prepetition and postpetition obligations and exposure is not the question.”

Analysis and Takeaways

- On the micro-level, this case broadens the ability of insurance companies to challenge proposed reorganization plans.

- More generally, by reversing the Fourth Circuit’s decision and holding that Truck Insurance is a “party in interest,” the Court has established that future § 1109(b) inquiries are to look not at the merits of an objection, but rather whether a prospective party may be affected by a proposed plan.

- The “insurance neutral” doctrine seemingly reached merits on the substance of a claim – before even considering the issue of standing. The Court roundly and unanimously rejected that approach.

Authored by Douglas S. Mintz.

If you have any questions concerning this Alert, please contact your attorney or one of the authors.

Heard at the 2024 Antitrust Law Section Spring Meeting: Part II

ARTICLE / CLIENT ALERT / US POLICY

April 12, 2024

Read time: 10 min

The American Bar Association Antitrust Law Section’s annual Spring Meeting concluded on April 12. The annual Spring Meeting featured updates from federal, state and international antitrust enforcers and extensive discussion on priority antitrust issues affecting various industries.

This article highlights takeaways from the final two days of the Spring Meeting.

State Enforcers Remain Active

Ignore State Antitrust Enforcers at Your Own Peril

Prominent state enforcers described how they are aggressively enforcing state and federal antitrust laws by bringing cases and reaching settlements with or without a concurrent action from federal antitrust enforcement agencies. For example, state antitrust enforcers have led the way on aggressively clamping down on noncompete agreements in employment agreements and investigating and challenging no-poach agreements.

Leading antitrust enforcers from California, Maryland, Utah and Washington state touted their own statutes that prohibit or severely restrict noncompetes and other post-employment restrictive covenants. In the merger context, more states are creating “mini-HSR regimes” requiring parties to notify state antitrust enforcers of transactions in certain industries where states are especially worried about consolidation, particularly in healthcare. Several states’ mini-HSR regimes require notification of transactions that would fall below the Hart-Scott-Rodino Act (HSR) regime’s reporting threshold.

Gwendolyn Cooley, Chair of the National Association of Attorneys General Multistate Antitrust Task Force, emphasized that state attorneys general have the right to challenge mergers based on nationwide effects – not just effects within their jurisdictions.

Increased Interagency Collaboration Supports Greater State Antitrust Enforcement

State enforcers are partnering with other federal and state agencies on antitrust enforcement. For example, Schonette Jones Walker, Chief of the Antitrust Division for the Maryland Attorney General, touted a recently launched partnership between the US Department of Agriculture and several state attorneys general to protect competition and consumers in food and agricultural markets.

The Biden Administration Continues ‘Whole-of-Government’ Approach to Competition Enforcement

The Biden Administration Is All in on Interagency Cooperation

The Biden administration has taken a “whole-of-government” approach to competition policy. In the wake of the administration’s July 2021 Executive Order on Promoting Competition in the American Economy, the Federal Trade Commission (FTC) and the US Department of Justice (DOJ) have entered into numerous memorandums of understanding with industry regulators.

Mac Conforti, Assistant Chief of the DOJ Antitrust Division’s Competition Policy & Advocacy Section, explained that the “whole-of-government approach” involves both enforcement and regulation. On the enforcement front, the antitrust agencies have opened more investigations and brought more cases as a result of interagency memorandums of understanding. These agreements have fostered information sharing and case referrals across a variety of industries, including agriculture. On the regulatory front, DOJ has issued public comments on proposed regulations from non-antitrust agencies in numerous industries, with the aim of shaping regulatory frameworks that enhance competition and limit barriers to entry.

Industry Regulators Are Focused on Competition

Industry regulators are also increasing their own focus on competition in their respective sectors. For example, the Consumer Financial Protection Bureau (CFPB) has increased its cooperation with DOJ and FTC and is actively exercising its own rulemaking authority to enhance competition in consumer financial markets.

In one initiative, CFPB is promulgating rules that would enhance the portability of consumer bank account information, promoting competition from smaller banks. Likewise, the Federal Deposit Insurance Corporation (FDIC) is in the process of modifying its bank merger review process. Traditionally, the FDIC’s bank merger analysis focused on parties’ market shares for local consumer deposits; however, its new approach will focus on competition in different product lines to take a more wholistic approach to bank mergers.

Consistent Antitrust Goals Remain

At the annual Enforcers Roundtable, FTC Chair Lina Khan and DOJ Assistant Attorney General (AG) Jonathan Kanter emphasized that the end goal of antitrust enforcement remains increasing access to products and services beneficial to the lives of everyday consumers.

Across the board, enforcers highlighted healthcare and digital markets as the top areas of their current and future enforcement priorities. Additionally, Cooley, Chair of the National Association of Attorneys General Multistate Antitrust Task Force, highlighted the states’ use of state legislation and resources in collaboration with the federal antitrust enforcers to investigate complex market realities, reinforcing the “whole-of-government” approach.

Regulators Are Focused on Information Exchanges

New Technologies Must Play by Old Rules

Markus Brazill, Counsel to the Assistant Attorney General at the DOJ’s Antitrust Division, emphasized that established principles regarding collusive conduct apply the same to the “digital realm” as they do to the “physical realm.” While many have called for new guidelines on algorithmic pricing and complex data aggregation, Brazill believes the “novelty” of these emerging technologies does not change the underlying antitrust principles. If anything, new technologies “facilitate collusive practices that would otherwise not be feasible.” DOJ will continue to treat price fixing – however it is achieved – as per se unlawful.

DOJ Opines on the Withdrawal of Safety Zones for Information Sharing

When DOJ and FTC withdrew their policy statements for the healthcare industry in 2023, they withdrew safety zones for information exchanges. Brazill emphasized that the healthcare statement’s safety zones were never meant to apply outside of the healthcare industry, and the safety zones and policy statements were “formalistic and arbitrary” and “not reflective of the economics of information exchanges.”

Assistant AG Kanter opined that the withdrawn guidelines included “outdated” guidance on the use of third-party intermediaries to mitigate antitrust risk resulting from data exchanges, and that nowadays, such third parties or technology tools will “magnify” potentially anticompetitive effects. Current DOJ and FTC leadership evaluate information exchanges on a case-by-case basis, typically under the rule of reason, analyzing the nature of the market and the type of information exchanged.

Aggressive Merger Enforcement

The New Merger Guidelines Signal a More Aggressive Approach

Agency staff commented on the new Merger Guidelines and the more aggressive approach to merger enforcement that they embody.

Under the December 2023 Merger Guidelines, DOJ and FTC look at how a transaction affects the full ecosystem of trading partners – including downstream customers, upstream suppliers and rivals. The antitrust agencies are also looking to competitive harms beyond increased prices and reduced output, such as lower quality, reduced consumer choice and less innovation. In addition, the guidelines allow the agencies to look solely at direct evidence of head-to-head competition and place less reliance on industry structure.

In the annual Enforcers Roundtable, Chair Khan further noted the agencies’ intent to conform their understanding of market realities to their theories of anticompetitive harm to protect the interests of nascent and innovative competitors. Khan also opined that the contention that an acquisition of a nascent competitor by an established firm is necessary for commercialization is unconvincing when the nascent competitor is selling to a monopolist. She emphasized that it is particularly critical to consider the effects of impeding nascent competition in the pharmaceutical industry.

Negotiating Remedies: Come Prepared With a Buyer Upfront

Agency staff emphasized that it is critical for merging parties to propose remedy packages that fully address all competitive concerns. In the antitrust agencies’ view, it is not their job to assist parties with determining what remedy package will be sufficient.

The agencies recommend selecting a strong divestiture buyer upfront and providing the government with unfettered access to that buyer, allowing the agency to vet its viability. The enforcers will view access restrictions – such as the merging parties controlling what documents and information the divestiture buyer produces to the government – with a high degree of skepticism.

Merging parties should also provide the divestiture buyer with sufficient time and resources to fully evaluate the divested assets and understand how to deploy them effectively once acquired. The agencies will evaluate whether the buyer has had sufficient time to vet the divestiture package.

Challenges to Consummated Transactions Continue

Agency staff discussed recent government challenges to consummated acquisitions under both Section 7 of the Clayton Act and Section 2 of the Sherman Act. The fact that mergers have been previously notified and reviewed pursuant to the HSR Act does not preclude DOJ and FTC from later bringing actions challenging consummated transactions.

“Mergers in Disguise” Are on European Enforcers’ Radars

Competition enforcers from Brussels and Germany observed that corporations have attempted to evade merger control by, for example, lifting competitors’ staff in lieu of a formal acquisition.

Andreas Mundt, President of the German Bundeskartellamt (Federal Cartel Office), noted that these corporate maneuvers are “mergers in all but name” and “we must think about how to deal with these types of cases and think about whether legislation is needed.” Olivier Guersent, Director-General of the European Commission’s Directorate-General for Competition, noted that he has observed “relationships between large corporations and small artificial intelligence companies that conveniently never fall into the merger regulations,” further stating that he “would like to investigate whether clever lawyers deliberately planned [to evade merger regulation].”

Robinson-Patman: Restarting Enforcement?

FTC Commissioner Alvaro Bedoya Wants to Revive Robinson-Patman Enforcement

The Robinson-Patman Act prohibits price discrimination in certain circumstances. Although the law has been on the books for nearly a century, DOJ and FTC have not brought any enforcement actions under the Act in decades.

During a panel, FTC Commissioner Alvaro Bedoya expressed strong interest in bringing cases to enforce the statute, which is consistent with past comments. According to Bedoya, his priority is to “take the [Robinson-Patman Act] car out of the garage” and bring a winning case. He stated, “What happened in 1936 is happening again today. Large powerful market players are receiving secret deals smaller retailers are not, not because they’re efficient, but because they’re powerful.”

Given the antitrust agencies’ renewed interest in Robinson-Patman enforcement, companies should evaluate their pricing and trade policies to assess risk and ensure compliance.

Noncompetes and No-Poach Agreements

The Status of the Proposed Noncompete Rule Is Uncertain

In January 2023, FTC announced a Notice of Proposed Rulemaking that would ban noncompete clauses in employment contracts. The proposed rule states that noncompete provisions in employment agreements are an “unfair method of competition” under Section 5 of the FTC Act. While FTC has not disclosed when it expects the proposed rule to be finalized, the agency reiterated that it has closely reviewed more than 26,000 comments on the rule, and the final rule will incorporate the public’s feedback.

Labor Market Enforcement Is Growing Globally

Although no-poach prosecution in the US has garnered recent attention, with DOJ and private plaintiffs bringing both criminal and civil enforcement actions, other jurisdictions, such as Canada, China and Australia, have begun to follow suit, prosecuting certain no-poach and wage-fixing agreements under antitrust and competition laws akin to those of the US. Salary benchmarking, in particular, is an area of focus for global antitrust enforcers.

Consumer Protection

FTC Rulemaking Authority Remains in Use

Samuel Levine, Director of the FTC Bureau of Consumer Protection, indicated FTC’s plans to continue using its rulemaking authority to address consumer harms, which the agency views as a more effective tool than relying solely on case-by-case enforcement. The FTC highlighted its particular focus on protecting consumers in the artificial intelligence and privacy spaces. Levine said the FTC intends to bring more Section 5 claims to pursue practices harmful to consumers.

SEC Targets Certain Proprietary Trading Firms and Private Funds With Expanded “Dealer” Definition

ARTICLE / CLIENT ALERT / US POLICY

February 21, 2024

Read time: 19 min

Executive Summary

On Feb. 6, 2024, the US Securities and Exchange Commission (“SEC” or “Commission”) adopted new Rules 3a5‑4 and 3a44‑2 (together, “Final Rules”)[1] under the Exchange Act to further define what it means to be “engaged in the business” of buying and selling securities for one’s own account and, as such, required to register with the SEC as a “dealer” or “government securities dealer,” as applicable (collectively, a “Dealer”). The Final Rules establish two non-rebuttable qualitative standards — one that targets the regularity of a market participant’s expressions of trading interest (“Expressing Trading Interest” factor, as further defined below) and another that targets a market participant’s primary source of revenue (“Primary Revenue” factor, as further defined below) — to determine if a market participant is required to register as Dealer. While the Final Rules have been significantly scaled back from the SEC’s initial proposal (“Proposal”),[2] based on the qualitative standards set forth in the Final Rules, certain private investment funds and their advisers may be required to register as Dealers.

The Commission declined to adopt the two most controversial provisions of the Proposal. The first was an additional qualitative standard that would have required any persons who “routinely [makes] roughly comparable purchases and sales of the same or substantially similar securities (or government securities) in one day” to register as a Dealer.[3] The second was a quantitative standard that would have required any person who, in four of the last six calendar months, bought or sold over $25 billion in US Treasuries to register as a “government securities dealer.” However, in what appears to be a significant expansion from the Proposal, the Adopting Release notes market participants do not need to express trading interest continuously nor simultaneously be on both sides of the market to be captured by the Expressing Trading Interest test.

Additionally, the SEC declined to adopt the broad definition of “own account” included in the Proposal, which would have required that investment advisers aggregate activity across private funds and accounts managed by the adviser. Instead, the SEC adopted a definition of “own account” that focuses on the entity engaged in the dealer activity along with an anti-evasion prohibition designed to restrict circumvention of the Final Rules.

Final Rules

As adopted, the Final Rules require that, subject to limited exceptions, any person who “engages in a regular pattern of buying and selling securities [or government securities] for their own account that has the effect of providing liquidity”[4] by engaging in the below activities must register as a Dealer:

- Regularly express trading interest that is at or near the best available prices on both sides of the market for the same security and that is communicated and represented in a way that makes it accessible to other market participants (“Expressing Trading Interest” test);[5] or

- Earning revenue primarily from capturing bid-ask spreads, by buying at the bid and selling at the offer, or from capturing any incentives offered by trading venues to liquidity-supplying trading interest (“Primary Revenue” test).[6]

While the SEC did not adopt the proposed “roughly comparable purchases and sales” qualitative standard, the SEC cautioned that such activity may still be “de facto market making under the [adopted] two qualitative tests or dealer activity under otherwise applicable precedent.”[7] Further comments in the Adopting Release and a lack of clarity on key terms may permit broad interpretations of the two adopted qualitative tests to cover some of the activities previously captured by the “roughly comparable purchases and sales” test. The Commission also emphasized that the two adopted standards are non-exclusive, meaning that market participants must continue to assess their activities against existing SEC guidance and court precedent. This may be disappointing for market participants looking for additional clarity in light of recent court cases.[8]

Expressing Trading Interest Test

Under the Expressing Trading Interest test, a person “regularly expressing trading interest that is at or near the best available prices on both sides of the market for the same security and that is communicated and represented in a way that makes it accessible to other market participants” is engaged in buying and selling securities for its own account “as a part of a regular business.”[9] While the Commission stated it adopted this test largely as proposed, it made two significant textual changes. The first was to add the phrase “for the same security” to explicitly provide in the Final Rules that the expressions of trading interest must be for the same security. The second change replaced the term “routinely” from the Proposal with “regularly.” Additionally, the Commission provided guidance on a number of terms used under the Expressing Trading Interest. This guidance indicates that the SEC may take an expansive view of what activity is captured by the test.

“On Both Sides of the Market”

While the Final Rules clarify that the Expressing Trading Interest test requires a person’s trading interest to be “on both sides of the market for the same security,” the Commission declined to require that expressions of trading interest be simultaneous or provide a time horizon over which to evaluate single-sided expressions of trading interest. The Commission explained that “participants will need to assess the totality of their trading activity to determine if they are expressing trading interests on both sides of the market for the same security sufficiently close in time to have the effect of providing liquidity in the same security to other market participants,”[10] including in determining whether their quoting activity meets the Final Rules’ “regularly expressing” standard.

“Regularly Expressing”

As proposed, the Expressing Trading Interest test would have required a person who “routinely” expresses trading interest at or near the best available prices on both sides to register as a Dealer. While the SEC noted that the term “routine” was “intended to capture significant liquidity providers who express trading interests at a high enough frequency to play a significant role in price discovery and the provision of market liquidity, even if their liquidity provision may not be continuous like that of some traditional dealers,”[11] commenters expressed concern due to a lack of clarity and ambiguous nature of the term. Rather than directly addressing these concerns through a formal definition or clear guidance, the SEC replaced the term “routinely” with “regularly,” indicating the change was intended to mirror the statutory text.[12] Notwithstanding the SEC’s note regarding its purpose, this change may result in additional activity being captured by the Final Rules. For instance, while the term “routine” indicates activity that is common and expected, the term “regular” could include activities that, while not routine, simply occur with some frequency (contrast one’s morning “routine” with “regularly” traveling for work).

The term “regularly” in the final rules will apply to a person’s expression of trading interest both “within a trading day and over time.”[13] This requirement is intended to distinguish persons engaged in isolated or sporadic expressions of trading interest from persons whose regularity of expression of trading interest demonstrates that they are acting as Dealers. The Commission was clear, however, that a person does not need to be “continuously expressing trading interest” to be engaging in a “regular” business; rather, whether a person’s activity is “regular” will depend on the liquidity and depth of the relevant market for the security.[14]

For example, while expressing trading interest “as part of an investment strategy on a one-off basis,” in a liquid market would not meet the requirements of the Expressing Trading Interest test,[15] in less liquid markets (e.g., where it is more difficult to execute orders or large orders can significantly impact the price of the security), “regular” would include the “possibility of more interruptions or wider spreads for the best available prices.”[16]

“At or Near the Best Available Prices”

While the Expressing Trading Interest test requires that quoting activity be “at or near the best available prices on both sides of the market,” the Final Rules and Adopting Release provide little guidance on this standard. Notably, statements by the SEC during the open meeting to consider the Proposal suggested that the SEC would look to the relevant facts and circumstances to determine if expressions of trading interest are at or near the best available prices.[17]

Further, in the Adopting Release, the Commission explained that, in determining whether trading interest was expressed “at or near” the best available price, market participants should look to information typically used to make bids and offers, including “recently completed purchases and sales and the totality of indications of willingness to buy or sell at specified prices.”[18]