ARTICLE

December 2025

Read time: 7 min

Key takeaways

- Professional sports represent a sought-after investment sector, with valuations continuing to climb.

- There are a growing number of investment opportunities in emerging sports like pickleball, lacrosse, and women’s soccer.

- New investors are entering space, including current and former athletes, private equity firms, and high-net-worth individuals.

- Tech investors can help sports leagues use new means to monetize IP and expand fan bases.

- Emerging sports leagues can be nimbler and more innovative in how they build visibility and reward players.

- More dealmaking in emerging sports leagues is expected in 2026.

Professional sports is currently one of the hottest sectors in the United States, as enterprise valuations of teams continue to dramatically increase. Historically, the preserve of ultra-high-net-worth individuals where investment opportunities arose once in a generation, the relaxation of league shareholding rules, and a growing appetite among institutional investors have fueled a robust and vibrant deal environment.

In August 2025, McDermott Will & Schulte represented Aditya Mittal and trustees of the Mittal family trusts as part of a buying group led by William Chisholm that acquired the National Basketball Association’s Boston Celtics for $6.1 billion. At the time, it was the largest sale of a US professional sports team in history. But the value of professional sports sector deals continues to climb, boosted by eye-popping media deals and investors attracted to stable revenue streams and loyal fan bases.

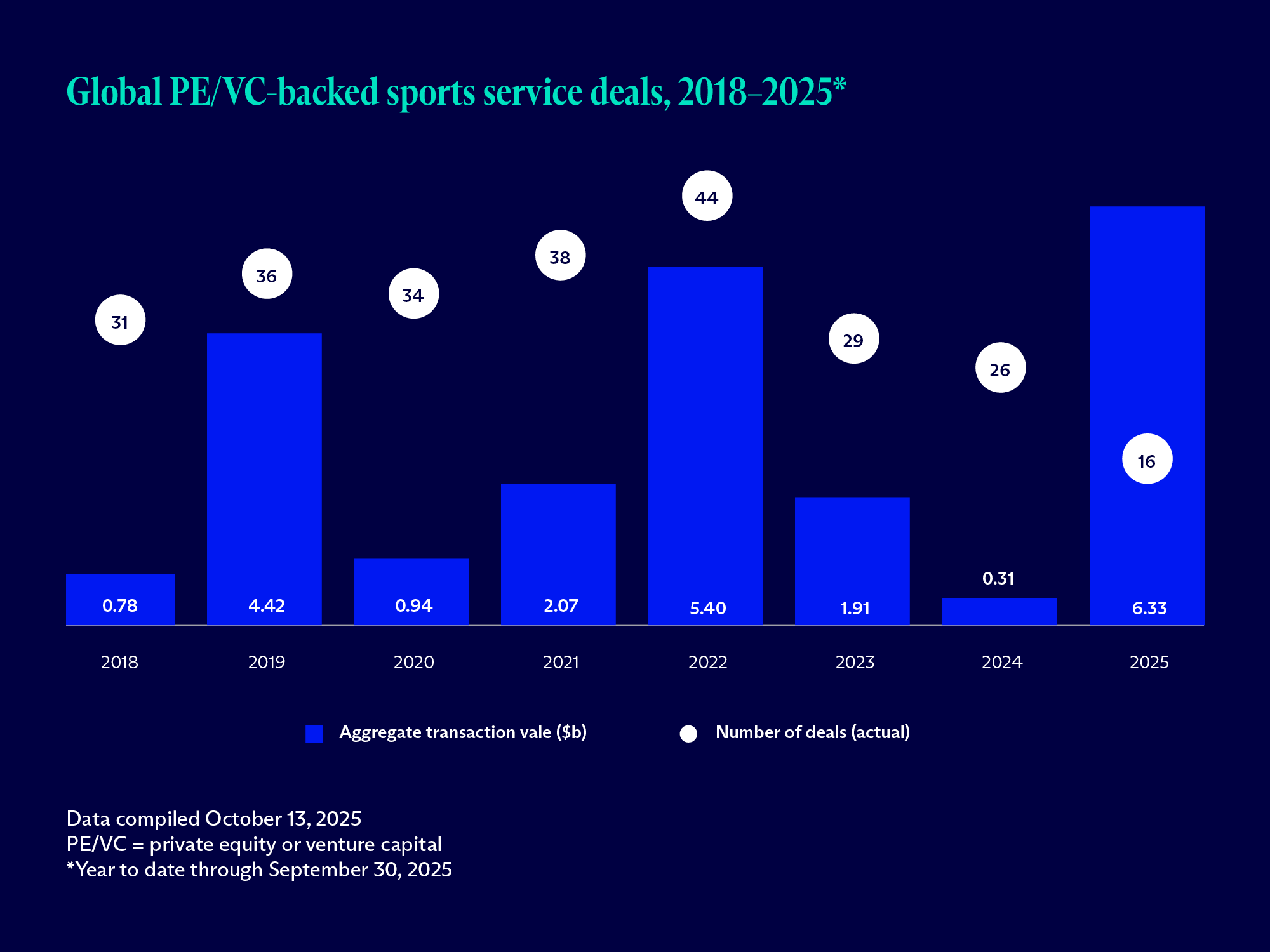

As high valuations continue to bring more sellers to market in the big four US professional sports of football, basketball, hockey, and baseball, investors that do not have billions at their disposal are starting to look deeper into the sector. We are seeing the interest in emerging sports increasing as investors continue to look for new angles and networks remain hungry for sports content to satisfy viewers.

All eyes on emerging sports

So, what are those emerging sports presenting attractive investment opportunities? Pickleball, lacrosse, women’s soccer, padel, bull riding, drone racing, and various forms of football (such as flag football, spring football, and women’s football) are all gaining momentum. We recently closed a transaction in women’s volleyball, now one of the most popular women’s sports in the US.

As the range of opportunities grows, the range of investors accessing the sector is also diversifying. Anyone with capital is now able to participate.

We have seen many deals spearheaded by current and former athletes. Magic Johnson, a Los Angeles Lakers legend, was a trailblazer in showing professional athletes that they can use their fame and money to lead lucrative investing careers once their playing days are over. As the salary cap increases across top professional sports leagues to keep up with the league’s revenue, professional athletes have more money to spend.

Smartly, and with the right advice, athletes are realizing that with any investment, starting earlier is better. Even before making it to the professional ranks, name, image, and likeness (NIL) deals are affording college athletes the ability to make money and subsequently invest where they see fit, including in emerging sports.

Paige Bueckers, while a star on University of Connecticut’s women’s basketball team, received equity in Unrivaled, the three-on-three basketball league, in connection with signing an NIL deal.

Not only do current and former athletes have capital, but they also add value to these leagues. For example, Houston Rockets forward Kevin Durant and tennis pro Naomi Osaka are becoming the unofficial faces of pickleball while former professional women’s basketball player Candace Parker’s investment in the National Women’s Soccer League’s Angel City FC allows them to leverage her personal brand and increase visibility for the team.

Private equity firms, which have entered the top US sports leagues in the last five years, are also starting to enter emerging sports. We have already seen deals completed in the National Women’s Soccer League, the Professional Fighters League, lacrosse, padel, and SailGP, the new global sailing competition.

There is a growing opportunity for high-net-worth individuals, too. While ownership in the top sports leagues is reserved for those with net worths over the billion-dollar range, individuals who have substantial wealth at a slightly lower level are using emerging sports as a new way to deploy capital.

The rules of the major professional sports leagues include express protection for control owners to ensure team and league stability. Private equity investors must hold passive stakes and, in general, most control owners would prefer that any new investors in their capital tables take a passive role.

By contrast, emerging leagues are looking for active investors that can help them grow the sport. Synergies via partnerships, brand recognition, and past success in the sports business arena are characteristics that emerging sports leagues are looking for in an investor.

Technology in sports

Successful Silicon Valley tech investors have become a large portion of the investor pool for sports teams because of their accomplishments, capital, and ability to provide synergistic value. Sports are intellectual property (IP), and technology is the most efficient method for monetizing this IP.

Technology connects people so that a league based in the US can establish a global audience. The technology can be as straightforward as having players mic’d up during a game or as in-depth as using artificial intelligence to obtain fan data that can subsequently be used to pitch sponsorships, enhance the fan experience, and direct marketing according to fans’ personalized data sets.

A win-win opportunity

The major professional sports leagues are firmly established, but emerging sports leagues have the room and passion to innovate and shape their sports – both on the field and off – to cater to a modern audience. Like the top sports leagues, media contracts will be a significant driver of success. With the right visibility, an emerging sports league can explode overnight.

There is no better example than pickleball. Rarely do you find a sport that can be played by both a 70-year-old and a 10-year-old. Pickleball is popping up all over the country, including on our TVs, and investors see an incredible opportunity to monetize that.

With the right visibility, an emerging sports league can explode overnight.

Certain emerging sports leagues, like the Premier Lacrosse League, which recently signed a long-term contract with ESPN, are sharing the league’s upside potential with their players via creative player equity participation programs. These are possible because emerging sports leagues are more nimble, less focused on rules and regulations, and more focused on pure growth. The lack of league red tape allows emerging sports leagues to scale at a faster rate with rapid decision-making.

Conclusion

The top professional sports leagues are not taking their foot off the gas, and fighting for fan time, attention, and money will not be easy for emerging sports leagues. But these new leagues are taking advantage of a fast-evolving media landscape that provides multiple ways for fans to consume sports in order to break through to their fan base.

These emerging leagues are looking for enthusiastic, proven, strategic investors to help them find and expand their market, and investors are increasingly looking for these opportunities to get in on the “next big thing” in sports. We expect more deals to take place in 2026 as dealmakers broaden their horizons and the scope of the opportunity within the sports sector continues to rise.

At McDermott, we know sports are more than just games—they’re global businesses, cultural touchstones, and platforms for innovation. Our sports law team works at the intersection of law, business, and culture, guiding clients through regulatory challenges, advising on high-profile transactions, managing labor matters, and addressing critical IP issues.

In the past year, McDermott has advised on transactions totaling almost $10 billion in value. Beyond structuring transactions, we help clients create lasting value that extends well beyond the season.

Hedge fund developments: Portable alpha and SMAs

ARTICLE

December 2025

Read time: 7 min

Key takeaways

- Insurance dedicated funds and rated feeders dominated hedge fund formation activity in 2025.

- There is continued interest in portable alpha strategies that capture both alpha and beta returns.

- Portable alpha strategies can be structured in several ways, each with different cost and contagion risk implications.

- Managers must consider different approaches to mitigating fiduciary risks and fee arrangements.

- SMAs continue to be widely deployed.

- Liquidity terms, contractual arrangements, expense allocations, and hurdle rates are all focus areas when negotiating SMA solutions.

Portable alpha strategies: Legal and structural considerations

While insurance dedicated funds and rated feeders dominated specialized fund formation activity in the hedge funds market throughout 2025, portable alpha strategies are of growing interest. Favored by certain sovereign wealth investors looking for one-stop-shop solutions, they allow investors to simultaneously capture alpha and beta returns within a single investment vehicle. We expect to see more demand for them in 2026.

Portable alpha strategies allow investors to capture alpha and beta returns within a single investment vehicle.

Understanding portable alpha

The term “portable alpha” is something of a misnomer. Rather than truly “porting” alpha, these strategies import beta market returns using swaps or futures from one investment source and combine those returns with alpha exposure from the manager’s actively managed fund(s).

Portable alpha is increasingly relevant in today’s investment landscape, with clients frequently inquiring about its implementation and structure. These strategies are designed to allow investors to enhance returns by capturing alpha independently while maintaining traditional market exposure via beta returns.

Structural options and risk considerations

Structuring portable alpha strategies involves balancing efficiency against fiduciary and legal risks. One key concern from a structuring standpoint is contagion risk, or the possibility that adverse movements in beta exposure might spill over and impact the alpha component.

Three principal structural approaches exist to deliver these strategies. First, managed accounts and funds-of-one present few legal or fiduciary issues and are easy to set up. They do, however, bring in additional costs and complexities when replicating alpha trades, and the only capital used to support the beta exposure is the single investor’s capital.

Another option is the class structure, which is the most cost-efficient option because everything resides in the same fund. Simply creating a new class presents the most contagion risk of the three options due to the proximity of the alpha and beta components.

Finally, separate feeder funds are also being used, which can provide a balance between legal risks and capital efficiency, especially if some amount of cash is held back at the feeder fund or intermediate fund level. While cross-class risk can still raise concerns with a separate feeder fund model, the cash provides a cushion should the beta component need additional capital during market turmoil.

Mitigating fiduciary risks

If a manager builds a fund-of-one for an investor to employ their portable alpha program, no novel fiduciary issues will be presented. However, if a manager seeks to bolt on a portable alpha program to an existing fund, important fiduciary concerns must be addressed because some (or all) of the remaining investors will not participate in the portable alpha strategy. The risk would be the potential for the portable alpha strategy to impact the existing fund and its investors in some adverse way.

Fund managers employ various approaches to address fiduciary concerns in these strategies, including limiting the size of portable alpha classes or feeders to control exposure, implementing fee arrangements where portable alpha investors compensate other investors for structural benefits, or establishing clear margin call procedures.

Managers must also document risk disclosures comprehensively. However, these measures only mitigate – and cannot eliminate – the inherent risks of these portable alpha strategies.

Fee structures and new trends

Fee arrangements for portable alpha strategies remain nonstandardized, reflecting their evolving nature. Some managers apply traditional hedge fund fees solely to the alpha component while others charge fees on net returns across the entire structure. We also see the use of hybrid approaches, with incentive fees on alpha and management fees on both components. Managers will need to ensure offering documents accurately reflect the fee calculation methodology.

One new trend is the offering of multiple beta options by managers. Each investor can choose which beta they wish to import and blend into their alpha returns. The manager must structure these options carefully to avoid cross-class liability, which could be created between classes in a single legal entity.

As these strategies continue gaining traction, market standards remain fluid and structures reflect the bespoke requirements of managers and investors.

The evolution of separately managed accounts

Separately managed accounts (SMAs) have undergone a profound transformation in recent years, evolving into an essential component of the fundraising and investment management landscape. As portfolios of securities managed on behalf of single investors, SMAs give investors direct ownership and custody of underlying securities.

Investment managers of varying sizes, vintages, and investment strategies now routinely manage significant amounts of capital in SMAs. This represents a marked shift over the past decade, prior to which SMAs were often viewed as secondary to commingled fund structures and funds-of-one.

While capital providers such as seed and anchor investors previously invested primarily in commingled fund structures (with side letters), they now frequently deploy capital via SMAs. We also see large investors in commingled funds negotiating for a right to convert some or all of their commitment to an SMA.

The use cases for SMAs have also expanded dramatically. These vehicles have become extraordinarily common in securing initial capital for emerging managers, and large multistrategy managers often use these structures to deploy significant capital to external managers to fill strategy gaps.

Further, while SMA structures are often best suited to liquid strategies, such as investments in publicly traded securities, they are now being considered for, and utilized in, more co-investment structures and less liquid strategies. That is something we did not see a decade ago.

Legal and commercial considerations

One reason for the growing adoption of SMAs has been the market shift to align liquidity terms, including termination rights and the ability to decrease notional trading value, with those of parallel commingled funds and other SMAs.

Historically, SMA clients often demanded preferential liquidity compared to parallel commingled funds, creating fiduciary complexities and operational challenges for managers. Now, more aligned liquidity terms are more commonly agreed, reducing the risk of misalignment and ensuring fair treatment across investor types.

The contractual terms of SMAs have also become more sophisticated. Parties now devote significant attention to leverage and financing mechanics, including how the cost of financing is allocated and how those costs are factored into management and performance fees.

Expense allocation is another area of focus. Historically, SMA investors often paid fewer expenses than their commingled fund counterparts, leaving managers to absorb the shortfall. That is no longer the case. We have also seen an increasing customization of how fees are calculated, including hurdle rates, which may be gauged against benchmark or absolute returns.

The SMA has evolved into a flexible, institutionally accepted investment structure that is attractive to both asset managers and investors. Whether as part of launch capital, a platform deployment tool, or a bespoke co-investment arrangement, we believe they will remain popular, offering tailored solutions in an increasingly complex investment landscape.

Conclusion

As we move into 2026, we expect more demand for portable alpha strategies that allow investors to capture both alpha and beta returns. Sovereign wealth investors looking for one-stop-shop solutions prefer portable alpha strategies because they can be structured in several ways to address different cost and risk concerns.

SMAs will also continue to be a popular tool, as investors increasingly seek bespoke arrangements as they deploy capital into private markets. With the terms of SMAs evolving and being hotly negotiated, managers will be paying close attention to market trends.

European real estate: A market ready to mobilize

ARTICLE

December 2025

Read time: 7 min

Key takeaways

- European real estate investors are preparing for more activity in 2026, with an acceptance that macro headwinds are now risk-allocated like any other underwriting consideration.

- Debt capital is available, but high-quality new money deals are intensely competitive.

- Effective risk assessment cannot rely on AI alone; personal connections and long-term partnerships are just as important.

- More capital is flowing into Europe from Australia, Canada, and Japan.

- The logistics, healthcare, life sciences, and living sectors are set to be the key beneficiaries as capital mobilizes.

- Increased defense spending across Europe will likely fuel infrastructure and logistics activity.

As we entered the final quarter of 2025, there was a sentiment shift within the European real estate investment landscape as industry leaders began to act despite ongoing geopolitical uncertainty.

There continues to be discussions around the evolution of risk assessment, shifts in capital flows toward European markets, and the enduring appeal of the logistics and living sectors. Further, as the market continues to regain confidence, we are noticing personal connection and trust being deemed essential for effective risk allocation and investment decisions.

Shifting sentiment: From caution to action

Sentiments over the past few years have been defined by a restraint on investor confidence due to geopolitical and wider macro uncertainty. The outlook was defined by caution and survival until such headwinds eased.

While those themes of caution and survival have not been confined to the past, we now see the return of optimism as we move toward 2026 and some mobilization toward action in the real estate investment and debt markets.

Despite certain markets and geographies remaining dislocated, there is an increasing acknowledgement that within a new world of greater pragmatism and the acceptance of geopolitical uncertainty, macro headwinds can now be risk-allocated, priced in, and inform rather than deter transactional activity.

Mobilization resulting from this mindset shift may take time to translate into pre-COVID-19 transaction volumes as the management of, and appetite for, risk is likely to influence the speed of and approach to transactions. Nevertheless, what we are hearing heralds an important vote of confidence in the fundamentals of the European market.

The debt landscape

While underlying transaction volumes are increasing, the small number of high-quality new money deals that come to market are aggressively brokered.

In this competitive landscape – and in the context of non-core deals – lenders who can blend different sources of capital, including cheaper insurance money, are well placed to secure mandates.

The comparative scarcity and pricing pressures of deals are increasingly forcing lenders to deploy tickets in the lower mid-market (€30 million – €50 million), where execution speed and the ability to underwrite more transitional business plans are highly prized.

As capital raising pressures slowly ease on managers with an allocation to credit, lenders continue to favor asset classes that benefit from structural undersupply combined with compelling debt-entry points.

The evolution of risk assessment

In a market regaining its confidence, it is clear that (more than ever) careful and considerate risk management will be a major influence on transaction activity.

Institutional capital remains attracted to asset classes where operational excellence and expertise drive value and returns. Meanwhile, the need for such capital to partner with sector-specific operators is fueling a rise in risk-sharing transaction models, joint ventures, co-investments, and secondaries.

The usual fundamentals of site selection, due diligence, and realistic transaction timetables remain important, but we are seeing the market focus much more heavily on personal relationships as the key to risk management.

While artificial intelligence (AI) may allow elements of investment due diligence to be accelerated, it cannot replace personal connection and accumulated trust. Confidence in investing via long-term partnerships requires cultural and personal alignment, and there is a palpable sense that nothing replaces the need to build deep and informed connections between parties to inform risk decision-making.

A market redrawn to embrace the new normal

So, in a market ready to mobilize, how will a return to optimism translate into activity?

First, there’s been a growing allocation toward European markets from global sources of institutional and sovereign wealth capital that will make a meaningful difference.

Flexible, tech-enabled, sustainable buildings are likely to attract such capital, enabling deployment at scale in familiar and stable markets.

Sector-wise, there are signs of improvement in the office markets, but the logistics, living, and healthcare sectors continue to dominate opportunities.

From a logistics perspective, whether through a combination of supply chain changes driven by the impact of AI and automation, a continued evolution and sophistication of logistics to meet customer demand, or a need to prepare for the anticipated growth in data center capacity, logistics will be at the heart of investment activity going forward. Our recent work for a managed fund of Invesco Real Estate on the formation of a joint venture with Logistics Capital Partners to acquire and develop an 800,000 sq ft logistics park in Thamesmead, London, is a case in point.

In the living and healthcare sectors, demographics and societal changes will continue to drive investor appetite. As populations live longer and become accustomed to home ownership no longer being a barometer of personal prosperity and status, the need for the living sector to adapt is resulting in the advent of options beyond traditional build-to-rent.

Single-family rental and senior living are comparatively underdeveloped asset classes, and we expect to see increased allocations to these subsectors. Meanwhile, affordability issues in the purpose-built student accommodation sector may yet lead to more investments in portfolios of homes in multiple occupancy.

From a healthcare perspective, the fourth quarter of 2025 has seen major deployment of capital by US healthcare real estate investment trusts in the care home space, and we expect further consolidation and activity across the healthcare real estate sector, attracted by the impact on average life expectancy from medical advances and other supportive demographics.

Finally, while we have yet to see the implications of increased defense spending across Europe, it is a major focus. Outside of the need for more manufacturing capacity, existing and new supply chains must be developed and adapted to facilitate the political shift in priorities. As with other sectors, it will be critical that infrastructure spending from both public and private sources keeps pace and enables rather than frustrates development.

Conclusion

Although encouragement can be taken from the gradual increase in market confidence and pragmatism, the most important theme among European real estate investors is the enduring power of personal connection and trust as the bedrock of investment.

The most important theme among European real estate investors is the enduring power of personal connection and trust.

We see a market ready to do business, but effective risk allocation is more critical than ever. In a world where the operationalization of real estate continues at pace, getting closer to, understanding, and leveraging the expertise of investment partners cannot be outsourced or automated – and that is something the sector is doubling down on going into the next wave of activity.

Setting the private capital compass for 2026

ARTICLE

December 2025

Read time: 5 min

Key takeaways

- Private capital strategies are evolving around a more unified, solutions-driven toolkit.

- Dealmaking saw a rebound and private market expansion continued in 2025.

- Private capital has proven its role as a stabilizer during uncertain times.

- Adaptability and creativity will be key going into 2026.

- Refinancings and liability management will be major themes in the coming year.

- Underpenetrated European markets will draw more attention and cross-border growth will continue.

- Origination quality and execution infrastructure will be decisive going forward.

As we consider the key developments that occurred in 2025 and look ahead to 2026, one theme dominates: the maturation of private capital as a truly integrated asset class. The old silos between private equity, private credit, and hybrid strategies are steadily eroding, presenting a mixture of solid foundations and fresh dynamics.

The most sophisticated investors are no longer defining themselves by the instruments they use but by the outcomes they deliver: control, alignment, and return in a world where capital is private by design. For senior practitioners and investors alike, they are tasked with separating meaningful change from noise and calibrating their strategies accordingly.

The past year has been marked by consolidation, calibration, and cautious optimism. The asset class delivered continuing proof of its resilience. As one KKR insight put it, private capital is doing “exactly what investors hoped it would in a year like this: providing strong, floating-rate yield and acting as a shock absorber from market volatility.”

On the equity side, global buyouts reversed a two-year slide and dealmaking began to recover. That recovery is further likely to be boosted by the prospect of rate cuts and an improving macro narrative. Private markets continued to expand, with total global assets under management expected to reach more than $20 trillion by 2030, according to a leading global asset manager.

Private capital as a stabilizer

These figures tell a simple story: Capital remains private because it can act with agility, and in times of uncertainty that independence matters. Private capital has again proven its role as a stabilizer. It has financed growth, managed liquidity, and stepped in where traditional lenders or public markets are constrained. The discipline of the asset class, combined with the flexibility of structure, has allowed businesses to navigate a complex environment with confidence.

However, this year was far from seamless as persistent inflation, elevated interest rates, and macropolitical tensions significantly influenced market behavior. Reports indicate nearly a third of firms were renegotiating pricing or structure in 2025, and a similar proportion of portfolio companies reassessed valuations. The engine kept running, but the road was uneven – proof that private capital’s strength lies as much in its adaptability as in its momentum.

As we look ahead to 2026, the need for adaptability will once again be paramount. Deployment will remain selective, favoring borrowers and sponsors who offer genuine alignment, optionality, and partnership. Capital will flow not merely to scale but continuingly to quality and those who can demonstrate resilience and clarity of purpose. The distinction between private equity and private credit will blur further as hybrid instruments and flexible capital structures continue to evolve. Borrowers and investors will continue to treat the capital structure as a dynamic toolkit rather than a fixed hierarchy.

Liquidity solutions remain crucial

Refinancing and liability management will also be very active. With maturities approaching and refinancing windows unevenly distributed, liquidity solutions, recapitalizations, and hybrid instruments will continue to drive origination. This is not the exuberant expansion of prior cycles; it is a more deliberate, technical phase of market evolution defined by structural sophistication and more disciplined execution where financiers hold their risk instead of syndicating it.

Geographically, might the focus tilt toward underpenetrated regions within Europe where private capital can scale most efficiently? Fragmentation, once viewed as a deterrent, is increasingly an opportunity for differentiation and local expertise, particularly where cost savings and synergies alone cannot drive valuation increase. In terms of sectors, capital will gravitate toward businesses with recurring revenues, pricing power, and technological or healthcare adjacencies while more commoditized industries will remain subdued.

In this environment, origination quality and execution infrastructure will be decisive. With abundant capital chasing few high-quality assets, the advantage lies with those who can source proprietary opportunities, underwrite intelligently, and deliver efficiently. The combination of local knowledge, institutional process, and global reach will set apart the market’s true leaders, as might scale in certain parts of the market.

Conclusion

In short, we believe that 2026 will not be about “faster, bigger” but “sharper, smarter.” Those who deliver capital with clarity of purpose, structural alignment, and operational agility will be successful. For borrowers, whether sponsor-backed or independent, this means championing capital partners who bring not only money but also insight, speed, credibility, and a genuine partnership mindset.

2026 will not be about ‘faster, bigger’ but ‘sharper, smarter.’

Private capital was tested in 2025 and passed. The question for 2026 is whether private capital can now excel. For those who get the structural basics right, the opportunity remains compelling. The market may be private, but the lessons it teaches about partnership and purpose are universal.

Transatlantic restructuring trends: What to expect in 2026

ARTICLE

December 2025

Read time: 9 min

Key takeaways

- It has been a tumultuous year, with modest economic growth with a continuing steady flow rather than a new wave of restructurings.

- Tariffs, layoffs, and industry-specific structural weaknesses are projected to constrain US economic growth in 2026.

- Private credit became more influential in US restructurings, and LMEs continued to shape US markets.

- In the UK, trends were similar to those in the US, with steady growth in private credit.

- France witnessed a record level of insolvencies in 2025, and 2026 looks set to be similar.

- The German economy has been feeling the pressure, with insolvencies of large companies increasing.

- Restructuring activity is likely to increase in 2026, but not at systemic levels and with varied impacts across markets.

In a turbulent year defined by a return to a more protectionist approach in the United States, tariffs remain a work in progress. Their impact has been felt everywhere, particularly on global supply chains and input costs, causing inflationary pressures for both businesses and consumers and creating difficulties for business planning. Still, the worst trade war fears have fallen away, and the global economy has shown itself to be remarkably resilient (notwithstanding some of the shocks experienced this past year).

Economic growth has been modest and is likely to continue to be so in 2026, eased by a slight fall in interest rates, particularly in the G7 countries. We have thus far avoided a recessionary environment and, while there is a steady flow of corporate restructurings, the long-anticipated wave has yet to materialize.

Investor confidence in technology – specifically artificial intelligence (AI) – remains strong and has done a lot to sustain equity markets, but there are voices urging caution and fears of a correction. Other concerns remain, including conflicts in Russia/Ukraine and the Middle East, but these have also driven spending on defense, energy security, and wider innovation.

Many countries are experiencing political instability and fiscal challenges that impact business confidence. However, given the challenges, 2025 turned out to be better than expected. Forecasting for the coming year remains cautiously optimistic.

Restructuring activity is likely to increase in 2026, but not at systemic levels and with varied impacts across markets.

US market dynamics are evolving

The prevailing view of the 2026 US economic outlook is cautious optimism. Inflation has cooled from its 2024 peak, consumer spending remains steady, and the technology sector continues to anchor growth.

Yet risks are evident: Tariffs burden manufacturing and agriculture, and mass layoffs at behemoths, including Verizon, Amazon, and UPS, indicate fragility in the labor market. Structural weaknesses in commercial real estate, healthcare, and automotive manufacturing persist while fiscal and political uncertainty clouds investor confidence. Consensus predictions point to moderate growth, with volatility likely a defining feature of 2026.

Private credit has expanded rapidly, offering flexible alternatives to traditional lending and reshaping the restructuring landscape. Moody’s projects global private credit assets under management will reach $3 trillion by 2028, driven largely by US and European growth. Institutional investors fuel middle market and distressed financing while banks remain constrained by regulation and risk appetite. This shift positions private credit as a growing influential presence in restructurings.

Companies continue to use liability management exercises (LMEs) to manage debt burdens, leveraging loose documentation and abundant capital. Borrowers deploy creative structures to extend maturities and preserve liquidity. While these techniques have drawn scrutiny and litigation, they remain a favored tool for parties seeking solutions outside formal proceedings.

Chapter 11 remains the cornerstone of corporate restructuring in the US, but its role is evolving as companies weigh costs, timing, and creditor dynamics. Large-cap debtors often pursue pre-packaged or pre-negotiated filings to minimize disruption while out of court solutions – from exchange offers to LMEs – compete with formal proceedings.

Simultaneously, debtors are increasingly exploring foreign jurisdictions with lower costs and fewer hurdles, underscoring the global dimension of restructuring strategy. The result is a market defined by flexibility and competition, where both debtors and creditors must adapt to an expanding toolkit.

A mixed UK outlook

The UK government, though committed to economic growth, has been beset with social and political pressures that have aggravated some of its fiscal challenges. Some government decisions are controversial and impact business confidence, with the recent Budget 2025 speech providing for substantial increases in the personal tax burden of many employees, savers, and pensioners.

The government is also rolling out reforms to employment legislation, which, taken with the added cost to employers of national insurance contributions, many fear will lead to greater unemployment and dampen entrepreneurship. However, modest economic growth has occurred and is expected to continue in the coming year.

2025 has seen steady growth in private credit. Certain sectors of the UK economy are showing more stress and vulnerability, and there is some anecdotal evidence of direct lenders being better prepared to enforce.

As interest rates have begun to ease, there is also evidence that competition for deals will rise. As with the US, there is a concomitant increase in LMEs to reduce debt burdens by corporate borrowers, facilitated by the “cov-lite” nature of much of the finance documentation. But borrowers and lenders are aware of the litigation risks and uncertainties.

There has also been a pushback in the origination of new finance documentation against liability management, with the introduction of embedded contractual defenses (referred to as LME blockers).

London remains a center for international restructuring, particularly where there is an English law element in the finance documentation or where there has been a shift in the center of main interest. The introduction of a restructuring plan under Part 26A of the Companies Act 2006 in 2020 and the ability to cross-class cram-down has added to the UK market’s attractiveness.

However, in 2025, there have been a series of cases focused on the treatment of out-of-the-money creditors and the extent to which they should share in the benefits of the restructuring, and this has generated some market uncertainty. To address this, a new practice statement was introduced in September 2025 and one case, Waldorf, is heading for the UK Supreme Court.

France sees record insolvencies

As expected, France saw a record level of insolvency proceedings in 2025. Experts anticipate that by the end of the year, the number of insolvency proceedings will reach 67,500 (23% up on the 2016 to 2019 average).

The trend for 2026 is likely to be similar: The economic landscape remains gloomy, with a slow increase in gross domestic product and the political and geopolitical environment remaining unstable.

The most severely hit sectors are construction, hospitality and catering, retail, and business-to-business services. In terms of jobs at stake, the industrial sector suffered the biggest hit with 16,000 jobs directly impacted by the opening of insolvency proceedings during Q3 2025, 20% of the total for Q3 2025. That is the result of an ongoing decrease in domestic production and demand, in contrast to production overcapacities elsewhere and high energy costs impacting domestic competitiveness.

We expect 2026 to bring a challenging environment where the availability of strong restructuring tools will be helpful. In this respect, the use of accelerated safeguard proceedings (sauvegarde accélérée), which allow for the implementation of restructuring plans via a cross-class cram-down of creditors and shareholders, has proven to be an efficient way to quickly implement major financial restructurings and preserve value for stakeholders that remained in the money.

Some great examples include the Atos SE restructuring implemented in October 2024, the restructuring of offshore services group Bourbon in July 2025, and the restructuring of childcare service provider People & Baby in March 2025. LME schemes are closely watched by the market, as Altice ran the largest LME scheme ever in Europe in 2025, showing the tool could prove efficient in France.

The German economy feels the pressure

The German corporate restructuring market is entering a phase defined less by a broad insolvency wave and more by structural, proactive transformation. The current economy continues to feel pressure from high operating costs, geopolitical instability, and industrial transformation. The number of insolvencies among companies with more than 1,000 employees has increased noticeably, particularly in the second half of the year, and this trend is expected to continue in 2026.

Restructuring activities, particularly in the automotive, engineering, and chemical sectors, focus on operational efficiency, capacity adjustments, and site closures. Across all industries, large-scale employee restructuring is taking place. This trend is set to continue into 2026 in certain industry sectors driven by the delayed – but persistent – need for companies to adapt their business models.

A significant development is the accelerated growth of private credit as an alternative source of capital in distressed and special situations. Facing tighter regulatory constraints and capital requirements, traditional bank finance is increasingly risk-averse, especially in the current economy.

This vacuum is filled by private debt funds offering flexible, bespoke rescue financing, bridge loans, and refinancing solutions, particularly for the small- and mid-market. This means restructuring transactions could become more complex, involving more non-bank creditor groups in the future.

LME remains a technique of continued interest. The German equivalent – the Stabilization and Restructuring Framework of Companies Act (StaRUG) – is a recognized tool for preventive reorganization, offering debtors a discreet, nonpublic path to restructuring. In 2025, there were several prominent cases, such as BayWa AG and Varta AG.

It is worth mentioning that StaRUG is also being used for purposes beyond pure financial restructuring, such as the entry of Porsche AG as an investor of Varta AG and the squeeze out of all existing stockholders. However, there remain practical issues relating to the use of StaRUG-plans, specifically concerning establishing legally robust valuation methodologies to enable cross-class cram-downs.

Conclusion

Some 2025 themes will continue to characterize the coming year, most notably cautious optimism driven by confidence in liquidity, AI, and tech, balanced against concerns over ongoing tariff reform, political instability, fiscal challenges, regional conflict, and the risk of a correction.

While a major surge in restructurings is improbable, overall activity is trending upward, and impact varies by market.

Avoiding pitfalls as litigation finance takes off

ARTICLE

December 2025

Read time: 7 min

Key takeaways

- Litigation finance looks set for a busy year in 2026 after some uncertainties throughout 2025.

- Sitting at the intersection of law and finance, litigation finance deals include unique complexities.

- Deals collapse for many reasons, but often because of trust issues, misunderstandings, or time delays.

- Building trust at the outset, carefully negotiating deal terms, and clear responsibility schedules can help mitigate risks.

- There are some new regulatory intricacies that will also impact the litigation finance market in 2026.

- With new capital providers entering the market, it is important to be aware of common reasons for deal failure.

2025 was a challenging year for the litigation finance market, as fears of tax changes in the Trump administration’s One Big Beautiful Bill Act threatened to materially impact returns. However, as those plans failed to survive the parliamentarian’s review, the final quarter of 2025 saw a significant spike in activity, and the appetite among private funds and other new sources of capital for investing in legal claims continues to scale.

Litigation finance sits at the intersection of law and finance and, while it has some similarities to other private credit and equity models, it carries unique complexities. These deals offer investors the prospect of attractive returns that are largely uncorrelated to other asset classes or the broader capital markets, but they sometimes fall apart because of trust issues, misunderstood terms, and delays.

The three pitfalls of litigation funding transactions

The typical litigation finance deal starts with the receipt of term sheets that lay out some material economic and noneconomic terms but, importantly, not all the particulars. Usually, these term sheets are highly negotiated, include an exclusivity period, and, on occasion, a break fee.

Once these term sheets are fully executed, funders start spending money to document the transaction and finalize the diligence. The clock to closing officially starts ticking. Sometimes litigation finance deals die because of reasons beyond anyone’s control (e.g., the diligence does not stand up to the funders’ expectations, the economics simply cannot work, or business conflicts are discovered).

But transactions often collapse because of one of three reasons:

- A lack of trust among the parties

- A misunderstanding of the deal terms

- Time (shout out to the old adage, “Time kills all deals.”)

With awareness and effort, these common issues can often be avoided.

Building trust

Skilled businesspeople and lawyers can protect against many risks in a transaction, but, at some level, there is always a leap of faith. Deal documents can outline clear obligations for each party and consequences for bad behavior, but no transaction is riskless.

Since litigation finance deals often last years, it is essential to build trust throughout the negotiation process and foster a sense of ongoing goodwill and teamwork. If one party is acting with opacity or is clearly resistant to fairness, distrust can creep in and lead to deal hesitancy or failure. Acting in good faith and with transparency throughout the negotiation process can help mitigate concerns.

Promoting trust starts at the term sheet phase. The financed party must be honest about any known flaws of an investment opportunity right from the outset. No opportunity is perfect, but funders don’t expect or require perfection. They do, however, expect forthrightness.

On the other side, funders benefit by laying out the complete economics and providing a sense of all the expected major sticking points that may be further addressed in more robust documentation.

For example, if the financed party has learned a material negative fact about the case to be funded that affects its merits, it should disclose that. If some claims are weaker than others or information has come to light indicating a lower likely recovery than initially expected, the financed party should disclose that, too.

There is nothing more likely to create problems for both parties than a late-stage unwelcome surprise in the deal terms.

A common understanding

In the litigation finance industry specifically, it is common that the recipient of funding does not engage in these types of deals on a regular basis. Therefore, the terms laid out in a term sheet can be easily misinterpreted or not fully understood by the user.

Well-developed term sheets can save deals. It is better to have the hard conversations upfront before fees are racked up and time ticks away. Specifically, funders should share an economic model to promote understanding. A discussion of ongoing obligations and events of default can also be helpful to ward off difficult conversations once the deal has already started to move.

Legal transaction structures are fluid, and no two deals look alike. In fact, there are very few document templates available for litigation finance deals because each one is highly tailored to fit a particular set of circumstances.

It is crucial to understand each participant’s motivation in a deal to promote alignment of interests, both in terms of economics and process. Discussing the expectations at each step of the investment at the start of the deal is essential to success.

In addition to understanding the economics, both parties would benefit from the financed party’s understanding of the various obligations it will be required to perform under the transaction, such as reporting, reimbursement of various expenses, and other covenants.

For example, financed parties will have to report on the case’s progress. They must agree to cooperate with the prosecution of the case, provide information to experts, prepare for depositions and testifying in court, and not take actions that could adversely affect the likelihood of success.

Many of these obligations are often new to the financed party and can seem daunting at first. A clear understanding of these obligations and what internal resources will have to be dedicated to complying with them will help avoid foot faults.

Time matters

Time is the ultimate deal killer. All dealmakers are humans and people can lose conviction and motivation as transactions drag on. Other opportunities may arise for funders that can cause a distraction, and funded parties can get cold feet, leading to distaste of already negotiated deal terms. It is to everyone’s benefit to move transactions along as quickly and efficiently as possible.

Nobody likes false deadlines but setting and communicating realistic timelines – and meeting them – is essential to deal success. Efficiently responding to due diligence requests and clearly communicating timing of deliverables can be powerful predicates for a positive working relationship.

Sometimes, a time and responsibility schedule helps everyone stay on track by laying out each deliverable, the responsible party, and the date by which the parties expect to receive it. Such a tool does not have to be inflexible and, while the time frames might be aspirational at times, the parties should aim to set achievable goals.

The lifespan of these investments can be long, often three to six years. Setting the right tone early can only help the ongoing working relationship and make the parties excited to close a deal and work efficiently toward the end goal.

Time is the ultimate deal killer.

The regulatory landscape

Going into 2026, several new pieces of legislation are poised to take effect that will impact the litigation finance market in the United States and require careful navigation. For example, new rules in various states oblige litigation funders to register with the state and make funding agreements discoverable.

Further, in California, a new law prohibits lawyers from sharing contingency fees with “alternative business structures.” It is key to any litigation finance transaction for all parties involved to understand any regulatory implications depending on the jurisdiction of the investment and underlying matters.

Conclusion

As new pockets of capital continue to enter the litigation funding market and activity looks set to rebound after stalling briefly in 2025, the year ahead should be a busy one. The unique structure of litigation finance deals can lead to challenges, however, so it is vital to keep common causes of deal failure in mind when embarking on new transactions.

The trends shaping cross-border M&A in 2026

ARTICLE

December 2025

Read time: 6 min

Key takeaways

- Megatrends around international trade flows, energy transition, technology, and critical minerals that are driving M&A strategies are accelerating.

- We will likely see more large-scale carve-outs in 2026 as strategics gain clarity on ultimate outcomes.

- State investments motivated by national security threats will also shape the market.

- Private equity buyers will be well-positioned to capitalize on new opportunities that emerge.

Cross-border mergers and acquisitions (M&A) are typically driven by strategics’ specific competitive needs and a combination of attractive targets and financing for private equity acquirors. Looking forward to 2026, however, it appears that much broader macro factors are likely to have an impact on cross-border M&A activity.

The world is in the process of adapting to several disruptive megatrends that are occurring simultaneously. International trade is shifting away from its focus on globalization that has been dominant since the 1980s. Western governments are gradually viewing critical mineral supplies as a national security issue. The energy transition toward renewables continues (albeit in an evolving form). Generative artificial intelligence and other advanced technologies are driving a global digital infrastructure arms race. Underlying all of these developments are long-term global demographic changes that are already affecting the markets in which many companies seek to grow.

When combined with post-COVID-19 inflation and high interest rates, M&A decision-makers have a lot to digest, whether they are strategics or sponsors. The first half of 2025 saw a significant slowdown as dealmakers took stock of all these factors. However, it seems that in the second half of 2025 dealmakers began to gain clarity on where they believe these trends will land in the medium and long term. As a result, in 2026, we anticipate an acceleration in both domestic and cross-border transactional activity as large companies begin to move even quicker to shift their operations to reflect this new economic cycle, giving sponsors the opportunity to acquire attractive assets as they adjust to the increased cost of capital.

Several disruptive megatrends are reshaping the landscape for cross-border M&A.

Expect more corporate carve-outs

The most obvious outcome will be a rise in corporate carve-outs. Anecdotally, we are already seeing this trend at play, but we expect to see a surge. That said, we would not be surprised to see more complex transaction structures than the traditional carve-out in which the strategic fully exits a business. As increased cost of capital puts pressure on private returns, we are seeing a growing number of transactions in which corporate sellers are expected to retain some participation in the business following a sale to a sponsor, be that through seller financing arrangements or material rollovers that strategics have customarily avoided.

State capital reshapes market dynamics

Another trend that may impact M&A activity in 2026 is the growing involvement of the United States and other Western governments in transactions aimed at strengthening national security. We are seeing an increased investment of state capital in private companies that support economic or industrial goals, such as securing access to or production of critical minerals or energy supplies.

For instance, the US and Australia recently signed a deal to extend financial support to several Australian companies with mining and processing projects that will shore up both countries’ access to critical minerals. Each country will invest at least $1 billion over the next six months as the US works to secure access to the minerals needed to power domestic manufacturing, national security, and other strategic industries.

This kind of investment is not a new or particularly partisan phenomenon – its roots can be traced back in the US to the lead in to World War II – but it has the potential for unpredictable impacts on where and how public and private nonstate capital gets deployed, both now and when governments seek to monetize these investments. As geopolitical undercurrents continue to push governments to encourage certain assets into national ownership, there may be opportunities for private funds to deploy capital into those deals.

Reconfiguring global supply chains

Although the seismic shifts in global trade policies that have come to a head in 2025 continue to occur, it seems dealmakers are beginning to understand what this new era of global trade will ultimately look like. We have started to see several deals motivated by a drive toward localized manufacturing. Many companies are working to shorten cross-border supply chains and bring manufacturing closer to end consumers, whether on a national level or within regional trade blocks. For instance, many energy companies are acquiring manufacturing assets in, or otherwise shifting production to, the Middle East to service regional customers (and doing the same in other parts of the world), regardless of where the business is headquartered.

Additionally, there is a desire among multinational companies to develop close relationships and bring local partners into overseas markets where they might historically have sought to grow organically. That is in part a recognition of a broader want among customers to work with local counterparties and it often results in joint venture transactions or tie-ups with equity partners that can bring local operational knowledge.

Conclusion

Even though there is much change to navigate, we do not anticipate any slowdown in deal activity in 2026. Rather, we expect the most forward-thinking companies to reposition themselves for the next economic cycle, resulting in more opportunities for both strategic acquirors and sponsors.

We look forward to a busy year of large-scale M&A action ahead, as some long-predicted fundamental shifts materialize and start to boost deal momentum.

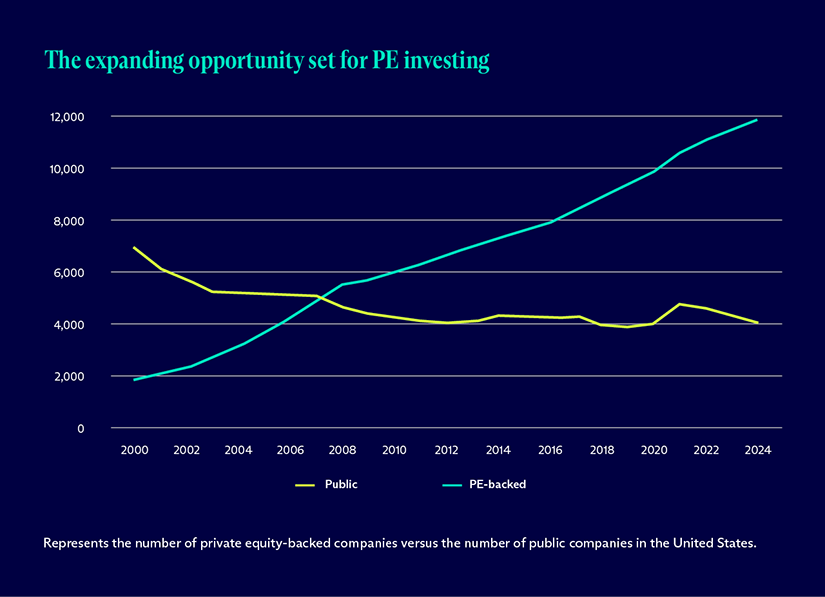

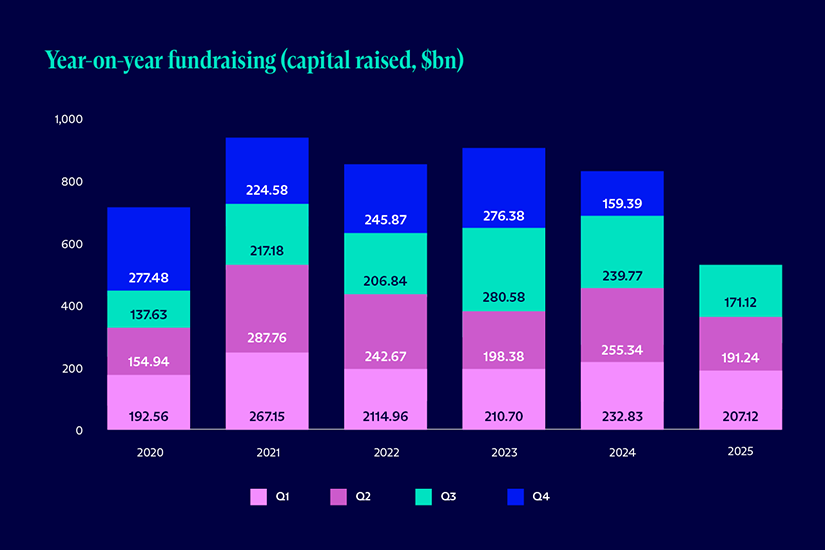

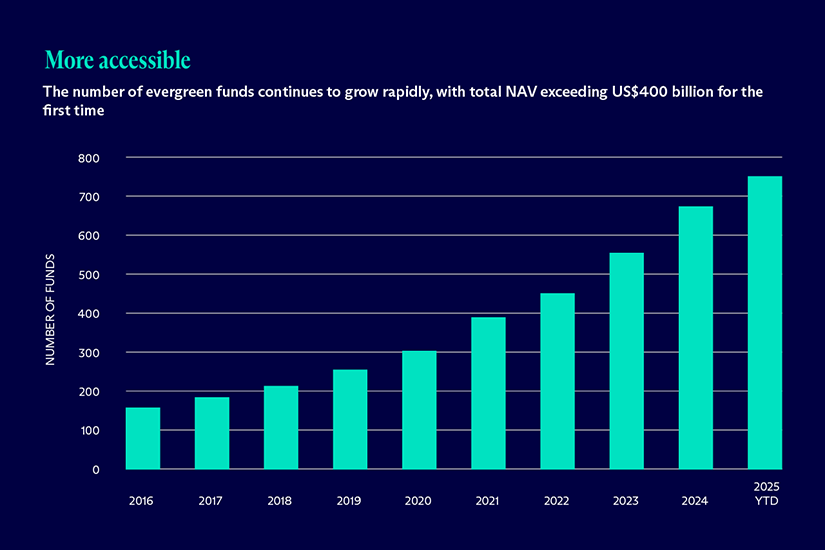

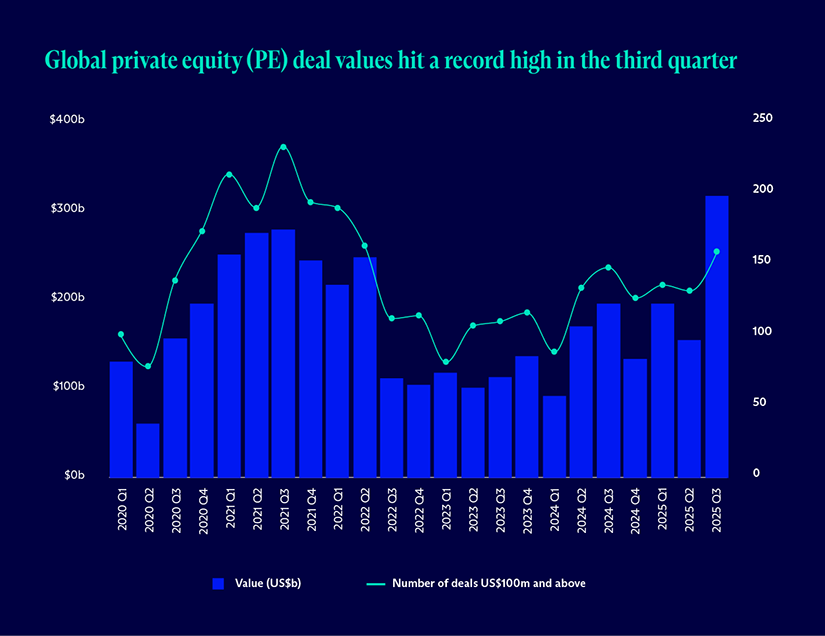

Market analysis: 10 trends affecting global private markets for 2026

ARTICLE

December 2025

Read time: 13 min

Welcome to the fifth edition of the Private Markets Update, a report in which our cross-border, multidisciplinary team of private capital advisers shares insights on the latest trends emerging across global private markets. This year, these insights are enhanced thanks to the merger of McDermott Will & Schulte.

Throughout this report, you will find detailed commentary on some of the major themes impacting private markets, including the emerging opportunities in professional sports, data centers, and litigation finance. We are pleased to share updates on developments in hedge funds, real estate, and transatlantic restructuring while also looking at the regulations shaping cross-border M&A going into 2026.

As with previous editions of this report, we explore some of the latest data on private markets activity via our 10 Trends to Track list. These trends are deemed most pertinent as we move into a new year because they are topics of conversation among our clients and are high on the agenda of sponsors, investors, and other market participants.

Entering a new year is an opportunity to reflect on the past 12 months, which have not been easy for private capital providers. If 2024 was characterized by general election uncertainty (as huge swathes of the global electorate went to the polls), then 2025 was about coming to terms with the results of those democratic processes. A new US administration in the White House brought a trade policy shift that impacted deal flow in the first half of 2025 while new governments in the United Kingdom and Germany brought shifting fiscal priorities and new approaches to infrastructure spending. For fund managers, there was much to digest.

There remain many uncertainties going into 2026 and plenty of headwinds to navigate, but as the policy backdrop has clarified, so too has the appetite to transact. In the coming year, we expect exit activity to pick up, fundraising to strengthen, and sponsor-driven M&A to accelerate, with private capital on hand to support businesses as they continue to address liquidity challenges and shore up for a new phase of growth.

The amount of capital deployed into private funds continues to grow year-on-year. The world’s largest asset manager recently noted in their Private Markets Outlook, that private markets currently account for $13 trillion in assets under management, with that figure predicted to grow to more than $20 trillion by the end of the decade.

The growth of private markets is being fueled on the demand and the supply side. From a demand perspective, more companies are staying private for longer, with the number of businesses listed on US stock exchanges diminishing over time. Likewise, companies are increasingly turning to private capital providers for the funds they need to navigate liquidity challenges and finance growth, recognizing the ability of private funds to respond with agile, bespoke solutions.

On the supply side, more capital is looking to benefit from the returns on offer in private markets. Allocations from private wealth, insurance, pensions, and sovereign investors are all expected to materially increase in the latter part of the decade, as those investors seek access to the real economy and see private markets as the best way to achieve that exposure.

Source: morgansstanley.com

![Side-by-side graph visualizations fo Americas PE deal activity in (#) by sector (left) and ($B) by sector (right) [source: Pulse of Private Equity Q3'25 KPMG analysis of global private equity activity as of 30 September 2025. Data provided by PitchBook.]](/wp-content/uploads/2025/12/McDermott_Private-Markets-Update-2026_Market-Analysis_Trend-8.png)

Unlocking global data center opportunities

ARTICLE

December 2025

Read time: 7 min

Key takeaways

- The accelerated rise of AI is driving demand for high-density data centers.

- These data centers require massive amounts of power, and the grid is ill-equipped to handle such power.

- In addition to traditional data center development opportunities, there is an investment opportunity around onsite electricity generation that requires significant capital for growth.

- This is an innovative space: new chips, cooling technologies, and designs; battery storage; collocated solar and wind power; and small modular nuclear reactors solutions are fast-emerging.

- New financing structures are being developed to fund powered land and powered shell opportunities or to refinance stabilized assets.

- There are geopolitical and regulatory issues to navigate in both the US and Europe.

The recent surge in generative artificial intelligence (AI) has resulted in an arms race to develop the technology, which will require many high-density data centers and significantly more electricity to power them. That challenge is creating a swathe of investment opportunities for private funds across debt, equity, energy, and infrastructure, right at the intersection of two global megatrends: digitization and decarbonization.

What is clear is that the global data center market is in serious need of power, further fueled by the growth of cryptocurrencies, and the traditional grid is not equipped to respond. Consequently, energy providers well-versed in data center developers’ needs are pursuing onsite electricity generation options, leading to interesting new structures in both the United States and Europe.

What is emerging is a market opportunity characterized by innovation, scale, and a deep need for capital. With traditional capital providers increasingly limiting their lending, private credit is seen as a growing source of finance at a time when deals are getting larger and the geopolitical and regulatory context is more challenging.

AI has created an arms race that will require many high-density data centers and significantly more electricity to power them.

Diversification of power essential

While electricity grids are under intense pressure, in all but extreme cases power is still available – just not necessarily where data centers are located. That means instead of bringing power to data centers, data centers need to be built near new power sources.

Developers must either improve data connectivity to and from those new sites or build onsite electricity generation as a complement – but rarely a total substitute – to the grid, an option known as behind-the-meter generation.

As the ability to deliver data center capacity quickly becomes crucial, data center owners and developers are increasingly offering their tenants – most often large US tech companies, or hyperscalers – solutions to bridge a temporary lack of capacity. Alternative power sources are installed to increase the site’s total capacity and provide backup power in case of grid deficiencies. While the market for renewable energy powered data centers continues to grow, this is progressively done via the installation of gas turbines which, once the onsite plant is built, then transition to a backup role.

At full production capacity, a data center powered by onsite generation has the added advantage of potentially selling surplus power back to the grid. This could help avoid a loss of production capacity and alleviate some of the financial pressure on the overall project.

Innovation’s impact

Ironically, AI will accelerate innovation and substantially affect how data centers are designed, powered, and connected to networks. A world where IT drives the economy represents an entirely new paradigm, one that will lead humanity into uncharted territory.

The current race for advanced chips and the pursuit of superintelligence – an intelligence that surpasses human capability – is a striking example of how the data center sector will evolve over the next decade.

Square footage is becoming less important as servers become more efficient. But these servers require significantly more power and cooling to function, and their numbers have increased dramatically. In response to that new challenge, small modular nuclear reactors are expected to be operational and deployed across data centers within two to four years. Similarly, solar and wind power generation is improving, and the use of hydrogen sources is being regularly tested.

Financing behind-the-meter data centers

We see a growing number of private funds exploring data center power opportunities. Powered land (or land with a timeline to power) in or near a cluster of existing data centers is seen as the golden ticket.

The market is also pursuing powered shells, on which data centers matching hyperscaler designs can be developed. These can either be rented with an option to purchase or purchased once built.

A similar logic is emerging for onsite power generation. Energy developers are buying large tracts of land, securing a connection to the grid, and building initial onsite generation plants. This first move is generally financed through equity and followed by a series of debt financing.

Once the initial groundwork is in place, developers seek equity partners to finance part of the construction of the data center through a joint venture. The remainder is financed through debt at the joint venture level, with lenders secured by a series of subordination, non-disturbance, and attornment agreements; enforcement rights; and, ultimately, the lease secured with the anchor tenant. Given that the overall power capacity may not be fully delivered at this stage, some projects rely on additional mezzanine financing.

The final step for the energy company that initiated the project is to secure additional funding to complete and build the onsite generation plant. This not only delivers a reliable primary power source for the existing buildings but may attract new customers who may request the construction of additional data center buildings powered by the plant.

The markets continue to evolve

The current global market capacity of data centers is approximately 59 gigawatts (GW), and Goldman Sachs estimates there will be around 122GW of data center capacity online by the end of 2030.

The US currently represents approximately 50% of globally installed data center capacity and looks set to account for the majority of data center power demand growth. This reflects the presence of many major hyperscalers, plus good access to reliable energy, strong connectivity, a low country risk profile, and a favorable regulatory environment.

The US Department of Energy recently directed the Federal Energy Regulatory Commission (FERC) to initiate a rulemaking process to expedite grid interconnection for data centers, aiming to ensure the grid can keep up with demand and processes are smoothed out. It remains to be seen how that proposal, which essentially expands FERC’s jurisdiction over the interconnection of large loads, will be met by state regulators.

Conclusion

The construction of high-density data centers and quickly increasing electricity demands present vast opportunities for private capital to support both data center and power project developers, and particularly those capable of bridging the two domains.

As deals continue to get larger and the pace of innovation intensifies, investors who can adeptly navigate these trends will be well positioned to capitalize on a meaningful growth trend.

Hybrid financing in life sciences: Unlocking growth amid market challenges

ARTICLE

December 18, 2025

Read time: 5 min

Life sciences companies and investors continue to navigate a complex and challenging investment landscape – marked by high interest rates, a volatile regulatory environment, tight venture capital (VC) markets, and slowly rebounding initial public offering (IPO) activity. Even so, the sector’s deep reliance on partnerships with major pharmaceutical companies and innovative MedTech providers is keeping deal activity alive, enabling strong performers to secure capital while driving life sciences advancements.

Against this backdrop, alternative financing strategies are no longer niche – in life sciences especially, they’re now essential. As costs continue to rise and pricing and reimbursement headwinds shift commercial assumptions, hybrid and crossover financing models – including royalty financing, innovative debt structures, and flexible capital stacks – are reshaping how capital is deployed across the life sciences sector and changing how deals get done.

Hybrid financing structures are helping catalyze sector growth and value creation, giving investors earlier, less crowded access to life sciences and MedTech operators. Blended finance approaches are helping companies secure better pricing and deal terms, de-risk investments, and position investors for significant upside when market favorability returns. And as life sciences mergers and acquisitions (M&A) accelerate and buyers look to acquire earlier in the development cycle, hybrid financing has become a critical bridge to acquisition – giving target companies the capital influx needed while providing investors structured protections and multiple paths to liquidity.

Creative financing and dealmaking options are also helping life sciences companies keep up with the rapid pace of scientific progress, while maintaining cash reserves to drive growth, development, and top-line success. At the same time, investors are structuring deals focused on creating value for all parties, whether that’s co-investing with VCs or partnering with strategics to reduce risk.

With these key trends in mind, what should life sciences investors and targets focus on for dealmaking success in 2026 and beyond? Six actionable steps include:

1. Spread financial risk and remain competitive

In a crowded market, creative life sciences dealmakers must move beyond binary “exit-or-bust” financing models to achieve success. Royalties, build-to-buy, or partial-liquidity structures help spread financial exposure while letting investors capture upside from pivotal inflection points like regulatory approvals and asset development milestones. These flexible structures give companies access to needed capital without forcing premature exits or excessive dilution.

2. Prioritize metrics and measurement

A comprehensive risk management strategy must include internal metrics and measurement to evaluate hybrid deal performance, such as milestone-to-capital spend ratios, actual vs. modeled probability-of-success curves, non-dilutive capital leverage, structured-return realization rates, and portfolio-level hybrid exposure concentration. Investors who make measurement a strong, repeatable capability will shape the next wave of investment wins and market norms.

3. Match funding models and capital needs to sector dynamics

Not every funding model works everywhere or at every point in time. In MedTech, hybrid financing options can shorten the path to commercialization, giving companies timely, flexible access to capital during the incredibly expensive clinical, regulatory, and scale-up phases. By reducing dilution and funding critical milestones without delays, companies and investors can accelerate launch preparation and reach commercialization faster. For specialty pharma, on the other hand, royalties may be a simpler investment approach, given fewer operational entanglements, clearer economics, and more predictable risk/return characteristics. Leveraging advisors with deep life sciences industry knowledge around the models that resonate in specific sectors can help investors move quickly and ensure alignment among stakeholders.

4. Build the right syndicate early

Deals succeed when investors line up and begin their due diligence before a capital raise is critical. Now more than ever, investors need to build strong relationships and explore proactive deal terms with potential partners well before a formal fundraising round begins, including providing strategic advice and expertise. This forward-looking, collaborative approach often leads to more favorable deal terms, better strategic alignment, and a smoother overall fundraising process for both parties, reducing the pressure and competition typical of later-stage, more crowded raises.

5. Treat hybrids as a core strategy, not a side bet

Hybrid structures allow for a combination of high-growth potential assets, which carry higher risk, with more de-risked or cash-flowing assets, thereby creating a more stable portfolio with longer-term viability. Embedding hybrid structures into the core investment playbook – not just using them opportunistically – creates more consistent returns across cycles and improves resilience when traditional equity markets are tightened.

6. Embrace the power of secondary markets

Secondary markets are opening new pathways for early investors to realize liquidity well before traditional exits. In the life sciences sector, secondary markets help investors and founders unlock capital even while clinical trials are ongoing or regulatory milestones are pending, reducing pressure to sell under suboptimal conditions, such as today’s unpredictable reimbursement and regulatory ecosystem. Secondary markets also help new investors acquire stakes in later-stage, more derisked companies, meaning investors can participate in the upside of targets with validated pipelines, established manufacturing capabilities, or early revenue streams, while mitigating the operational and clinical risks that often challenge earlier-stage ventures.

The life sciences sector is at an exciting inflection point, with headwinds and opportunities aplenty. But as we think about the actual assets that are coming online – those with high-ROI potential and thus ability for continued reinvestment into growing pipelines – hybrid financing options represent the kind of creative, strategic dealmaking that will drive scientific and technological advancements now and in the future.