ARTICLE

April 2026

Read time: 8 min

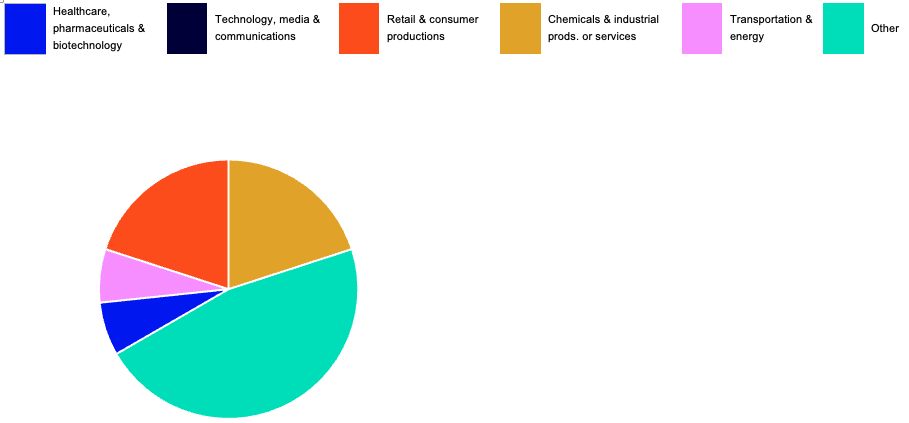

Global competition authorities scrutinized mergers closely in Q1 2026 across industrial, healthcare, energy, and services sectors. In the United States, the US Department of Justice (DOJ) and Federal Trade Commission (FTC) addressed deals in packaged ice, healthcare services, and medical technology, resulting in targeted divestitures and, in one case, deal abandonment following extended review. In the European Union, the European Commission applied the Foreign Subsidies Regulation (FSR) alongside merger control to impose remedies on a state-backed acquisition. In the United Kingdom, the Competition and Markets Authority (CMA) cleared a completed merger in the used vehicle auction sector after a Phase 2 investigation without imposing remedies.

These cases underscore a few clear themes: US agencies are pursuing targeted remedies, particularly in healthcare; close-competitor deals continue to face meaningful execution risk; the EU is ramping up scrutiny of foreign subsidies, including their impact on bidding; and the CMA remains willing to clear deals where competitive constraints are well supported, even in concentrated markets.

Notable US cases

DOJ requires divestiture of customer relationships to clear Reddy Ice’s acquisition of Arctic Glacier

Markets/structure

The merging parties, Reddy Ice and Arctic Glacier, are the first- and third-largest packaged ice producers in the United States. The DOJ alleged that the deal would combine the two largest packaged ice producers in local markets defined around two sets of targeted customers: (1) retail chains in Oregon, Washington, and Imperial and Riverside counties in California, and (2) airlines and airline caterers in the Boston and New York City metropolitan areas.

Summary and observations

On January 30, 2026, the DOJ entered into a settlement with Reddy Ice and Arctic Glacier, allowing the parties to proceed with their proposed deal with conditions.

The DOJ alleged the merger would eliminate head-to-head competition between Reddy Ice and Arctic Glacier in specific local markets, allowing the parties to raise price to targeted customers such as retail chains and to airlines and airline caterers.

For some markets, the parties agreed to divest ice manufacturing and distribution facilities and customer contracts. For others, the parties divested customer contracts without facilities. Each divestiture buyer is a co-packer for Reddy Ice that currently serves the divested customer.

FTC requires Sevita to spin off 168 facilities to clear acquisition of BrightSpring’s ResCare business

Markets/structure

Sevita and BrightSpring’s ResCare are the leading providers of home and community-based services for people with intellectual and developmental disabilities (IDD). The FTC alleged that the deal would substantially lessen competition for services to individuals with IDD in intermediate care facilities (ICFs) in local markets in Indiana, Louisiana, and Texas. In each of the local markets, the FTC alleged the companies had a combined share well over 30% and are each other’s largest competitor.

Summary and observations

The case is notable for alleging harm across non-price dimensions of competition. ICF services are, for the most part, paid through Medicaid according to fixed reimbursement rates, meaning parties compete on non-price factors. The FTC emphasizes that antitrust law “is not confined to price effects alone; it safeguards consumers – here, individuals with IDD – from a broader spectrum of harms.”

The FTC alleges that the deal would decrease quality and reduce or eliminate consumer choice. The parties compete on quality to attract referrals, convert referrals to residents, and retain residents. The elimination of competition between the parties would reduce incentives to maintain and improve the quality of facilities, staffing levels, safety, care, and service offerings. The deal would also reduce or deprive individuals with IDD choice when it comes to ICF providers.

To resolve the FTC’s competitive concerns, the parties agreed to divest 128 of Sevita’s facilities in Indiana, Louisiana, and Texas to Dungarvin Group.

Alcon and LENSAR terminate proposed deal after lengthy FTC review

Markets/structure

The FTC indicated that Alcon and LENSAR are “the two most significant players” in the femtosecond laser-assisted cataract surgery market.

Summary and observations

Alcon’s $365 million deal to acquire LENSAR was announced on March 25, 2025. Nearly a year later, on March 16, 2026, the parties agreed to terminate the proposed transaction, with Alcon attributing the decision to “the delay and associated costs of [the FTC’s] extended regulatory review.” The FTC appeared prepared to file suit to enjoin the deal. The merger agreement provided for a $10 million termination fee to LENSAR nine months after closing and an outside date of April 23, 2026.

The FTC found significant competition between the parties, which the FTC alleged resulted in lower prices and increased innovation in the femtosecond laser-assisted cataract surgery market. LENSAR’s annual reports indicated its innovative system allowed it to take substantial share. LENSAR’s compact system, unlike Alcon’s, allows for an entire laser-assisted cataract surgery to be performed in one room instead of two.

The FTC found a market comprised of laser-assisted cataract surgery systems, excluding traditional cataract surgery. Although the FTC did not address its reasons for doing so, it appears that commercial insurers use different reimbursement schemes for the two procedures and laser-assisted techniques offer unique benefits to patients over traditional surgery. The FTC’s investigation underscores that healthcare – innovation in healthcare, in particular – continues to be a focus at the FTC.

Notable EU case

European Commission imposes FSR remedies on ADNOC’s acquisition of Covestro

Markets/structure

The transaction involved the acquisition by ADNOC, the UAE state-owned energy and petrochemicals group, of Covestro, a leading German producer of high-performance polymers serving electronics, automotive, construction, and other industrial sectors. The relevant markets were global polymer and advanced materials, with Covestro maintaining a strong EU manufacturing and R&D presence.

Summary and observations

The acquisition of Covestro by ADNOC illustrates the emerging dual regulatory framework created by the EU Merger Regulation and the FSR. Under EU merger control, ADNOC obtained clearance from the Commission to acquire sole control of Covestro, while the Commission used the FSR to assess financial contributions from the United Arab Emirates. The Commission determined that ADNOC had benefited from a UAE state guarantee and a committed capital increase, which could distort market conditions within the EU.

For the FSR analysis, the Commission identified two main theories of harm: distortion of the acquisition process, enabling ADNOC to submit a higher bid, and potential post-transaction distortions through a strengthened investment position. Notably, this was the first case in which the Commission established that a distortion occurred during the transaction process itself, finding that foreign subsidies enabled ADNOC to offer an overvalued price and accept risks that a non-subsidized investor would not, potentially deterring other bidders. The Commission ultimately granted conditional clearance under the FSR in November 2025, requiring ADNOC to remove the effects of the state guarantee and to provide EU competitors with access to key Covestro sustainability-related patents for 10 years.

Notable UK case

CMA clears Constellation’s acquisition of Aston Barclay

Markets/structure

The transaction concerned Constellation Developments’ completed acquisition of ABVR Holdings (trading as Aston Barclay), both active in the business to business (B2B) used vehicle auction services market in Great Britain. Constellation is the largest operator in the sector through British Car Auctions (BCA), while ABVR is a significant independent competitor with multiple auction centers.

The CMA’s market investigation identified a relatively concentrated competitive landscape, with BCA as the leading national player and Aston Barclay positioned as the third-largest operator.

Summary and observations

The CMA opened a Phase 2 investigation on October 13, 2025, after concluding that the completed acquisition constituted a relevant merger situation requiring an in-depth investigation. In its interim report published on January 22, 2026, the inquiry group provisionally cleared the merger, finding no substantial lessening of competition in the supply of B2B used vehicle auction services across Great Britain. The CMA concluded that, despite the combination of two sizeable players, evidence did not show a materially adverse impact on competitive dynamics, vendor choice, or buyer outcomes. Following consultation and review of stakeholder submissions, the CMA issued its final report on March 5, 2026, formally clearing the merger without remedies and confirming that the acquisition is not expected to harm competition.

Overall, the CMA’s final findings underscore that existing competitive pressures, alternative auction channels, and customer switching options were sufficient to prevent the merged entity from exercising market power, despite notable concerns raised by rival auction groups and certain commercial vendors during the review.

EU and UK merger control in transition: Innovation, sustainability, and cross-border coordination

ARTICLE

April 2026

Read time: 6 min

The European Union (EU) is recalibrating its merger-control regime to respond to structural economic shifts driven by digitalization, decarbonization, and intensifying global competition. Policymakers are increasingly seeking to balance traditional competition principles with broader industrial, sustainability, and strategic autonomy objectives. Several initiatives illustrate this transition: First, the Commission is preparing updated merger guidelines that place greater emphasis on innovation, dynamic market analysis, and efficiency considerations aimed at strengthening European competitiveness. At the same time, proposed legislation, such as the Industrial Accelerator Act, introduces an additional review mechanism for foreign investments in strategic sectors, signaling a stronger industrial policy dimension. Finally, merger assessments are progressively incorporating public interest considerations, particularly environmental and social sustainability.

The United Kingdom (UK) is reshaping its merger-control framework as part of a broader strategy to strengthen economic competitiveness and improve regulatory predictability. Guided by the government’s 2025 “strategic steer,” reforms aim to modernize the institutional structure and operational approach of the Competition and Markets Authority (CMA) while ensuring that enforcement remains proportionate and business friendly. Key proposals include changes to decision-making structures, new operational priorities designed to accelerate reviews, and clearer jurisdictional rules to reduce uncertainty for merging parties. The new EU-UK Competition Cooperation Agreement introduces a formal information-sharing framework that enhances coordination between the CMA and European competition authorities.

EUROPEAN UNION

Modernizing EU merger control: Updates to the European Commission’s merger guidelines

- The Commission is committed to modernizing the EU merger guidelines to address the transformational challenges of digitalization, globalization, and decarbonization. A formal draft is expected by spring 2026, including the following key substantive shifts:

- Innovation shield: A protective framework for startups and innovators, focusing on long-term competitive dynamics rather than short-term price effects.

- Broadened policy criteria: Formal integration of sustainability, labor markets, and national security, alongside supply chain resilience in strategic sectors such as aerospace.

- Efficiency flexibility: A proposed lowering of the evidentiary bar for efficiency claims, allowing mergers that significantly enhance regional industrial competitiveness.

- Dynamic analysis: Extending assessment timeframes beyond the typical three-year window to capture delayed benefits in disruptive technology sectors.

- Legal presumptions: Introducing rebuttable presumptions to distinguish harmful transactions from those creating necessary scale for “European Champions.”

Expanding the toolkit: The potential introduction of the IAA

- The new Industrial Accelerator Act (IAA), proposed on March 4, 2026, and aiming to strengthen EU industrial capacity, reduce strategic dependencies, and accelerate clean and low-carbon technologies, introduces a parallel review process for mergers and acquisitions involving foreign investors in strategic sectors. This system operates alongside existing EU competition law, including the EU Merger Regulation, without replacing it. Key developments include:

- Mandatory and suspensory regime: Transactions exceeding EUR 100 million in sectors such as batteries or critical raw materials require prior notification to designated national investment authorities.

- Lowered control thresholds: Notification is triggered at 30% ownership or voting rights, widening the concept of control beyond the traditional “decisive influence.”

- Value-added substantive test: Approval depends on meeting specific criteria, such as establishing joint ventures or ensuring at least 50% of the workforce is located within the EU.

- Strict enforcement: Implementing transactions before approval (gun-jumping) faces administrative fines of at least 5% of the investor’s average daily turnover (5% of what the company earns on average for a single day based on annual revenue). This indicates a major shift toward strategic autonomy.

Bringing in public interest grounds

- EU merger control is undergoing a polycentric shift, moving beyond traditional price-centric analysis to integrate environmental and social sustainability. The Commission increasingly treats sustainability as a core differentiator in market definition and competitive assessments. However, this creates a potential “green catch-22”: identifying narrower, more sustainable markets increases the likelihood of the Commission challenging mergers between innovative “green” firms.

- To mitigate this, policy developments emphasize a holistic rethink of the efficiency defense. This includes explicitly considering out-of-market benefits and extending assessment timeframes to capture long-term environmental gains currently excluded by the traditional three-to-five-year window. Furthermore, there is a growing trend toward using investment-centric remedies to legally guarantee that claimed sustainability efficiencies actually materialize. These changes aim to align merger enforcement with broader EU objectives such as the European Green Deal and strategic resilience.

UNITED KINGDOM

Reforming UK merger control: The CMA’s revised approach to merger assessment

- UK merger control is currently undergoing a significant transformation driven by the government’s 2025 “strategic steer” to enhance international competitiveness and long-term economic growth.

- Restructuring decision-making: A major legislative proposal involves abolishing independent Phase 2 panels and replacing them with CMA board committees to improve democratic accountability. However, some experts caution that this structural shift could consolidate executive authority and risk future political influence in individual merger assessments.

- The “4Ps” operational strategy: The CMA is embedding pace, predictability, proportionality, and process across all operations to attract investment and foster business confidence. This involves deprioritizing multijurisdictional deals without specific UK impact and establishing ambitious targets for completing straightforward Phase 1 investigations.

- Narrowing jurisdictional scope: Reforms aim to limit CMA discretion by establishing specific criteria for jurisdictional tests like “share of supply.”

- Remedy evolution: Enforcement trends indicate greater flexibility for behavioral commitments and extended statutory timeframes for finalizing Phase 1 remedies.

Strengthening cross-border enforcement: The EU’s information-sharing framework with the CMA

- The EU-UK Competition Cooperation Agreement, signed on February 25, 2026, represents a major shift toward structured cross-border competition enforcement. As a supplement to the Trade and Cooperation Agreement, it replaces informal dialogue with a formal legal framework intended to improve predictability and legal certainty. A central innovation is the introduction of a new information-sharing mechanism allowing the UK CMA and European authorities to exchange confidential data. Where domestic law permits, information may be shared without the provider’s consent.

- The agreement also promotes cooperation between the CMA and national competition authorities across EU Member States through mutual notification and coordinated investigations, reducing the likelihood of conflicting rulings. Parallel domestic reforms reinforce this goal by extending the CMA’s Phase 1 merger remedy period to 20 working days and clarifying jurisdictional tests through closed statutory lists.

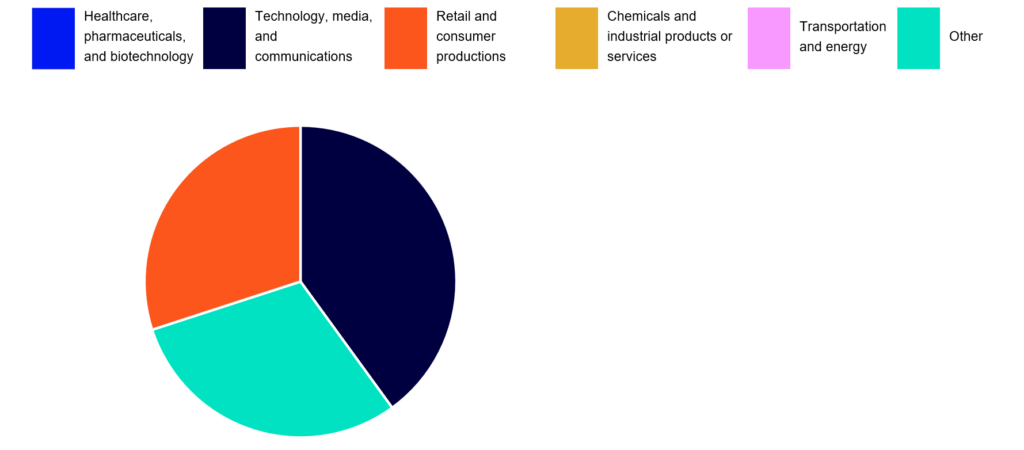

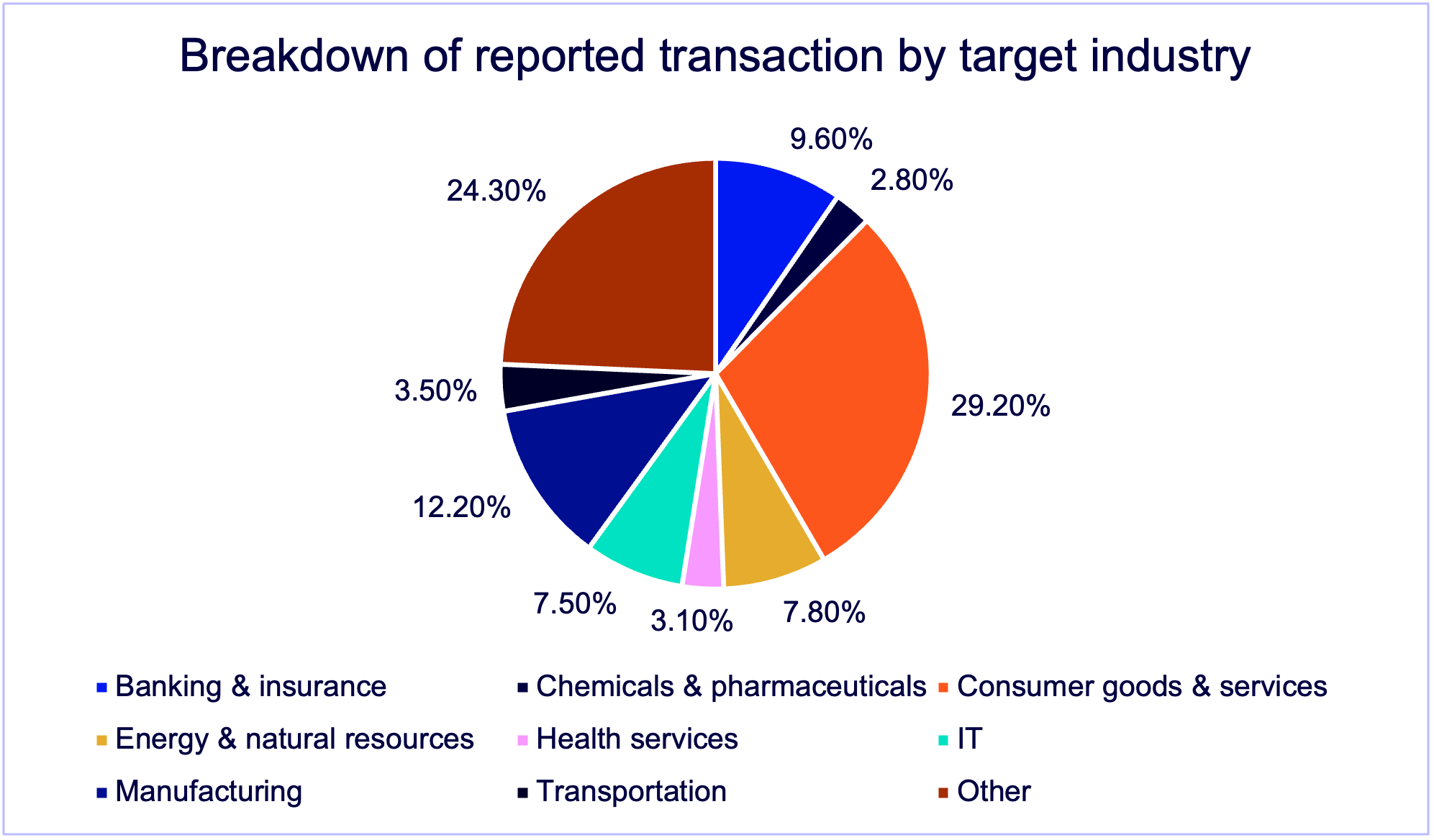

EU and UK Q1 2026 M&A activity: By the numbers

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

Time from signing to clearance

![]()

Merger enforcement under Trump 2.0: Challenges, crystallization, and criticism

REPORT

April 2026

Read time: 5 min

The Trump 2.0 antitrust agencies have changed how merger cases are being challenged and resolved. But the agencies’ tactics are not without criticism. States and lawmakers are scrutinizing recent Department of Justice (DOJ) decisions in several high-profile matters in which there are allegations of potential political interference, and conflicting views within the DOJ itself have resulted in the departures of several high-level officials. States and private parties are stepping in to fill perceived federal enforcement gaps. Meanwhile, a Fifth Circuit ruling has forced the regulators to revert to accepting the legacy Hart-Scott-Rodino (HSR) form while the Federal Trade Commission (FTC) appeals the decision.

FTC accepts old HSR form as Fifth Circuit hears challenge to new form

- Under the Biden administration, the FTC issued a final rule that adopted a new premerger notification form under the HSR Act. The 2025 HSR form expanded the categories of information that filers must furnish with their premerger notification, increasing the time and expense involved in preparing the filing.

- However, a legal challenge pending in the Fifth Circuit will decide the new HSR form’s fate. On February 12, 2026, a federal district court in Texas vacated and set aside the new HSR form as unlawful under the Administrative Procedure Act. The FTC appealed the decision to the Fifth Circuit, which on March 19, 2026, rejected the FTC’s bid to pause the lower court’s ruling pending the appeal. For now, federal regulators must accept the legacy, less burdensome form.

- Affirming their stance that the old HSR form is “insufficient to review modern mergers and acquisitions,” the FTC and DOJ are soliciting public comment on the effectiveness of the 2025 HSR form, suggesting that another round of HSR rulemaking might be on the horizon. The agencies’ requests signal an interest in using rulemaking to address “novel” transactions like “acquihires” that “may be structured to avoid” HSR reporting, as well as challenges posed by “late-proposed remedies” and “litigate the fix” strategies.

Trump 2.0 tactics for merger enforcement are taking shape

- FTC Chairman Ferguson emphasized that the FTC is open to negotiating settlements, which is a departure from policy under the Biden administration. The DOJ and FTC recently approved several transactions with settlements, including Sevita/BrightSpring, Columbus McKinnon/Kito Crosby, and Reddy Ice/Arctice Glacier. Ferguson expressed a distaste for “fake settlements ” that require extensive monitoring and noted a preference for “real settlements that fully protect competition” (which include divestitures of complete “lines of businesses,” with strong, upfront buyers). He also noted that behavioral remedies are disfavored and should be informed by the unique risks presented in different industries. Citing research suggesting that divestitures are “difficult” in retail and grocery contexts, Ferguson indicated that he will “require more” from parties in these sectors to show that their divestiture proposal preserves competition.

- For future FTC merger challenges, the FTC will attempt to litigate under the same standards as the DOJ. FTC Chairman Ferguson stated that his preference is to have the FTC challenge mergers by seeking a permanent injunction in federal court instead of the traditional FTC practice of seeking a preliminary injunction in federal court and then litigating on the merits in the FTC’s in-house administrative process. The FTC implemented this approach in its ongoing Loctite/Liquid Nails merger challenge.

- If Ferguson’s plan is put into practice, (1) the FTC will now have to meet the higher permanent injunction standard, (2) merging parties can expect lengthier timelines to trial on the merits, and (3) the commissioners can now engage in settlement negotiations during litigation because they are not in an adjudicative role.

States stepping up as DOJ shrinks and settles

- Twelve states and the District of Columbia continue to challenge a DOJ settlement approving Hewlett Packard Enterprise’s acquisition of Juniper Networks. The states’ intervention was prompted by reports from an ousted, formerly senior DOJ official that the settlement was a product of improper influence by lobbyists.

- Allegations of political interference have emerged again this quarter, related to the DOJ’s decision to clear, without a second request, the $1.6 billion merger of Compass and Anywhere, two of the largest real estate brokerages in the United States. The Wall Street Journal reported that Compass appealed to DOJ officials above Gail Slater, the former assistant attorney general of the Antitrust Division, who wanted to investigate the deal in-depth. Lawmakers have also raised concerns about Slater’s forced resignation in February 2026, given allegations that DOJ leadership overrode Antitrust Division officials in matters like HPE/Juniper and Compass/Anywhere.

- Parties should be aware that allegations of political influence may prompt intervention by state enforcers and private parties. For example, after Nexstar Media Group, Inc.’s, $6.2 billion acquisition of TEGNA Inc. received Federal Communications Commission (FCC) and DOJ approval – with a public endorsement from President Trump – a coalition of eight states filed a lawsuit to block the deal. Separately, DirecTV succeeded in obtaining an order to temporarily pause further integration efforts between the parties.

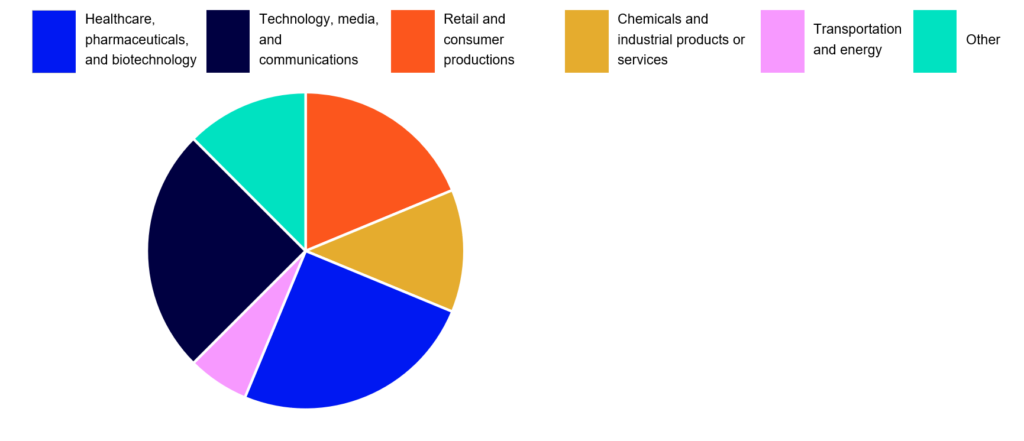

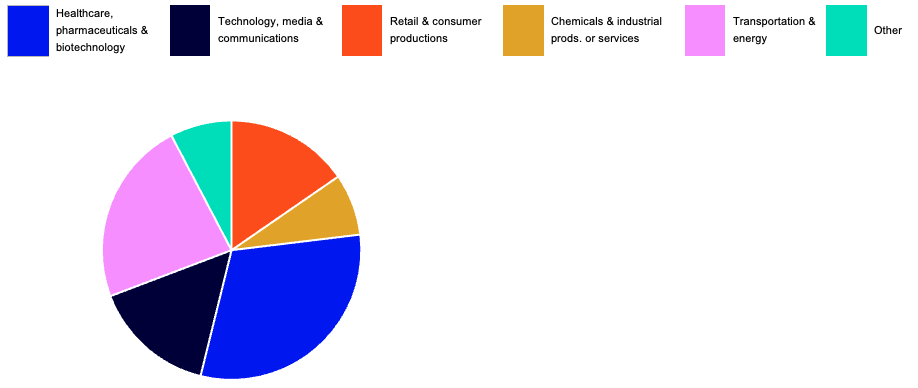

US Q1 2026 M&A activity: By the numbers

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

Time from signing to consent or investigation closing

![]()

Global M&A trends: 3 notable Q4 2025 cases out of the US and UK

ARTICLE

February 2026

Read time: 6 min

Merger control authorities remained active in Q4 2025, reviewing transactions across the healthcare, manufacturing, and consumer goods sectors. In the United States, courts and regulators issued rulings in cases involving medical device coatings and automotive services. In the United Kingdom, the Competition and Markets Authority accepted remedies to resolve concerns in a food manufacturing merger.

These decisions illustrate key enforcement themes: courts’ willingness to accept party-proposed remedies despite regulator skepticism, the viability of new market entrants as divestiture buyers, and regulatory theories focused on market concentration and elimination of competition even absent concrete evidence of consumer harm. Below are three notable cases that capture these trends.

Notable US cases

FTC fails in challenge of GTCR BC Holdings, LLC acquisition of Surmodics, Inc.

Markets/structure

The FTC alleged the deal would eliminate head-to-head competition between the two leading providers of outsourced hydrophilic coatings in the United States, Surmodics and Biocoat Inc. (owned by GTCR).

Summary and observations

In November, Judge Cummings of the US District Court for the Northern District of Illinois denied the FTC’s attempt to block GTCR’s $627 million acquisition of Surmodics, the other leading provider of outsourced hydrophilic coatings for medical devices.

The FTC argued that the merger would eliminate head-to-head competition between Surmodics and Biocoat (acquired by GTCR in 2022) for outsourced hydrophilic coatings, which are a critical component in lifesaving medical devices such as catheters. The FTC alleged that the post-merger entity, absent any divestiture, would control more than 50% of the market.

Judge Cummings’ ruling demonstrates the success of parties litigating the fix. At trial, Judge Cummings repeatedly urged the parties to reach a settlement, but the FTC expressed little interest in any sort of remedy, even calling it a “smokescreen.” The merging parties, on the other hand (and in an attempt to litigate the fix), proposed a divestiture agreement whereby GTCR would sell portions of Biocoat that overlapped with Surmodics’ offerings to a third party, Integer. The FTC argued that the divestiture to Integer was not sufficient to remedy any harm because they were a new entrant in the space, but the court held that Integer was well qualified to compete. The court also relied heavily on the merging parties’ expert testimony which calculated far lower shares than the FTC asserted; ultimately, the court was persuaded that the remedy would suffice to mitigate any potential anticompetitive effects from the deal.

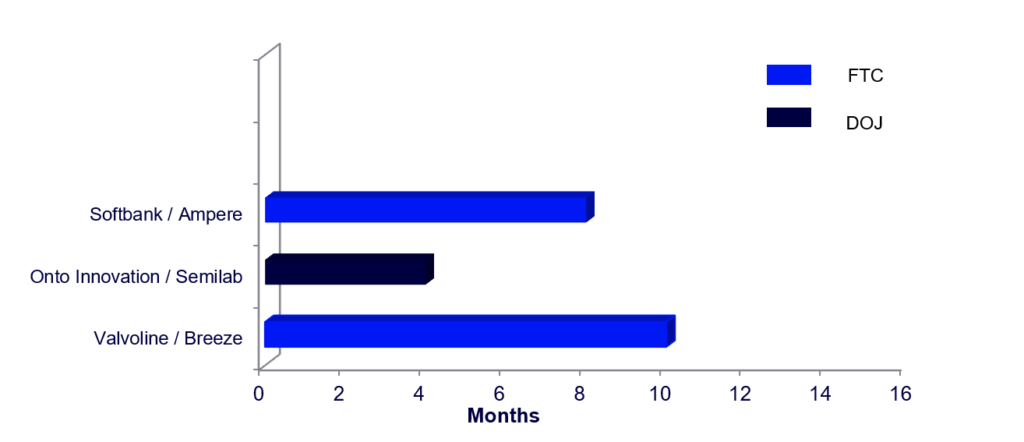

FTC agrees to consent order in Valvoline Inc. acquisition of Breeze Autocare

Markets/structure

The FTC alleged the deal would eliminate head-to-head competition between two quick-lube oil change companies, Valvoline and Breeze Autocare, in 25 local markets across eight states, creating combined shares in excess of 30% or more.

Summary and observations

In November, the FTC agreed to a divestiture order as a condition to closing Valvoline’s $625 million acquisition of Breeze Autocare (owned by Greenbriar Equity). As part of the agreement, the parties agreed to divest 45 quick-lube oil change retail stores, of the 200 retail stores to be acquired, to Main Street Auto. Main Street Auto is a new entrant in the 25 local markets that were the focus of the FTC.

The FTC alleged that the proposed acquisition would result in unilateral effects by eliminating head-to-head competition between the parties. However, in challenging the deal, the FTC’s complaint lacked more typical allegations in a unilateral effects case that Valvoline and Breeze Autocare are particularly close competitors or that customers lacked strong substitutes for oil-change suppliers in the local markets of concern. Instead of focusing on the potential for the new combined entity to raise prices absent competition from one another, the FTC’s theory resembled that of a coordinated effects case. Indeed, the emphasis in the complaint was that Valvoline’s post-merger market shares would be more than 50% in 17 of the 25 local markets alleged.

While this administration has shown a greater appetite for consent agreements, the antitrust theories propagated still echo a dangerous pattern: that elimination of head-to-head competition alone is bad, even when not tethered to any concrete allegations of harm.

Notable UK case

CMA grants conditional clearance in Greencore acquisition of Bakkavor

Markets/structure

Market for supply of own-label chilled sauces; effectively a four-to-three merger with two substantially smaller competitors and fringe players.

Summary and observations

The CMA reviewed Greencore Group plc’s acquisition of Bakkavor Group plc and found that the merger could lead to a substantial lessening of competition in the supply of own-label chilled sauces in the UK. The CMA considered Greencore and Bakkavor as close competitors based on tender offer data and that each served as an important constraint on the other. Post-merger, the CMA believed, the combined firm would have a substantially stronger position relative to remaining rivals such as 2 Sisters Food Group and Billington Foods, which the CMA viewed as weaker competitors. This raised concerns about reduced retailer choice and higher prices for supermarkets that would likely be passed through to consumers.

To address this concern and avoid a Phase 2 investigation, Greencore offered undertakings, including the divestment of its entire chilled soups and sauces business located in Bristol, together with associated assets and employees. Greencore also entered into a conditional agreement to sell this business to The Compleat Food Group, which the CMA assessed as a suitable purchaser.

Following a public consultation, in which grocery retailers raised no objections and several supported Compleat as an appropriate buyer, the CMA concluded that the undertakings were clearcut and effective in remedying the competition concerns.

A window into the latest EU and UK antitrust M&A activity: Clearance trends and CMA remedies

ARTICLE

February 2026

Read time: 6 min

The fourth quarter of 2025 underscored evolving merger control frameworks in the European Union and United Kingdom, marked by greater flexibility, streamlined processes, and pragmatic enforcement. Competition authorities are showing increased openness to behavioral remedies, encouraging deeper pre‑notification engagement, and prioritizing proportionate solutions that preserve pro‑competitive transactions. These developments highlight a regulatory environment in which strategic planning, early dialogue with authorities, and well‑crafted remedies are essential to securing timely approvals in both jurisdictions.

European Union

Early and close engagement with the Commission results in clearances

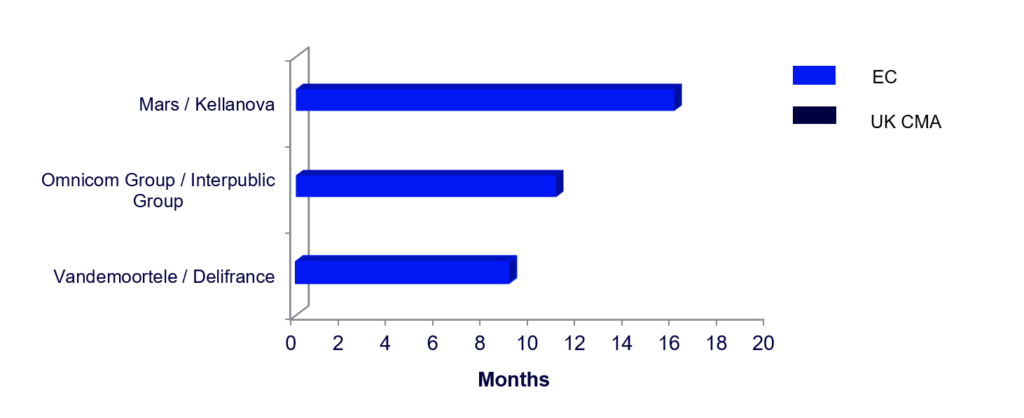

In the last quarter, the European Commission reviewed several complex transactions requiring significant regulatory scrutiny: (i) Mars’ acquisition of Kellanova, in which the Commission considered in-depth supplier power vis-à-vis supermarkets; and (ii) Omnicom’s acquisition of IPG, which was formally notified to the Commission in October 2024 and cleared in Phase 1, some 10 months after the deal was first announced.

In each case, the Commission eventually cleared the transaction, but only after requesting, reviewing, and considering thousands, if not hundreds of thousands, of documents submitted by the parties.

Unconditional clearance for Mars’ acquisition of Kellanova

One of the quarter’s most notable decisions saw the Commission unconditionally clear Mars’ acquisition of Kellanova in Phase 2 almost 16 months after deal announcement. The review focused on how the deal might affect bargaining dynamics with retailers for snack and cereal products. The Commission ultimately concluded that there was no credible risk of increased power leading to competitive harm, relying on the differentiated nature of the relevant product categories and the lack of evidence supporting increased brand loyalty or a “basket effect” on the part of consumers.

The investigation into portfolio effects highlights that the Commission will closely scrutinize transactions in markets where broad product portfolios play a large role and where products could be perceived as “must-stock.” Nevertheless, the unconditional clearance demonstrates that the Commission is unlikely to challenge under a portfolio effects theory without persuasive economic evidence and robust data.

Unconditional clearance for Omnicom’s acquisition of IPG

The Commission also unconditionally approved Omnicom’s acquisition of Interpublic Group (IPG), a merger that creates one of the world’s largest advertising and marketing services networks. The assessment found that existing competitive constraints – from players such as WPP, Publicis, and others – along with high customer mobility and relatively low switching costs, meant the deal was unlikely to significantly impede effective competition in the European Economic Area.

The parties did not formally file the transaction with the Commission until 10 months after deal announcement, after having obtained approval from multiple other jurisdictions. This transaction demonstrates that for complicated transactions parties need to spend a significant amount of time in pre-notification discussions with the Commission.

United Kingdom

CMA revises approach to remedies in year of streamlining merger control investigations

On December 19, 2025, the new guidelines for merger remedies, issued by the Competition and Markets Authority (CMA), took effect. The changes to the merger remedy guidelines are the latest installment in the CMA’s implementation of the “4Ps” framework – pace, predictability, proportionality, and process – which seeks to make merger control more transparent and business friendly. Key points include the following:

Behavioral remedies are more acceptable

While structural remedies remain the preferred option and the test remains the same (i.e., will the remedy be effective, and if so is the remedy proportionate?), the guidelines suggest a more open approach to behavioral remedies, especially if the CMA’s concern relates to specific activities and there is no other alternative remedy to “fix” an otherwise pro-competitive transaction.

Similarly, the CMA relaxed its position on accepting behavioral remedies during the first phase of the investigation. Behavioral remedies still must meet the “clear cut” standard, which requires that remedies must provide obvious and straightforward resolutions to competition concerns and be capable of ready implementation. However, the CMA highlights that early engagement on a remedy that aligns with established market practices and has a degree of market transparency, as well as the parties’ appointing a monitoring trustee, are all factors that increase the likelihood of the CMA accepting behavioral remedies early in the investigation.

Willingness to discuss remedies earlier in the review process

The CMA’s updated guidelines open the door for early, pre-notification discussions around remedies, with such discussions being “without prejudice” to the substantive analysis. Particularly with more-complex remedy packages that include carve-outs (as opposed to standalone businesses), the CMA seeks early engagement from the parties to provide measures to mitigate concerns such as the inclusion of an upfront buyer, the use of a monitoring trustee or independent expert to assess compliance, as well as potential alternative solutions should the remedy deal fall through.

The new guidelines bring to a close a year of realignment for the CMA and make the UK a much more deal-friendly environment.

After introducing new service standards that streamline the merger control process (reducing the average timeline from five to three-and-a-half months) and updating guidelines on jurisdiction and process, the CMA rounded out the year by publishing its latest annual merger investigation outcomes.

For calendar year 2025, the CMA considered 881 mergers (compared to 1,037 mergers in 2024), investigating 39 at phase 1 (compared to 38 in 2024), with only 4 referred to in-depth phase 2 review (compared to 6 in 2024). Of those phase 2 investigations, two were unconditionally cleared (compared to 2 in 2024), 1 resulted in acceptable remedies (compared to 2 in 2024), one was blocked (same as in 2024), and none was abandoned by the parties (compared to one in 2024). Overall, only 0.1% of all considered mergers were blocked or abandoned in 2025 (same as in in 2024).

EU and UK Q4 2025 M&A activity: By the numbers

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

Time from signing to clearance

5 lessons learned from US litigation wins/losses in 2025

ARTICLE

February 2026

Read time: 6 min

2025 proved to be a challenging year in court for the Federal Trade Commission (FTC), as it was unsuccessful in challenging the Tempur Sealy/Mattress Firm acquisition, the GTCR/Surmodics acquisition, a decade-old Meta Platforms acquisition, and (on appeal) the Microsoft/Activision Blizzard acquisition. These decisions provide several key takeaways for companies contemplating future M&A.

Overly aggressive, narrow product markets hurt the agencies’ claims

Courts have rejected relevant markets proposed by the FTC where the narrow segmentation is belied by the record and industry norms. In Tempur Sealy, the FTC alleged a “premium” market for mattresses over $2,000. The district court disagreed, finding competition for mattresses “fierce” and noting that the FTC’s own expert admitted that he picked $2,000 as a threshold merely because it gave Mattress Firm higher shares. In the retroactive challenge to Meta, the FTC’s proposed market included Facebook, Instagram, Snapchat, and MeWe but excluded YouTube and TikTok (which are not owned by Meta). The district court disagreed, finding that YouTube and TikTok were competitive substitutes to Facebook and Instagram. Ultimately, market definition is very fact dependent, and the agencies have won many cases by proving narrow markets where facts supported them, especially when business documents align with the narrow-alleged market. The FTC announced on January 20, 2026, that it will appeal the district court’s decision in Meta, and it remains unclear whether retroactive challenges — brought after market conditions have significantly changed since the original acquisition — will gain traction on appeal.

Courts are inclined to accept remedies as a fix to merger challenges

In Tempur Sealy and GTCR, the courts found that the merging parties’ proposed remedies mitigated any antitrust concerns. In GTCR, to address the horizontal overlap, the merging parties proposed a fix during the course of litigation to sell portions of GTCR’s Biocoat to Integer. In Tempur Sealy, to address vertical concerns, the judge found that behavioral remedies (e.g., slot commitments and supply agreements) and a small divestiture of stores undermined the FTC’s concerns. Similarly, in Microsoft, the court found that Microsoft’s licensing agreements and pledge to keep Activision’s key games on all platforms addressed the vertical foreclosure issues. Even when the regulators are unwilling to accept the proposed remedy, these cases demonstrate that courts are giving significant weight to remedies, enabling the parties to “litigate the fix” and prevail at trial.

Vertical challenges are hard to win

The courts have rejected vertical foreclosure theories of harm that rely solely on market share or a “big is bad” approach. In both the Microsoft/Activision Blizzard acquisition and the Tempur Sealy acquisition, the FTC failed to provide concrete evidence of likely foreclosure of competitors, post-acquisition. In Microsoft, the court found that Microsoft lacked profit incentives to only make games available on Microsoft’s gaming system, Xbox. In Tempur Sealy, in addition to the behavioral remedies offered, the court found the potential foreclosure harm for competitors was overstated, as Mattress Firm was not a critical sales channel for mattress manufacturers. While Mattress Firm was a large retail outlet, there were many other channels through which mattress suppliers could reach customers.

The FTC is moving away from in-house challenges

In its most recent transaction challenge, the FTC signalled a significant change in its enforcement practices, opting only to challenge the Henkel and A-Paint merger in federal court via a permanent injunction, rather than initiating an administrative action in parallel. Historically, the FTC has utilized Section 13(b) of the FTC Act, which allows the agency to seek a preliminary injunction in federal court where an administrative challenge is pending at the FTC. Under Section 13(b), a court can grant a preliminary injunction enjoining the merger until the case is heard in the administrative action if the FTC raises questions on the merits of the deal that are “serious, substantial, difficult and doubtful.” A permanent injunction, on the other hand, requires the FTC to succeed on the merits in proving that the merger may substantially lessen competition or tend to create a monopoly. While this change in practice means parties will only have to litigate one case at a time, the timeline for that challenge is likely to increase because of the additional legal and evidentiary standards that must be evaluated by the court. This change also aligns FTC antitrust enforcement more closely to that of the US Department of Justice (DOJ), which only utilizes a permanent injunction standard when challenging a merger.

Increased lobbying efforts in M&A prompts more state intervention

Twelve states and the District of Columbia have intervened in the latest settlement between the DOJ and merging parties, Hewlett Packard Enterprise (HPE) and Juniper Networks (Juniper). The HPE/Juniper settlement raised concerns after internal DOJ disagreements surrounding the deal became public, with former US Deputy Attorney General Roger Alford even calling the consent agreement “pay-to-play.” The intervening states have decried the settlement as the product of undue influence by well-connected lobbyists.

The publicity surrounding the settlement agreement has also called renewed attention to the Antitrust Procedures and Penalties Act (Tunney Act). Under the act, the DOJ must file proposed settlements in federal court for review, and the court evaluates the settlement agreement to see if it is in the public interest.

The states’ intervention in the HPE/Juniper settlement shows a pattern of increased state antitrust action amidst perceived politicized federal antitrust enforcement. Companies that are considering M&A activity should be cognizant that their lobbying efforts are likely to be monitored more closely, not just by the courts, but by state actors as well.

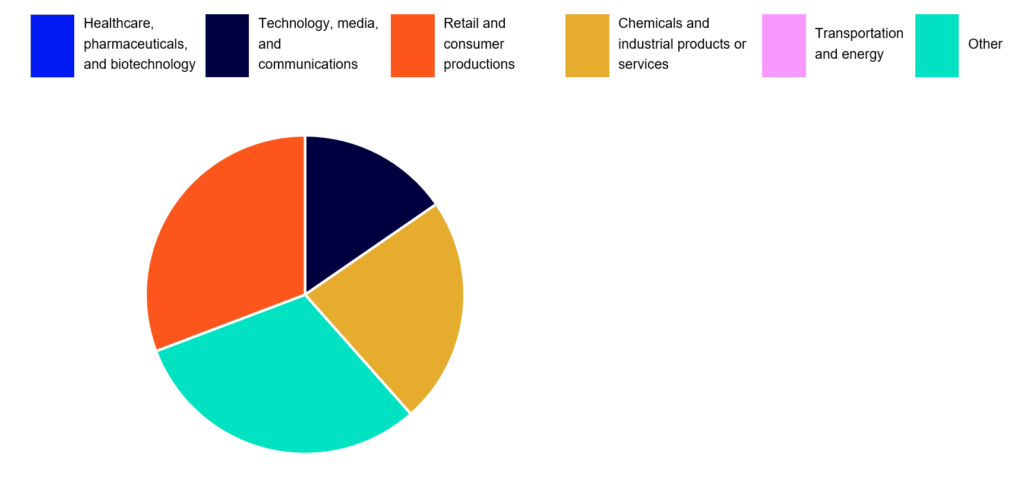

US Q4 2025 M&A activity: By the numbers

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

Time from signing to consent or investigation closing

Global M&A trends: 4 notable Q3 2025 cases out of the US, EU, and UK

ARTICLE

November 2025

Read time: 5 min

Global merger control authorities remained highly active in Q3 2025, scrutinizing deals across healthcare, aerospace, logistics, and digital platforms. In the United States (US), the Federal Trade Commission (FTC) and US Department of Justice (DOJ) pursued aggressive enforcement in home health markets, while European and United Kingdom (UK) regulators focused on cross-ownership, supply-chain resilience, and platform dominance.

These cases highlight evolving priorities: safeguarding innovation, addressing labor-market effects, and managing competitive risks in sectors critical to public welfare and industrial strategy. Below are four notable decisions that illustrate these trends.

Notable US case

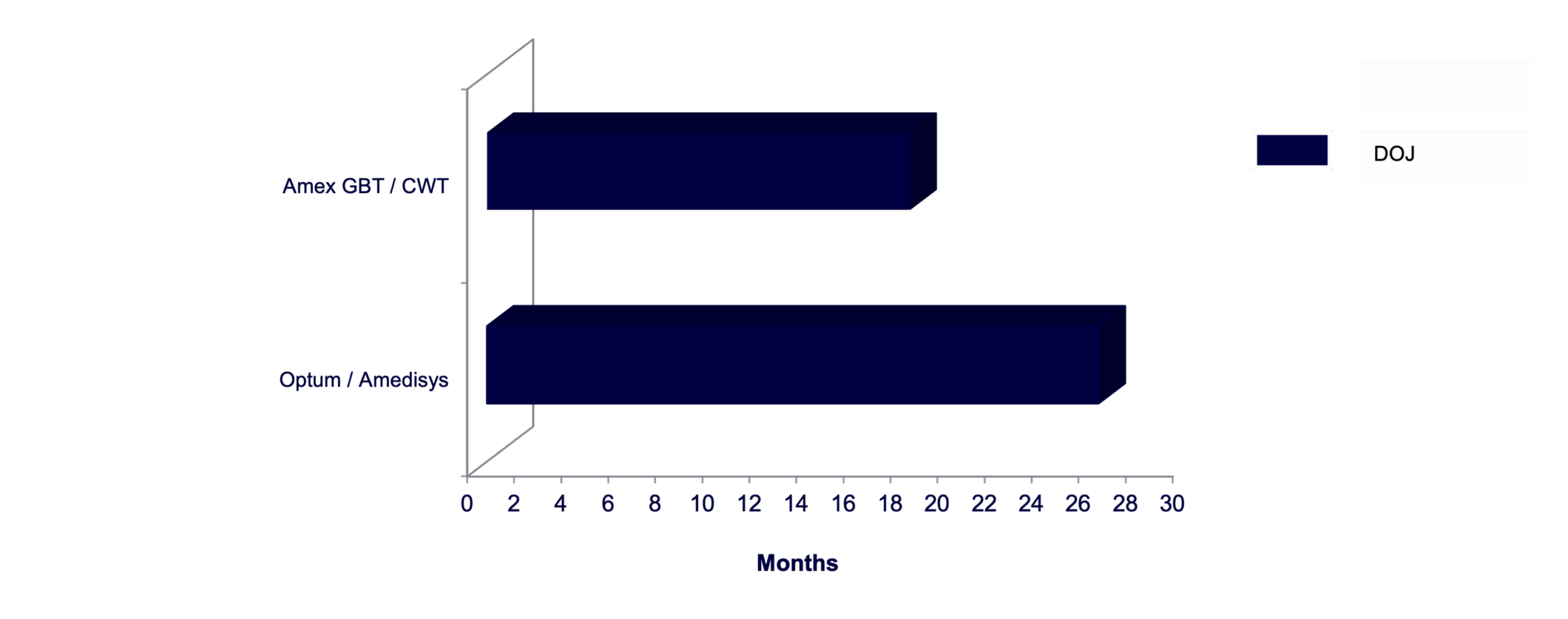

DOJ reaches mid-litigation consent in UnitedHealth’s acquisition of Amedisys

Markets/structure

The DOJ alleged the deal would eliminate head-to-head competition between two of the three largest providers of home health services, UnitedHealth and Amedisys, in hundreds of local markets.

Summary and observations

The DOJ alleged that the merger of two of the three largest home health services providers would result in a significant increase in concentration in hundreds of localized markets where UnitedHealth or Amedisys treat home health patients. Additionally, the DOJ alleged that the merger would substantially lessen competition in employment prospects, compensation, and other employment terms for home health and hospice nurses.

The settlement requires the divestiture of 164 home health and hospice locations across 19 states (which accounted for approximately $528 million in annual revenue). The settlement also required Amedisys to pay a $1.1 million civil penalty to settle the DOJ’s allegation that it falsely certified that it had provided true, correct, and complete responses under the Hart-Scott-Rodino Act during the DOJ’s merger review, when it produced a large volume of documents after that certification.

The DOJ touted the settlement as the largest divestiture of outpatient healthcare services to resolve a merger challenge.

Notable EU and UK cases

EC clears Prosus’s acquisition of JET with conditions

Markets/structure

Prosus/Naspers sought to acquire Just Eat Takeaway (JET), which operates online food-delivery platforms.

Summary and observations

The European Commission approved the transaction subject to commitments aimed at preventing conflicts of interest and overlap between Prosus’s holdings in competing delivery platforms. The remedies included a partial divestment and limits on Prosus’s ability to influence strategic decisions in rival companies, notably Delivery Hero.

The case illustrates the Commission’s growing scrutiny of cross-ownership structures in the digital platform economy and its effort to safeguard competitive independence among major European delivery operators. It has been widely discussed in competition law circles as a precedent for future investment-based control cases.

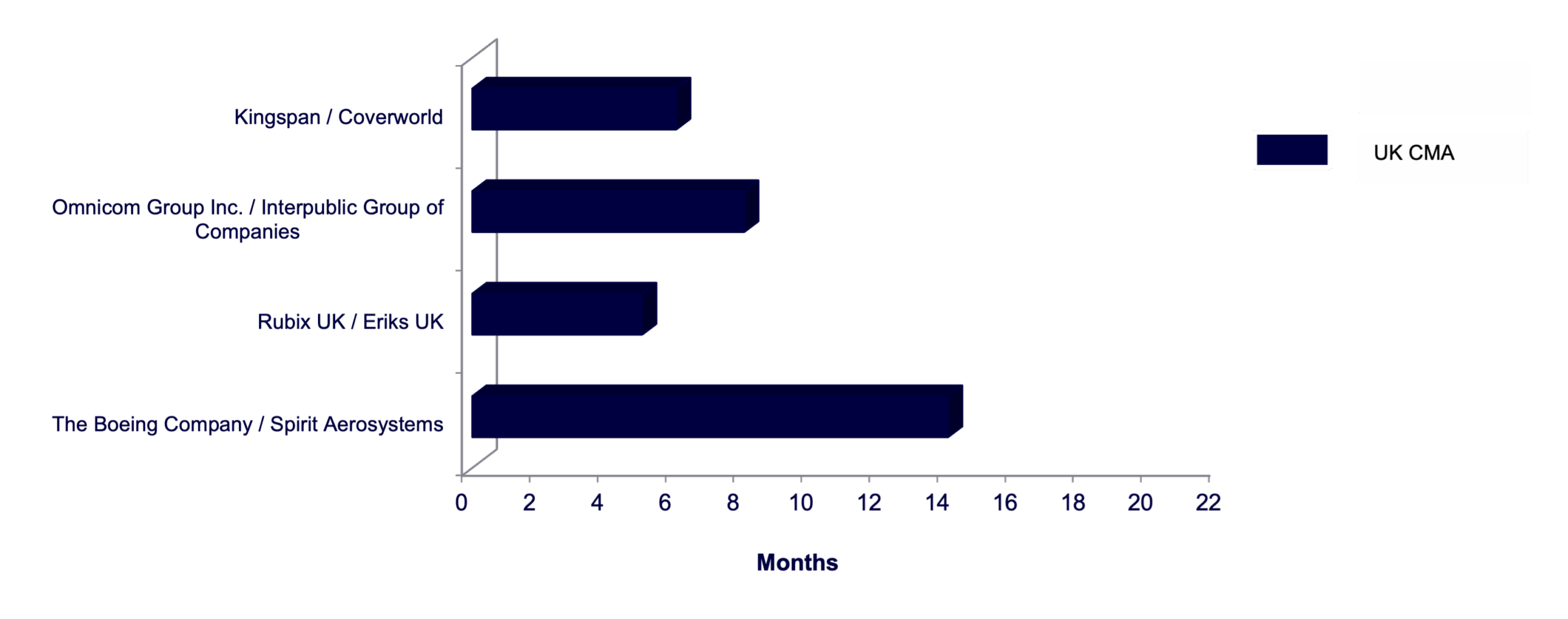

CMA clears Boeing’s acquisition of Spirit AeroSystems

Markets/structure

The CMA granted Phase I clearance on August 8, 2025, with the full decision published later in the month. The review focused on Boeing’s acquisition of Spirit AeroSystems’s segments, specifically upstream components and supply chain for aircraft structures.

Summary and observations

The CMA cleared the transaction following an assessment of potential supply-chain effects in the UK aerospace sector. The authority examined whether the acquisition might restrict competitors’ access to key structural components but concluded that sufficient alternative suppliers remained active in the market. The decision also acknowledged the deal’s relevance to the UK’s industrial strategy and the importance of resilient domestic supply chains.

The case is notable for showing how the CMA balances competition concerns with broader national policy considerations in strategically significant industries.

CMA approves merger of EVRi and DHL eCommerce UK

Markets/structure

The transaction involved parcel delivery and e-commerce logistics, combining DHL eCommerce UK with EVRi and granting DHL a structural and minority stake in EVRi.

Summary and observations

The CMA granted Phase I clearance on September 4, 2025, despite vertical and cooperative elements within the transaction. The deal combined EVRi’s domestic delivery network with DHL’s UK e-commerce operations, alongside a reciprocal minority shareholding. The authority investigated whether the structure could facilitate coordination or reduce competitive pressure in parcel logistics but found that strong competition would continue to constrain the merged entity.

The decision highlights the CMA’s pragmatic approach to joint-venture and partnership models in logistics and its recognition of evolving collaboration structures driven by e-commerce growth.

A deep dive into recent EU and UK antitrust M&A shifts: Flexible jurisdiction and remedies

ARTICLE

November 2025

Read time: 7 min

Recent developments in European Union (EU) and United Kingdom (UK) merger control reveal a dynamic shift toward greater flexibility and practical enforcement. From jurisdictional referrals that balance local expertise with centralized oversight to remedies designed for real-world viability, competition authorities are reshaping how deals are assessed and cleared. These changes underscore a growing emphasis on strategic planning, early engagement, and operational readiness – factors that now define success in navigating complex regulatory landscapes. For dealmakers, understanding these trends is essential to anticipate challenges and secure timely approvals.

Flexible jurisdiction: The EU’s “referral up” and “referral down” toolkit in action

Jurisdictional allocation remains a defining feature of EU merger control, and recent cases have showcased just how flexibly the system can respond to the realities of modern dealmaking. Two contrasting referrals highlight both the strengths and the ongoing challenges of this approach: one “down” to a national authority, one “up” to Brussels.

A key trend in recent years is the increasing willingness of the European Commission to refer cases with purely national competitive effects to Member State authorities, even when the transaction meets the EU dimension thresholds. The Mehiläinen/Regina Maria Healthcare Group case is a textbook example: Despite the parties’ global scale, the deal’s impact was confined to Romania’s healthcare sector. The Commission’s decision to grant a full “referral down” under Article 4(4) EUMR reflects a pragmatic approach, ensuring that local markets are assessed by those with the best knowledge of their dynamics.

The Commission’s readiness to hand over jurisdiction signals growing trust in national enforcers’ expertise – especially in sectors such as healthcare, retail, and media, where market realities are often highly localized. For dealmakers, this means that even “big ticket” transactions may ultimately be reviewed under national rules and standards, with all the procedural and substantive nuances that entails.

Nevertheless, the referral system is not a one-way street. The Brasserie Nationale/Boissons Heintz case demonstrates how national authorities can invite the Commission to take over cases that, while local in scope, raise complex or sensitive competition issues. Here, Luxembourg’s request for a “referral up” under Article 22 EUMR was driven by concerns about market concentration and the need for robust, resource-intensive analysis. The Commission’s acceptance and its subsequent imposition of significant remedies shows that Brussels remains the forum of choice for cases with broader policy implications or where national authorities seek additional firepower.

National authorities are increasingly proactive in escalating cases to the EU level when they perceive a need for deeper scrutiny, cross-border coordination, or simply a more authoritative outcome. This trend is particularly pronounced in markets with entrenched incumbents, high entry barriers, or where remedies may have ripple effects beyond national borders.

The dual-track referral system is a strength of EU merger control, allowing for both local expertise and centralized oversight. However, it also introduces unpredictability: The same transaction could be reviewed under very different standards depending on the direction of referral, the appetite of national authorities, or even political considerations. Recent speeches by Directorate-General for Competition officials have emphasized the need for “coherent and efficient” allocation, but the practical reality is that forum shopping and procedural jockeying remain part of the landscape.

For merging parties, the message is clear: Jurisdictional strategy is now a core part of deal planning. Early engagement with national and EU authorities, careful mapping of potential competition concerns, and scenario planning for divergent outcomes are more important than ever. The key is to anticipate where the deal will land and to be ready for a review that is both local and European in character.

When remedies get real: From aerospace divestments to local distribution dynamics

Recent merger reviews by the UK’s Competition and Markets Authority (CMA) illustrate how competition authorities are sharpening their focus on the practical enforceability of remedies and how early engagement can make the difference between clearance in Phase I and a lengthy investigation. The Safran/Collins Aerospace transaction, reviewed in parallel by the Commission and the CMA, and the Schlumberger/ChampionX inquiry, assessed solely by the CMA, offer valuable insights into how remedies are evolving not just in substance, but also in structure, timing and execution.

In the aerospace sector, both the Commission and the CMA identified concerns in the market for trimmable horizontal stabilizer actuation (THSA) systems. These components are essential for aircraft stability and fuel efficiency, and the merger would have combined two of the few global suppliers. To resolve these concerns, Safran committed to divesting its North American THSA business, including sites in Canada, the United States and Mexico. The buyer, Woodward Inc., was preapproved by both authorities, as confirmed in the Commission’s decision published on October 10, 2025. The Commission emphasised that the buyer had to possess the technical capability and financial resources to operate the business as an effective competitor over time.

The CMA’s early involvement proved decisive. By working with the parties from the outset, the authority ensured that an effective remedy package and a credible buyer were identified before formal clearance. It accepted undertakings in lieu of a Phase II reference and imposed an upfront buyer condition. The CMA reviewed Woodward’s integration plans, including the relocation of certain manufacturing activities to Poland, as well as transitional service agreements, knowledge transfer arrangements, and buyer suitability criteria. This proactive engagement allowed the case to be cleared in Phase I. By contrast, the Commission also cleared the deal with commitments but delegated oversight to a monitoring trustee, reflecting a more traditional approach. The comparison highlights the CMA’s growing insistence that remedies must be operationally viable before clearance is granted.

The Schlumberger/ChampionX case, concerning oilfield services, reinforces this trend. The CMA accepted commitments in lieu of a Phase II investigation, having been closely involved throughout remedy design and buyer selection. It even required that the buyer be pre-approved prior to clearance, underlining its focus on ensuring that divestments would function effectively in practice. While the CMA maintains a clear preference for structural remedies, it is increasingly open to behavioral measures where these ensure that a structural divestment remains viable and achieves its intended effect.

There are several takeaways from the CMA’s approach to remedies. First, merger remedies are no longer just about what to divest but also how that divestiture will work in practice. Competition authorities are increasingly focused on the real-world implementation of remedies. Whether in aerospace or energy services, regulators expect merging parties to demonstrate that a remedy is not only conceptually sound but operationally workable and ready to go at the time of clearance. Early engagement and proactive remedy planning are now critical to achieving Phase I outcomes. Second, while structural remedies remain the benchmark, authorities are showing a greater willingness to accept supporting behavioral measures where these enhance the effectiveness of a divestment. The shift is toward remedy realism: Effective execution now matters as much as formal design. Where parties engage early and present credible, practical solutions, even complex mergers can obtain swift clearance.

EU and UK M&A activity: By the numbers

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

Time from signing to clearance

3 takeaways from US antitrust M&A activity in Q3 2025

ARTICLE

November 2025

Read time: 6 min

United States (US) antitrust enforcement in Q3 2025 reflects a pragmatic yet assertive approach under the Trump administration. While the US Department of Justice (DOJ) and Federal Trade Commission (FTC) are clearing mergers swiftly or resolving concerns through settlements, they remain vigilant on compliance – particularly with Hart-Scott-Rodino (HSR) obligations. Recent speeches and enforcement actions underscore a dual message: Regulators aim to facilitate dealmaking where competitive risks are minimal but will not hesitate to impose penalties or pursue litigation, when necessary.

DOJ antitrust head says its aim is to “get out of the way quickly” in most cases

In a speech before the Ohio State University Law School, US Assistant Attorney General (AAG) Gail Slater, the head of the DOJ Antitrust Division, noted that the guiding principle of her (and the Trump administration’s) antitrust enforcement philosophy is to enforce the nation’s competition laws “both vigorously and fairly, with clear rules that facilitate, rather than stifle, the ingenuity of [America’s] greatest companies.” AAG Slater said the DOJ’s job is to call balls and strikes and let the free market do its job, opining that the “vast majority of mergers do not give rise to competitive concerns, and in those cases, [the DOJ] aim[s] to get out of the way quickly.”

These comments are consistent with what we have seen with the Trump FTC and DOJ in 2025, as demonstrated by the number of merger settlements entered into this summer by the FTC and DOJ. Though AAG Slater’s remarks only represent the Antitrust Division’s enforcement philosophy, the FTC appears to be following a similar philosophy as the DOJ by clearing transactions unconditionally or entering into significantly more merger settlements as compared to the Biden administration.

The chart below identifies the merger settlements entered into this summer and fall. It is important to note that the Trump DOJ agreed to settle two merger challenges brought by the Biden administration (Hewlett Packard Enterprise/Juniper Networks and United Health/Amedisys). Despite the merging parties proposing a settlement, the FTC elected to continue challenging GTCR’s acquisition of Surmodics, arguing that the divestiture proposed was not a stand-alone business and would not maintain competition. The Surmodics challenge demonstrates that the Trump antitrust regulators will still scrutinize proposed settlements and will not just accept any settlement if it does not address its concerns.

The chart below is provided as a refresher of the merger settlements entered into this summer and early fall.

Merger settlements in Q2/Q3 2025

| Merging parties | Settlement requirements | Antitrust agency |

| Synopsys/Ansys | Divestiture of optical software tools, photonic software tools, and consumption analysis tool | FTC |

| Keysight Technologies/Spirent Communications | Divestiture of high-speed ethernet testing, network security testing, and RF channel emulation businesses | DOJ |

| Safran/RTX | Divestiture of North American actuation business and related assets | DOJ |

| Hewlett Packard Enterprise/Juniper Networks | Mid-litigation divestiture of HPE Instant On business and license critical Juniper software to independent competitors | DOJ |

| UnitedHealth/Amedisys | Mid-litigation divestiture of 164 home health and hospice locations across 19 states | DOJ |

DOJ continues to pursue alleged HSR rules violations

Although the antitrust agencies are accepting more settlements, they are still aggressively investigating and prosecuting companies that they contend violate the HSR rules. As part of the UnitedHealth/Amedisys settlement referenced above, Amedisys agreed to pay a $1.1 million civil penalty and implement a compliance program to settle claims that it violated the HSR Antitrust Improvements Act (HSR Act) (15 U.S.C. § 18a) by allegedly falsely certifying that it had provided true, correct, and complete information in response to the DOJ’s merger investigation when it provided large volumes of information after that certification.

Amedisys is not the only company that has found itself in DOJ’s crosshairs. There have been a number of lawsuits related to HSR Act compliance either because parties allegedly provided false information or failed to comply with document production requirements. Former Assistant Attorney General for Antitrust Bill Rinner said in a speech earlier this summer that the division “will seek judicial sanctions where parties systematically abuse legal professional privilege or recklessly disregard professional duties by withholding or altering documents required by the HSR Act.”

AAG Slater announced the creation of the “Comply with Care” task force meant to resolve some of the challenges that the DOJ staff encounter with “problematic tactics” from outside lawyers and law firms – including what AAG Slater describes as delay tactics, privilege abuses, and destruction of evidence via failure to preserve ephemeral chat communications.

FTC and DOJ issue annual HSR report for FY 2024

The FTC and DOJ released the HSR Annual Report for FY 2024, which covers October 1, 2023, through September 30, 2024. While the report does not include the significant effects of the new HSR filing rules on parties making US premerger filings, it does contain key statistics regarding the number of filings overall and in specific sectors. In FY 2024, there were 2,031 transactions reported under the HSR Act, up from 1,805 the previous year. Roughly one-fourth of these transactions were valued at $1 billion or more. The agencies took action against 32 transactions – 18 by the FTC and 14 by the DOJ – resulting in abandonments, the restructuring of deals, or federal court litigation. Below are more key statistics on the number of challenged transactions and abandonments.

| FTC | DOJ | Total (percentage of transactions reported) | |

| Clearance granted to agency | 103 | 81 | 184 (9.0%) |

| Second requests | 30 | 29 | 59 (3.0%) |

| Enforcement actions against transactions | 18 | 14 | 32 (1.6%) |

| Abandonments/restructured transactions | 12 | 14 | 26 (1.3%) |

Below is the industry breakdown of adjusted transactions based on the acquired entity’s operations.

US M&A Activity: By the numbers

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

Time from signing to consent or investigation closing

Global M&A trends: Notable cases from the US, EU, and UK

ARTICLE

August 2025

Read time: 10 min

Recent antitrust enforcement actions in the United States and Europe have significantly influenced global M&A trends. Regulators approved major deals in highly concentrated markets, such as Synopsys / Ansys in the US and UniCredit / Banco BPM in the EU, only after substantial divestitures. However, outcomes have varied across different cases.

Notable exceptions include the atypical behavioral remedy in the US Omnicom / Interpublic case, which was driven by non-traditional concerns. Another exception is the rare unconditional Phase II clearance in the EU for Liberty Media / Dorna. In some instances, the intensity of regulatory scrutiny has led parties, such as Owens & Minor / Rotech, to abandon their transactions altogether due to the challenges posed.

Notable US cases

| Parties | Agency | Case Type (Cleared, Consent, Challenged, Abandoned) | Markets / Structure (as agency alleged) | Summary & Observations |

|---|---|---|---|---|

| Ansys, Inc. / Synopsys, Inc. | FTC | Consent | Products markets: optical software tools, photonic software tools for designing and simulating photonic devices, and register transfer level (RTL) power-consumption analysis tools

Geographic market: global |

Synopsys is a leading developer and supplier of software used to design semiconductors, known as electronic design automation software. Ansys is a provider of simulation software tools, known as simulation and analysis software, which engineers use for testing products, including semiconductors.

According to the FTC, Synopsys and Ansys directly compete against one another across all three markets alleged by the FTC. Synopsys and Ansys hold a duopoly of the optical software tools market, with a combined share of more than 60% of the photonic software tools market, and more than 70% of the RTL power-consumption analysis tools market. The complaint alleges that the proposed deal would eliminate head-to-head competition and lead to higher prices and decreased innovation, harming device manufacturers and consumers. Synopsys will divest its optical software tools and photonic software tools. In addition, Ansys will divest an RTL power consumption analysis tool called PowerArtist. Both Synopsys and Ansys will divest their assets to Keysight Technologies, Inc. |

| Hewlett Packard Enterprise Company (HPE) / Juniper Networks | DOJ | Consent (settling litigation) | Product market: enterprise-grade WLAN solutions

Geographic market: United States Merger would result in two firms (HPE and Cisco) controlling more than 70% of the relevant market |

On June 28, the DOJ announced a settlement with HPE and Juniper allowing their proposed merger to continue. In January 2025, the DOJ sued to block the transaction.

HPE and Juniper are the second- and third-largest providers of enterprise-grade wireless local area network (WLAN, i.e., wireless networking) solutions in the United States. The DOJ alleges that the unremedied transaction would eliminate fierce head-to-head competition between the companies and result in two companies, HPE and Cisco, controlling more than 70% of the market. According to the complaint, Juniper has been a fast-growing disrupter with its AI-driven solution, and HPE sought to acquire its smaller, innovative rival rather than compete on the merits. The settlement requires HPE to divest its worldwide Instant On business and to license the source code for Juniper’s AI Ops software used in Juniper’s WLAN products to one or more licensees approved by the DOJ. Per the terms of the settlement, HPE / Juniper must hold an auction to license the source code and enter into a perpetual, worldwide license allowing the licensee to operate the technology as a “viable, ongoing business.” |

| Omnicom Group Inc. / The Interpublic Group of Companies, Inc. | FTC | Consent | Product market: media buying services performed by advertising agencies

Geographic market: United States Merger would reduce the number of major competitors from six to five; merged entity would become the largest competitor |

On June 23, 2025, the FTC announced that it had entered into a consent agreement with Omnicom and Interpublic related to their proposed transaction. The consent agreement is atypical for several reasons. It is a behavioral remedy used in the context of a horizontal merger (typically resolved through structural remedies), and the relief it requires is unusual: it prohibits post-merger Omnicom from directing – unilaterally or in concert with other companies – advertising spend toward or away from any media publisher based on the publisher’s political or ideological viewpoints or content running alongside the publisher’s advertising inventory.

Omnicom and Interpublic are two of the largest advertising agencies in the United States. One of the services they provide to advertiser clients is representing those clients during negotiations with media publishers. In its complaint, the FTC does not allege any traditional theories of competitive harm (e.g., that the merger would allow the merged firm to increase prices to advertisers). Instead, the complaint focuses on coordination between advertising agencies regarding placement of ads with media publishers. According to the FTC, advertising agencies and the advertisers they represent have engaged in such coordination in the past, including through trade associations, and declined to advertise on certain websites. The FTC alleges that the merger would make this coordination easier, harming certain media publishers and their downstream consumers. The consent order, which appears to reflect Trump administration concerns about suppressing conservative speech, aims to prevent Omnicom, after the merger, from directing advertising dollars based on publishers’ viewpoints. |

| Owens & Minor / Rotech Healthcare Holdings | FTC | Abandoned | Product market: Home healthcare equipment | In July 2024, Owens & Minor announced plans to acquire Rotech. Owens & Minor’s Patient Direct business delivers medical equipment to home health agencies and patients, while Rotech also supplies home healthcare equipment. The companies mutually agreed to terminate the deal on June 3, 2025.

The companies’ decision to abandon the merger came almost eight months after the FTC issued a second request in October 2024. The companies had entered into a timing agreement with the FTC giving the agency until June 10, 2025, to complete its review of the transaction. Owens & Minor paid an $80 termination fee to Rotech in connection with the abandonment. |

Notable EU and UK cases

| Parties | Agency | Case Type (Cleared, Consent, Challenged, Abandoned) | Markets / Structure (as agency alleged) | Summary & Observations |

|---|---|---|---|---|

| UniCredit / Banco BPM | EC | Phase I; conditional clearance | Product market: corporate banking services to small and medium-sized enterprises and large corporate clients; retail banking services and insurance and asset management services

Geographic market: Italy, Germany, and Central and Eastern Europe |

On June 19, 2025, the EC approved UniCredit S.p.A.’s proposed acquisition of Banco BPM S.p.A., subject to structural remedies. The decision follows a Phase 1 investigation into the merger’s potential impact on competition in the Italian banking sector.

The EC found that the transaction would significantly reduce competition in 181 local markets across Italy, particularly in retail and small and medium-sized enterprise (SME) banking services. The overlap between UniCredit and BPM’s branch networks raised concerns about increased market power, potentially leading to higher prices and reduced service quality. However, no concerns were identified at the regional level for large corporate clients, nor were there risks of coordinated behavior due to the fragmented and opaque nature of the Italian banking market. To address these concerns, UniCredit committed to divesting 209 branches in the affected areas. These divestitures are designed to eliminate overlaps and preserve competitive dynamics. The commitments were positively received during the market test. In parallel, the EC rejected a request from the Italian competition authority to assess the merger under national law. Citing Article 9(3) of the EU Merger Regulation, the EC concluded it was better placed to handle the case, given its expertise and the strategic importance of the banking sector to the EU’s Capital Markets and Savings and Investment Unions. |

| Safran / Collins Aerospace | EC | Phase I; conditional clearance | Product market: supply of trimmable horizontal stabilizer actuator (THSA) systems

Geographic market: Europe |

On April 4, 2025, the EC approved Safran USA Inc.’s acquisition of part of Collins Aerospace’s actuation business, subject to structural remedies. The decision followed close cooperation with the UK’s CMA and the US Department of Justice, both of which approved the transaction with similar remedies. The deal involves the transfer of Collins’ THSA systems business, a critical component used in civil aircraft to ensure stable and fuel-efficient flight.

While Safran and the target’s operations are largely complementary, the EC identified significant competition concerns in the THSA systems market. The merger would have combined two of the few global suppliers in a market characterized by high entry barriers, long development cycles, and extended supply contracts. The EC concluded that the deal, as initially proposed, would likely reduce competition and lead to higher prices for aircraft manufacturers. To resolve these concerns, Safran committed to divesting its entire North American THSA business, including facilities in the United States and Canada and assets in Mexico. This remedy fully removes the overlap in THSA activities and was positively received during the EC’s market test. The EC found no competition issues in other aerospace markets affected by the deal, such as flight control actuators, pilot controls, or space launcher valves, due to the continued presence of alternative suppliers. It is worth highlighting that Safran publicly announced an agreement to sell its THSA business to Woodward Inc in August 2024. However, the EC has not yet approved Woodward as a suitable purchaser, and this assessment will be carried out separately as part of the buyer approval process. |

| Liberty Media / Dorna (MotoGP) | EC | Phase II; unconditional clearance | Sports media sector (licensing of broadcasting rights for sports content) | On June 23, 2025, the EC unconditionally approved Liberty Media’s acquisition of Dorna Sports, the commercial rights holder for MotoGP. The decision followed an in-depth investigation under the EU Merger Regulation and concluded that the transaction would not harm competition within the European Economic Area (EEA).

Liberty Media, which owns Formula 1, and Dorna, which manages MotoGP, are both active in the global sports media sector. The EC focused its review on whether the merger would reduce competition in the licensing of sports broadcasting rights, particularly in national markets for regular, non-premium sports content. For background, in the 2006 decision, when CVC Capital Partners Group Sarl acquired the holding company of the Formula One group of companies, the Commission defined a very specific product segment consisting of “TV rights for major motor sports events, including Moto GP and Formula One.” This was particularly relevant for Italy and Spain, where the combined share of the parties at the time ranged from 90% to 100%, which led CVC Capital to divest MotoGP rights that it held. Following this investigation, the EC found that Formula 1 and MotoGP are not close competitors in this space. Broadcasters typically distinguish between regular and irregular sports, and between premium and non-premium content. While both Formula 1 and MotoGP are regular sports, they are generally not considered premium in most EU countries. The EC concluded that broadcasters would still have access to a wide range of alternative sports content post-merger. The EC also examined whether Liberty Media’s largest shareholder, John Malone, could exert control over Liberty Global, a broadcaster active in several EU countries. It found no decisive influence or competitive concerns arising from this link. The EC ultimately determined that the merger would not significantly impede effective competition and cleared the transaction without conditions. Liberty Media aims to leverage its experience with Formula 1 to expand MotoGP’s global reach and appeal. This unconditional clearance in Phase 2 highlights the significance of the Liberty Media / Dorna case, as unconditional Phase 2 clearances represent less than 10% of Phase 2 results since 2019 (four out of 45) and only a total of 10 cases in the past decade. |