ARTICLE

Transfer pricing, MAP, and Fast Track: The forces reshaping tax controversy

June 3, 2026

Read time: 6 min

One message stood out during our Tax Symposium 2026 session, Tax controversy: What’s hot and what’s not: The Internal Revenue Service (IRS) is becoming more strategic in how it pursues audits and disputes in today’s resource-constrained environment.

During the interactive session, Alex Jupp, Susan Ryba, and Shawn O’Brien explored how the IRS and global revenue authorities are adapting after years of staffing disruptions, budget uncertainties, and procedural slowdowns. While many organizations expected enforcement activity to weaken, the reality looks different: Authorities are prioritizing narrowing examinations to focus on high-value targets and pushing taxpayers toward faster resolution pathways.

The result is a controversy environment where preparation, documentation, and execution are critical differentiators.

High-risk areas face mounting audit pressure

Transfer pricing continues to dominate controversy activity because it is one of the most fact-intensive and subjective areas of tax enforcement, leaving room for disagreement on economics, valuation, and characterization.

Cost-sharing arrangements; intellectual property (IP) migration structures; and challenges related to development, enhancement, maintenance, protection, and exploitation are particularly difficult to resolve, especially where multiple jurisdictions approach the same transaction from different perspectives.

Simultaneously, valuation disputes are becoming more common across industries, including in renewable energy transactions and IP structures. Revenue authorities are revisiting assumptions driving pre-COVID-19 valuations while taxpayers face growing scrutiny over their methodologies, comparables, and projected business outcomes.

Tax authorities are not auditing more issues, necessarily. Rather, they are auditing more selectively, prioritizing areas where they have technical familiarity, established playbooks, and the potential for large adjustments.

Sharper IRS enforcement demands early preparation

Despite the resource constraints, IRS exam teams are operating with clearer priorities and added pressure to resolve cases. That approach is changing how audits unfold.

The panelists noted a more disciplined approach from IRS exam teams that is characterized by:

- Narrower issue selection

- Greater focus on resolving legacy cases

- Wider use of standardized information requests

- Harsher penalty assessments

- Longer statute of limitations extension requests earlier in the audit

The practical implication for taxpayers is clear: Controversy management requires earlier strategic planning.

Companies that proactively develop supporting documentation, preserve evidence, and clearly articulate technical positions before an audit are often better positioned to reduce the number of disputes and accelerate resolution.

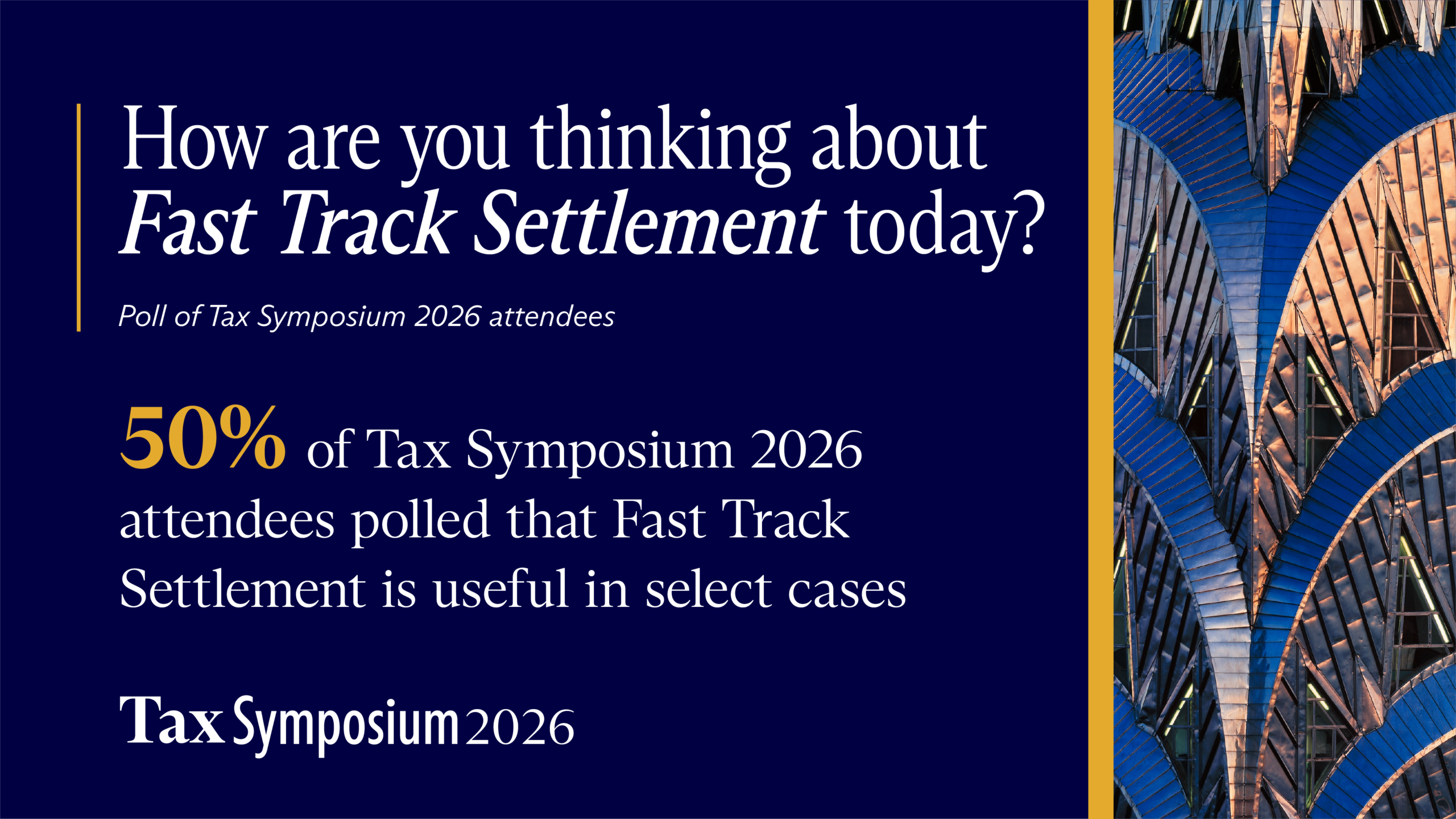

Fast Track Settlement is gaining momentum

One of the most significant procedural developments discussed during the session was the IRS’s increased push toward Fast Track Settlement.

Fast Track allows taxpayers and IRS exam teams to enter a mediation-style process facilitated by the IRS Independent Office of Appeals (IRS Appeals), with the goal of resolving disputes within approximately 120 days.

Senior IRS leadership is actively encouraging Fast Track as part of a wider effort to move disputes through the system more efficiently. Fast Track’s advantages include accelerated timelines compared to traditional appeals, earlier insight into the IRS’s substantive positions, added pressure on both sides to engage meaningfully in settlement discussions, and opportunities to resolve penalties alongside substantive issues.

However, success with Fast Track depends heavily on preparation. Taxpayers must enter the process with a fully developed factual and legal record because introducing new information later can delay or derail settlement discussions.

The focus on Fast Track may also have broader implications for traditional appeals timelines. As more experienced IRS Appeals personnel are diverted toward mediation programs, taxpayers in the standard appeals queue may face even longer resolution periods.

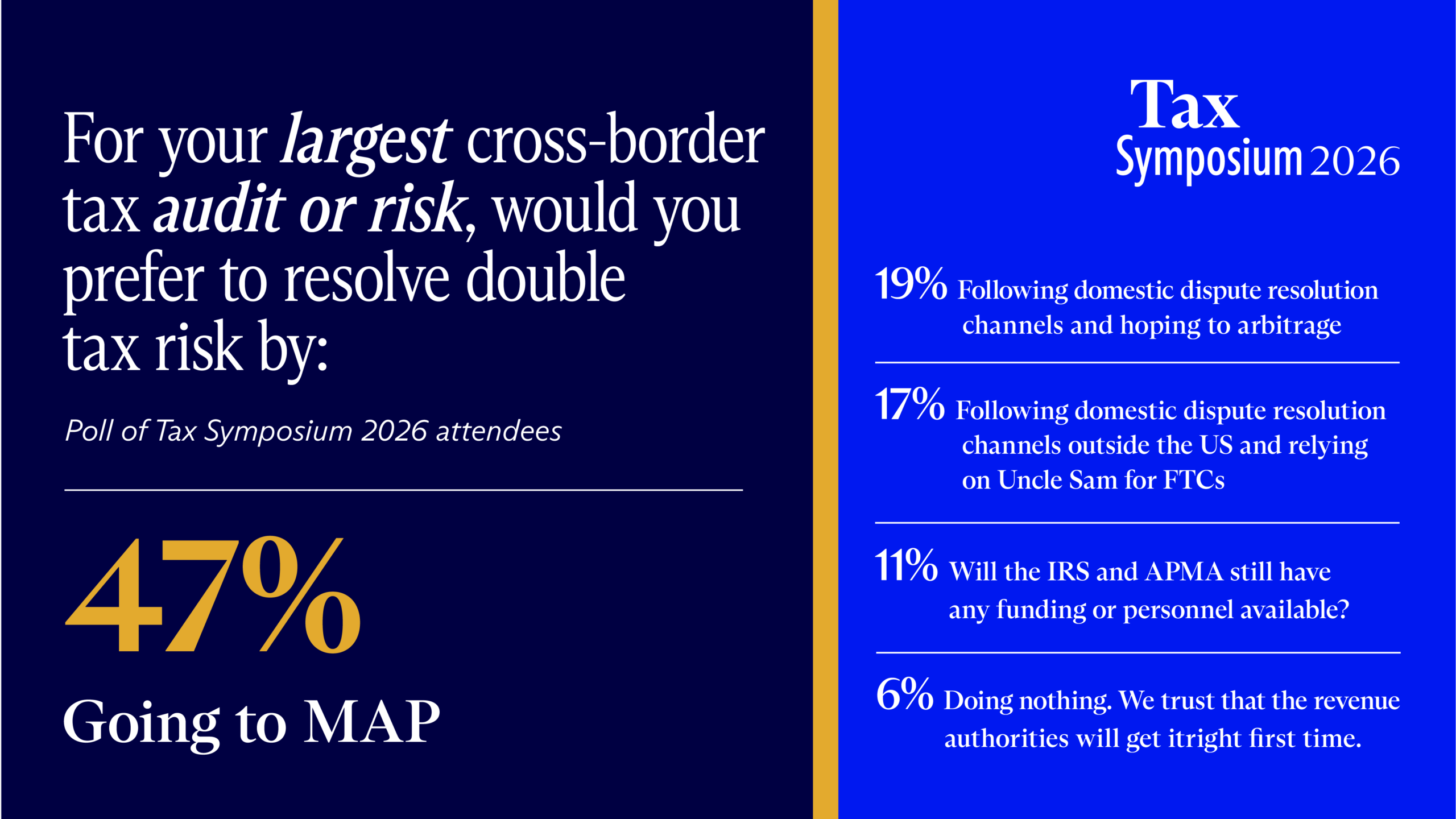

Cross-border controversy and MAP remain critical yet complex

Cross-border controversy continues to create some of the most challenging dynamics for multinational businesses.

When asked how they would prefer to resolve cross-border disputes involving double taxation risk, nearly half of session attendees selected Mutual Agreement Procedure (MAP).

MAP is an important tool for disputes involving transfer pricing adjustments between jurisdictions. However, attendees also acknowledged growing frustrations with the process, including extended timelines, limited transparency into competent authority negotiations, jurisdictional inconsistencies, and a narrow procedural scope in certain countries.

MAP works best when jurisdictions are effectively addressing the same underlying issue. Cases involving different legal characterizations, valuation disputes, or complex IP structures can be harder to resolve through competent authority processes. The follow-on from MAP is equally important, with multinationals increasingly considering wrapping MAP outcomes into an APA.

Taxpayers who choose not to pursue MAP may face questions from the IRS about whether they exhausted all remedies before claiming foreign tax credits in the United States. As a result, companies must evaluate their controversy strategies globally and earlier in the dispute life cycle.

Preparation is becoming the defining advantage

With controversy strategies shifting upstream, companies are placing greater focus on building audit-ready documents, aligning their tax planning with defensible operational substance, evaluating controversy risk during transaction structuring, managing cross-border positions consistently across jurisdictions, and developing proactive engagement strategies with revenue authorities.

As tax authorities become more targeted and resolution timelines accelerate, taxpayers who enter audits organized, documented, and strategically aligned are often best positioned to manage risks and the outcome.

Looking ahead: What tax authorities should prioritize

With the tax controversy landscape rapidly evolving, our panelists identified several priorities for tax authorities:

- Expect continued focus on transfer pricing, valuation, and cross-border substance

- Prepare for faster procedural timelines and earlier settlement discussions

- Consider Fast Track Settlement as a potential strategic tool

- Build documentation with penalties and privilege in mind

- Coordinate global tax controversy strategy across jurisdictions earlier in the process

- Treat controversy readiness as part of broader tax planning and governance

The environment may still be resource constrained, but tax authorities are becoming more efficient in how they deploy those resources. For taxpayers, that means controversy preparedness is no longer reactive but a core part of risk management.