ARTICLE

November 2025

Read time: 5 min

It has been a busy year for European financing markets, with robust demand for refinancings driving volume. The fourth quarter of 2025 likely will see more transactions coming to market in preparation for an even livelier 2026, and lenders are gearing up for another 12 months of strengthening deployment.

In September 2025, McDermott Will & Schulte assembled hundreds of healthcare professionals, investors, and industry changemakers for the annual HPE Europe conference in London. Our keynote speakers, Steph McGovern and Robert Peston, hosts of the hit UK podcast The Rest is Money, outlined geopolitical trends impacting the markets, launching lively discussions about how private credit funds are addressing the healthcare sector and what borrowers will be looking for in the year ahead.

Investors and borrowers alike are bullish about how hot the European financing markets have been this year, noting the proliferation of deal opportunities and advantageous terms. After an election year in the United States that saw a cautious return of activity following a slowdown in 2022 and 2023, limited partners were hungry for returns in 2025 and put pressure on sponsors to execute refinancings and dividend recapitalisations.

Private credit funds have enjoyed strong fundraising appetite in the higher interest rate environment of recent years and now are experiencing pressure to deploy capital and fierce competition for a small number of quality assets. The uncertainty created by the new US administration dashed expectations of a healthcare M&A surge coming into Q1 2025, but clarity emerged through the course of the year, and industry leaders expect more sellers to soon start bringing assets to market.

Ongoing disparities in pricing expectations between buyers and sellers have led to slower deal processes, but stakeholders anticipate that bid-ask spread will narrow going into 2026. Some private equity funds have held assets longer than anticipated and now are eager to transact.

“For lenders, it’s been a year defined by compression – tighter spreads, looser docs, and a more competitive deployment environment. The challenge now is to balance discipline without passivity. That tension has really defined 2025 so far.” – Aymen Mahmoud, European head of finance and co-head of the London Transactions Group and the London Finance, Restructuring, and Special Situations Group, McDermott Will & Schulte.

Creativity, certainty, and portability are front of mind

Amid pressure to deploy, credit quality will be more important than ever in 2026. Relationships with sponsors remain a priority, as do documentation, structuring, amortisation, and the ability to secure a seat at the table early in the event that the asset experiences difficulties.

A growing number of credit funds are building sector-focused teams with deep expertise in the healthcare and life sciences space, the better to evaluate assets’ creditworthiness. Developing specialist knowledge can equip lenders to handle more complex situations and be paid additional yield for doing the work that other lenders may be less willing to embrace.

A tough dealmaking environment and an uncertain macroeconomic and geopolitical backdrop have prompted borrowers to seek out lending partners that can deliver reliability and creative financing solutions. Portability features have played a significant role in leveraged finance negotiations. These features allow a debt facility to roll over even if the company is sold, without triggering a mandatory repayment.

In today’s market, certainty also is increasingly a key differentiator. In order to sign up to a deal first, some lenders are committing to transactions without doing a great deal of work, relying on sector knowledge to gain an advantage over competitors.

“Private credit is no longer defined by what banks don’t do. It’s evolving into a multi-product platform capable of addressing everything from securitisation to equipment and royalty financing. The direction of travel is sophistication, not substitution.” – Aymen Mahmoud, European head of finance and co-head of the London Transactions Group and the London Finance, Restructuring, and Special Situations Group, McDermott Will & Schulte.

Looking ahead to 2026

Investors and industry leaders are cautiously optimistic about the outlook for the next 12 months. They anticipate that artificial intelligence and other emerging technologies will create more healthcare investment opportunities and drive activity. Other mega trends such as nearshoring of manufacturing and demographic change will also play into investment theses.

Sponsors still face uncertainty over government spending, trade tariffs, and healthcare policy and regulation. A meaningful decline in interest rates is not expected imminently, so it may take time for M&A dealflow to fully unlock. However, recent years have highlighted the resilience of mature economies and the enduring attractiveness of the healthcare and life sciences sector for both sponsors and their lenders. If economic conditions downgrade, the financing markets could tighten, but with record dry powder in the system and signs of dealflow picking up, the hope is that 2026 will see the return of M&A. That robust outlook will likely continue.

“The dislocation of 2023 was an inflection point. With syndicated markets effectively shut, private credit demonstrated its ability to step into core territory and execute at scale. That credibility has endured as macro events drove turbulence. 2024 brought the banks back into the mix, but the market reset has left a more stable equilibrium. The interplay between private and public capital is healthier and far less binary than before as part of private credit’s evolution.” – Aymen Mahmoud, European head of finance and co-head of the London Transactions Group and the London Finance, Restructuring, and Special Situations Group, McDermott Will & Schulte.

Inside HPE Europe 2025 | European healthcare investment in 2026: Outpatient services, optimisation, and optimism

ARTICLE

November 2025

Read time: 5 min

As macro trends such as population growth, ageing demographics, and co-morbidities place increasing pressure on healthcare systems, investors are once again seeking out compelling opportunities in the healthcare services space. Going into 2026, investors are expected to double down on several emerging growth areas.

In September 2025, McDermott Will & Schulte assembled hundreds of healthcare professionals, investors, and industry changemakers for the annual Healthcare Private Equity Europe conference in London. Our keynote speakers, Steph McGovern and Robert Peston, hosts of the hit UK podcast The Rest is Money, outlined the latest geopolitical trends impacting the markets and launched lively discussions about what might be next for private equity investment in European healthcare.

One major trend that investors are watching is the shift towards outpatient care. In the United States, use of hospital beds has reduced by half over the past 50 years despite population growth. Europe too is seeing increased use of outpatient settings across a broad range of specialties. In France, outpatient surgical procedures have grown from 47% of all surgeries in 2013 to 64% in 2024. Cataract surgery, for example, has moved almost completely out of hospital settings on both sides of the Atlantic.

One US study showed that 10% of operations currently taking place in hospitals could be shifted to outpatient settings without having any impact on clinical outcomes. Many patients are keen to avoid hospital stays, so the move to alternative spaces could open up fresh investment opportunities.

The outpatient sector is attractive to investors for several reasons, including market tailwinds, the potential for operational and financial efficiencies, policy support, and technological innovation.

“The data shows that private equity has become a significant player in outpatient care both in the US and in Europe. There are a lot of opportunities in Europe now for private equity to step in and help deliver more affordable and efficient care in outpatient settings.” – Holger Ebersberger, partner, McDermott Will & Schulte.

Addressing skilled labour shortages

Staffing shortages continue to challenge the European healthcare sector, with 21 out of 28 European countries reporting a shortage of doctors in the last few years and 16 reporting a shortage of nurses. Data from the European Labor Authority estimates that the EU healthcare workforce is short 1.2 million doctors, nurses, and midwives.

As staffing shortages create myriad issues for healthcare providers, private equity firms have been focused on delivering solutions. Investors are particularly interested in opportunities that make use of emerging technologies, such as artificial intelligence (AI) and robotisation, to make systems more efficient.

AI use cases are beginning to emerge across the healthcare ecosystem. Several HPE Europe 2025 panellists pointed to recent investments that are already delivering value in diagnostics, medical imaging analysis, bed optimisation, and fall prevention. Moving forward, investors expect advances in personalised medicine, powered by AI and robotics, to offer significant value.

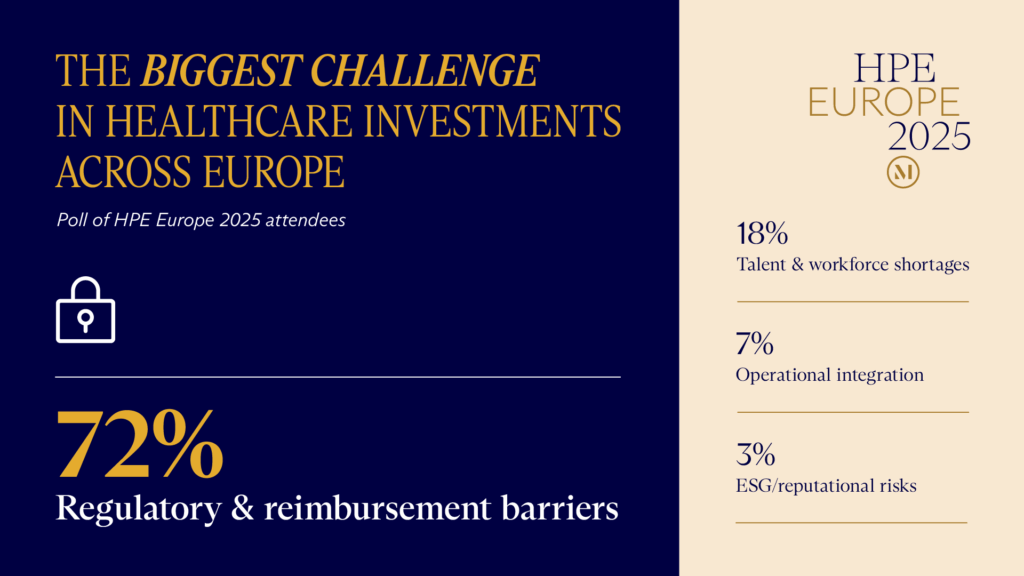

HPE Europe attendees identified talent and workforce challenges as one of the biggest difficulties facing healthcare investors in Europe today. In a poll, 72% of respondents stated that regulatory and reimbursement barriers were the biggest challenge to investments across Europe in 2025. Staffing ranked second with 18%.

Opportunities for future dealmaking

Investments in healthcare services businesses in Europe have slowed over recent years following a period of intense capital deployment in the wake of the COVID-19 pandemic. Some of those past transactions received elevated valuations but did not generate the returns expected. Since then, regulatory scrutiny of private capital in healthcare, reimbursement challenges, and an ongoing bid-ask spread issue have caused the buyer universe to decrease.

Today, with interest rates coming down and a clear ongoing need for affordable care in an outpatient setting, private equity buyers are showing signs of cautious interest again.

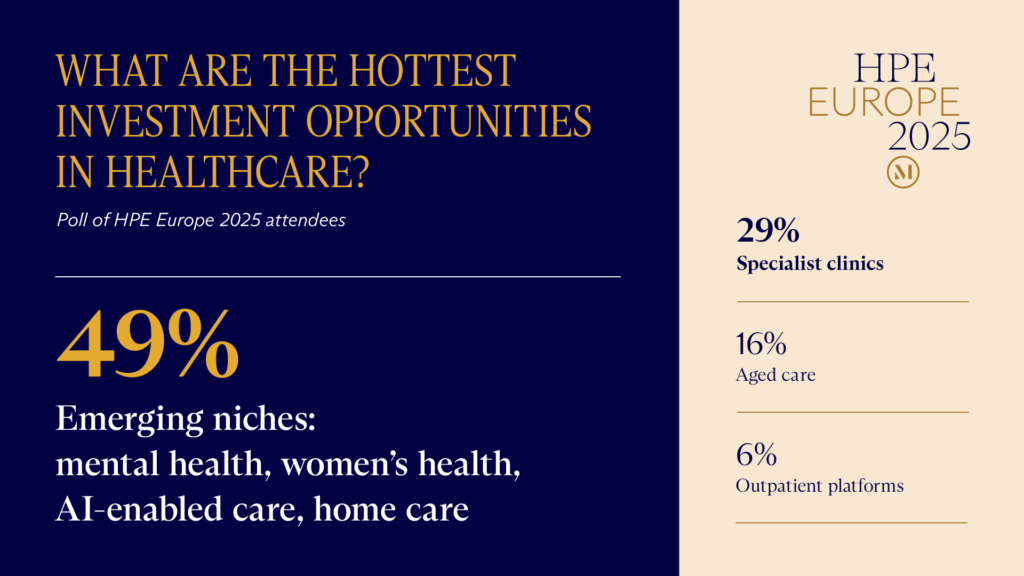

Some of the most attractive healthcare services investment hotspots today are in emerging niches such as mental health, women’s health, AI-enabled care, and home care, according to 49% of HPE Europe attendees. Specialist clinics in areas such as ophthalmology, fertility, orthopaedics, and dermatology are also garnering interest, according to 29% of respondents.

Investment bankers and other dealmakers expect more transactional activity in healthcare in 2026 than has been evident in 2025. Large listed healthcare businesses likely will prune their portfolios, creating carve-out opportunities for investors capable of such transactions.

The European market likely will also see more sponsor exits in the small to mid-cap space, more cross-border expansion of regional platforms, and heightened investor focus on domestic businesses rather than entities with global supply chains.

“There are now interesting investment prospects coming up in outpatient care and healthcare services, with a backlog of exits waiting to transact. Investors see ways to do things better and a swathe of value-creation opportunities driven by technology, which we expect to lead to more activity in 2026.” – Jason Zemmel, partner, McDermott Will & Schulte.

HPE Europe 2025: What to know, what’s next

VIDEO

September 25, 2025

Read time: 6 min

On September 25, hundreds of healthcare professionals, investors, and industry changemakers gathered in London for McDermott Will & Schulte’s annual Healthcare Private Equity (HPE) Europe conference.

Keynote speakers Steph McGovern and Robert Peston, hosts of the hit UK podcast The Rest Is Money covering money, politics, and the markets, kicked off a high-impact event with remarks from the main stage at the Hyde Park-adjacent Peninsula hotel. Additional insights on European healthcare investing trends flowed from panels throughout the day, including industry leaders’ thoughts on life sciences developments, value creation, and developing exit strategies.

As HPE Europe’s official knowledge partner, McKinsey & Company delivered sharp insights into the position of private capital in 2025 and the outlook for healthcare deal activity. The teams at McKinsey and McDermott Will & Schulte have compiled the following key takeaways from the event.

Shifting pressures in European life sciences

- Manufacturing and R&D pipelines: European life sciences business have faced significant cost pressures and shifting global market dynamics over the past 12 months, impacting manufacturing and research and development (R&D) pipelines.

- Biotech innovation: Attendees noted that global competition in this space continues to intensify, with significant innovation emerging from multiple markets. This dynamic is influencing European strategies, particularly in areas such as oncology and cell therapy, where cost pressures and the pace of discovery are creating a more competitive environment.

- Investor areas of interest: Despite shifting pressures, there are strong companies coming out of Europe. Panellists noted that investors are focusing on rare diseases and the supporting pharma services, along with cardiometabolic diseases, oncology, and neuroscience. Immunology and inflammation, and particularly autoimmune disorders, also continue to see meaningful early-stage investment.

- Biosimilars and generics: Given the constraints on budgets and pace of global innovation, attendees noted that biosimilars and generics are increasingly interesting to European investors, along with pharma services companies that service generics. In uncertain times, many European life sciences companies are looking to diversify portfolios as a means of derisking.

Opportunities in the next generation of European healthcare

- Outpatient care: This is an area of healthcare investment that attendees noted has many positive drivers. For example, despite population growth, US hospitals have half the number of beds than they did 50 years ago. Outpatient surgery use has grown across specialties, most notably cataract surgery, with huge potential savings for the healthcare system. In the right context, private capital can help deliver more affordable and efficient care in outpatient settings.

- Staffing shortage solutions: Staffing shortages are a critical factor in the European healthcare market, with Europe currently short of 1.2 million medical staff, almost 20% of the total. Solutions that address these shortages can create value, with opportunities for investment in emerging technologies like AI and automation to make systems more efficient and free up workers to focus on patient care or other key priorities.

- Overcoming regulatory and reimbursement barriers: In a poll of HPE Europe attendees, 72% felt that regulatory and reimbursement barriers were the biggest challenge to healthcare investments across Europe today, followed by talent and workforce shortages (18%).

- Specialists and niche areas: Some of the most attractive investment hotspots today are in emerging niches like mental health, women’s health, AI-enabled care, and home care, according to 49% of the HPE Europe audience, followed by specialist clients like ophthalmology, fertility, orthopaedics, and dermatology (29%).

“European healthcare continues to draw strong interest from private capital. Investors seem especially focused on the growing importance of consumer-driven models and AI as a tool to spark innovation, improve care, and enhance portfolio efficiency.” – Michael Morley, partner in the London office of McKinsey

Financing: Creativity, certainty, and portability are front of mind

- Refinancing: So far, 2025 has been a busy year for the European financing markets, with a focus on refinancing activity. As we move towards Q4, more deals are starting to come to market, though processes are generally taking longer as the bid-ask spread remains an issue.

- Credit quality: For private credit funds, there is pressure to deploy and a need to find opportunities, but the overriding consideration is credit quality. Lenders are focused on documentation, structuring, amortisation, and getting to the table early in the event of difficulties. Truly understanding creditworthiness often comes down to having deep sector knowledge.

- Portability: In healthcare investment deals, portability from one deal to another has become a major point of negotiation. And those with the ability to commit to a deal faster than others often have a competitive edge.

- Private credit: This may continue to offer a more flexible solution to borrowers. Private credit is expanding its product suite to offer financing tools such as securitisation, equipment financing, or royalty financing. There is a growing focus on products that look to both cashflows and assets as collateral, and there may be yield to be found in lending into complexity.

“The current mood among healthcare investors and CEOs is one of cautious optimism. Financial conditions are improving, cost pressures are there, regulatory hurdles are there, but deals are getting done. We have been particularly active in Q3 and are excited about what is next.” – Ira Coleman, chairman of McDermott Will & Schulte

Conclusion

Conversation at HPE Europe was wide-ranging and diverse, reflecting the breadth and depth of the healthcare private equity opportunity set and the trends impacting capital flows.

We look forward to continuing these conversations with our clients and partners in the months ahead. Please reach out if you would like to explore any of these themes further.